Attention Hastings: Millennials are replacing “mom and pop” and machine learning will wipe you out

Digital players like biBerk are delivering commercial insurance coverage directly to small business owners online and threatening to turn the small commercial insurance industry on its head

Within the next 5 to 10 years, Hastings Mutual Insurance Company and other mid-size small commercial insurance carriers will be wiped out by online insurance companies. The process for a small business owner (e.g., local baker) to buy commercial insurance is surprisingly painful. While individuals can buy personal auto insurance directly online with a few clicks, business owners need to spend hours on the phone with an agent, or physically go into an agent’s office, sometimes waiting days to receive a quote. The process is cumbersome because insurance companies need to ask a lot of questions about a business to assess its risk (e.g., age of office building, number of employees, types of vehicles) [1]. However, digital players are changing the way insurance coverage is delivered to businesses by leveraging machine learning to allow customers to purchase commercial insurance with the same convenience as auto insurance. As millennials replace “mom and pop” and become small business owners, companies like Hastings need to adapt to meet expectations of convenience and speed, or risk becoming obsolete.

[Source: McKinsey Small Commercial Insurance Buyer Survey, 2015)

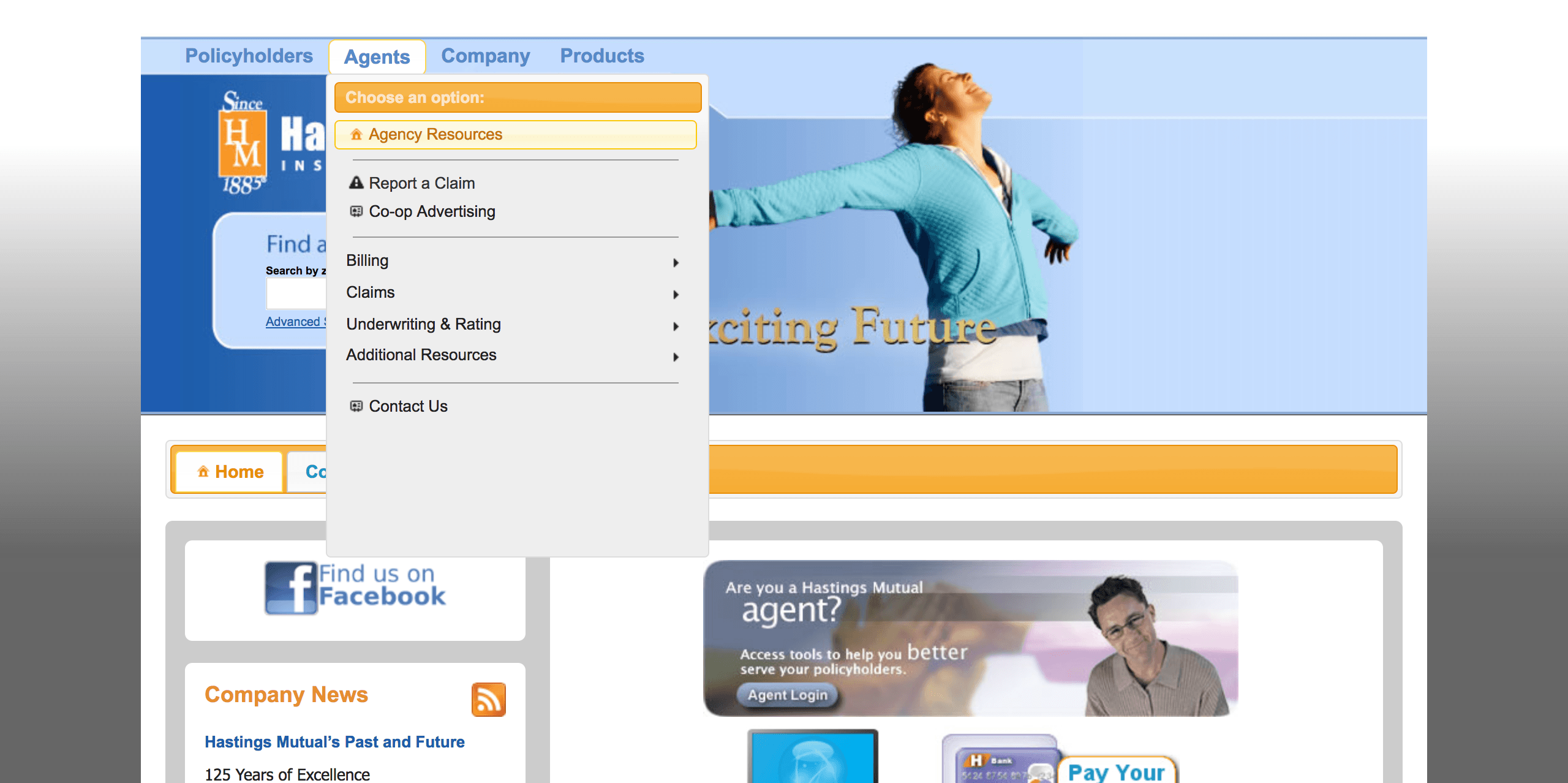

Hastings has over 600 independent agents across the mid-west region [2]. To buy insurance from Hastings, Business owners must deal with an agent and answer tens of questions. Digital competitors like biBERK, Berkshire Hathaway’s online insurance seller launched in 2016, allows business owners to buy insurance directly online, answering only a handful of questions, and receiving a quote in under 5 minutes [3]. biBerk uses machine learning to analyze historical claims data to identify the application questions that are most predictive of loss. It then further reduces the number of questions by drawing data from third party sources [4]. For example, instead of asking a customer for the year an office building was constructed, this information can be automatically drawn from a deeds registration database available to the public. Larger insurance companies are making multi-million dollar investments in technology to keep up with the changing customer demands for online direct-to-customer channels. Mid-size players like Hastings just simply do not have the financial horsepower to respond [5].

Having said that, Hastings has made smaller investments in digitization. It has tried to improve the speed of delivering a quote to customers by implementing an online agent portal. The online portal allows agents to submit an application, interact with Hastings underwriters, submit claims, and access other resources [2]. Hastings relies on its independent agents to generate a business pipeline and are therefore the central part of the selling process. Independent agents work for commission, so if Hasting’s system generates quotes and services customers faster than its competitors, agents are more likely to select Hastings. While it does not enable Hastings to respond to online direct-to-customer disruptors, it does make Hastings more competitive among its peers.

[Source: https://www.hastingsmutual.com]

In the medium term, Hastings can also take advantage of machine learning to reduce the number of questions business owners are required to answer. If agents spend 5 minutes to generate a quote from Hastings, and 5 hours from its competitors, he or she will choose Hastings every time [6]. This effort is a sub-million-dollar investment and even cheaper if Hastings has in-house data scientists and IT talent. If it has the resources, Hastings could go even further to leverage third party data sources to auto-fill questions, thus further reducing the number of questions customers (and agents) need to answer [7].

