The geeks shall inherit the earth

In some cities in Brazil, you don’t need to carry cash. Even street peddlers accept credit cards in Sao Paulo.

It comes as no surprise, then, that there is a move to digital payments and banking happening in the country, more specifically in the city of Sao Paulo. One example is Nubank, one of the hottest Brazilian start-ups in recent years.

Although relatively digital, the Brazilian banking system is very concentrated: the four largest banks control about 75% of the banking assets in the country [9], a result of a series of mergers and acquisitions over the last 15 years.

With scarce competition and high interest rates (the Brazilian reference rate, Selic, is now at 14% a.a.), the banks charge what is one of the highest spreads in the world. The average credit card interest rate in Brazil is north of 470% a year [10]. Banks say that the high rates are due not only to the high prevailing reference rate, but also because of high default rates.

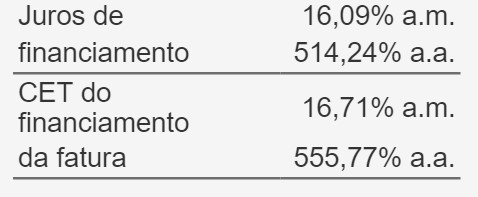

If you don’t believe me, here is a screenshot of my latest credit card bill, showing a staggering 514.24% yearly interest rate.

Is there a David to challenge these Goliaths?

One start-up is trying to break into this exclusive world of the Brazilian banks without opening a single branch. Nubank is a digital financial services provider that offers a credit card, coupled with a personal finance app that lets you track, label and organize your spending. The app is very intuitive and simple, and they charge no fees at all.

Besides charging no fees, Nubank charges lower interest rates on credit card debt compared to other Brazilian banks: the average rate is 145% a year, with rates as low as 38.5% a year [3]. This is a screenshot from wife’s Nubank credit card bill, showing interest rates of 41.86% a year.

![]()

They claim this ability to charge less stems from their low-cost structure – possible due to the digital nature of the service provided – and because of their superior credit risk modeling, which leverages cutting edge big data analytics.

Not only is the service all provided online, but also the whole application process can be done from your smartphone. After downloading the app, you just follow the instructions, take a couple of pictures of selected documents, and you’re done! More than 3 million people have already registered, but there is currently a waitlist to become a client. (Tip: getting a referral from a current customer increases your odds of being accepted).

The miracle of digitization

Nubank’s capacity to threaten the establishment has been recognized by a handful of VC funds (e.g. Sequoia Capital, Peter Thiel’s Founders Funs etc), which have invested at least $80 million so far [2] [3] [7]. Their ability to enter this market was made possible thanks to the power of data: not only is the whole experience provided through the app, but also their superior credit modeling is enabled by big data.

To better decide which customers to accept and how much to charge, Nubank has put together a team that uses public and private data to assess credit risk. Whereas the average bank considers about 10 variables when making these assessments, Nubank uses from 2,000 to 3,000 variables [3]. Credit rating agencies are not as widespread in Brazil as they are in the United States, so there is huge value in having a state-of-the-art internal credit model.

Commandments for the future

There are 168 million Smartphone users in Brazil, a number expected to reach 236 million by 2018 [11]. Also, only about 28% of the Brazilian population owns a credit card – versus about 70% of the adult population in the USA [13]. These factors, coupled with Brazilian’s dissatisfaction with the major bank’s services, makes for great opportunity for Nubank.

To make things even more promising, Brazil actually has the world’s largest number of installed PIN card prepared POS equipment, at 4.4 million units [12].

To fully capture the potential market, I believe they should follow the path of a couple of other small digital banks in Brazil and broaden their product offering, with actions such as:

- Offering other credit products, such as personal loans and the “cheque especial”, a very popular form of overdraft credit used in Brazil

- Offering savings products: XP Investimentos, Sofisa Direto, Original and other banks have already tapped into this market

- Expanding to other countries: initial expansion in Latin America would be the natural way to go

- Offering other payment methods: debit cards, online payments (like Paypal and players Moip, Pagseguro etc)

- Starting their own points program: incentivize the use of their credit cards, maybe partnering with a big Brazilian player such as Multiplus

Their success would be great for consumers and they are now in a good position to make it happen.

(798 words)

[1] Company Website, Nubank,

[2] “The New York Times”, Jun 2, 2015, http://www.nytimes.com/2015/06/03/business/dealbook/nubank-raises-30-million-to-challenge-banking-in-brazil.html

[3]”Tech Crunch”, Jun 2, 2015,

[4] “O Estado de São Paulo”, Sept 25, 2014,

[5] “Exame”, May 23, 2016,

http://exame.abril.com.br/pme/inovador-nubank-ganha-premio-no-vale-do-silicio/

[6] “Globo”

[7] “The New York Times”, Jan 6, 2016,

[8] “The Economist”, Apr 9, 2016,

[9] “The New York Times”, Aug 13, 2015,

http://www.nytimes.com/2015/08/14/business/dealbook/in-good-times-or-bad-brazil-banks-profit.html

[10] “Globo”,

[11] “Folha de Sao Paulo”, Apr 15, 2016,

[12] “Convergencia Digital”, Jun 22, 2016,

http://sis-publique.convergenciadigital.com.br/cgi/cgilua.exe/sys/start.htm?infoid=42723&sid=135

[13]”Credit Cards .com”,

http://www.creditcards.com/credit-card-news/ownership-statistics-charts-1276.php

Thanks for the article, Arthur. I agree with you that this market is ready for disruption and it’s great for both consumers and the economy that a new player is challenging the big players. However, one thing that concerns me is the scalability of the business model. You mentioned that there is already a waiting list to receive credit; do you think that they have already reach the maximum of their potential? I am worried that credit orifue=kes will deteriorate if they try to speed up their growth or go into other products.

Thanks for the post, Arthur!

Given that NuBank is offering a fundamentally different value prop for its competitors, I am wondering how different stakeholders will respond to their product offering. Do you anticipate new regulatory restrictions coming into play given this new operating model / product offering? Do you anticipate consumers mistrusting this new platform given its digital nature, susceptibility to security breaches and vastly reduced interest rates? Although the lower interest rates are attractive to consumers, I imagine they may be hesitant / mistrustful of this offering at first, since it is so dramatically different than other market players. In addition, the bank does not have physical branches, which will require a change in consumer behavior.

I’d also be interested in learning more about NuBank’s use of data. What is the biggest breakthrough / insight they have pulled from the data so far? How are competitors responding to digital disruption and the introduction of this new competitor?

Reference: https://techcrunch.com/2015/06/02/brazils-nubank-raises-30m-led-by-tiger-to-build-out-its-mobile-based-credit-card-business/

Arthur, this was incredibly interesting. I had no idea interest rates were that high for credit cards in Brazil. Are default rates really so high to justify such an APR? In the US, these sort of rates are typically only seen on payday loans and only taken by people ignorant of the costs. It’s somewhat seen as an immoral business model. Often payday loan shops and car dealerships that finance at high APRs will pop-up outside military bases and try to lure young enlisted people to take loans or buy cars at interest rates about 50%. For the interest rates you mentioned in Brazil, this article lays out your monthly payments if you carried a thousand dollar balance(http://time.com/money/4094286/brazil-credit-card-rates/). It says basically your monthly payment would be $355 a month. At rates that high, doesn’t it make it more likely someone would rather default than pay it off thereby making this already bad cycle worse?