The only risk of using machine learning for mid-size insurers like Hastings is limited historical claims data. Many of these companies sell less than 1 billion dollars in premiums each year [5]. It is difficult to understand which application questions are most predictive of losses if few claims have been placed before. My recommendation to Hastings and other mid-size small commercial insurers is to pool their historical claims data together so that they can improve the accuracy of machine learning analytics outcomes. They will also enjoy greater negotiation power with third party data providers to lower the costs. While this would not ensure mid-size players withstand digital disruptors like biBerk, it would prolong their existence.

Digitization is rapidly disrupting the insurance industry, leaving the mid and small size players most vulnerable. While these players can slow the disruption by pooling together data and leveraging technological innovation, several questions remain:

- To pool together data to improve machine learning analytics outcomes, insurers would need to share claims data with their competitors. Do the benefits outweigh the risks?

- Using machine learning to reduce the number of application questions and leveraging third party data sources come with risks (e.g., inaccurate third-party data). It is likely digital players like biBerk will therefore need to sustain higher number of losses. Is this a viable business model?

Word count: 779

[1] What’s the Business Insurance Application Process Like?

http://www.businessinsurancenow.com/business-center/business-insurance/application-process/

[2] Hastings Mutual Insurance Company

https://www.hastingsmutual.com/

[3] Berkshire Hathaway Goes Small with biBERK Online Commercial Site, Insurance Journal

https://www.insurancejournal.com/news/national/2017/05/10/450433.htm

[4] Berkshire Unit Prepares to Sell Insurance Direct to Business via Internet, Insurance Journal

https://www.insurancejournal.com/news/national/2015/12/11/391593.htm

[5] Small Commercial Insurance: A Bright Spot In the U.S. Property- Casualty Market, McKinsey

https://www.mckinsey.com/industries/financial-services/our-insights/small-commercial-insurance

[6] Small-business insurance in transition: Agents difficult to displace, but direct sellers challenge status quo, Deloitte

[7] Digital Disruption in the US Small-Business Insurance Market, Boston Consulting Group

From my experience at a Fortune 500 insurance company, most customers view these products as commodities. I think there are a few areas for possible differentiation, which I will walk through briefly. These are:

PRICE

A competitive price is critical since these are products that people never want to buy and which often don’t seem different from competitor offerings. However, unlike a tangible good, the actual “COGS” will not be known until the duration of a policy or rate lock has expired. Selling at an irrationally low price has allowed many companies to hit sales goals, but it has caused massive profitability issues just a few years down the line. Setting the right price is dependent on having great, principled underwriters and on having the right set of data that you trust. To this latter point, claims data is a differentiator and you need to rely on its efficacy. Pooling data removes both of these advantages.

EASE OF DOING BUSINESS

As you point out, this is also critical when you think of both the independent agent and the end customer sitting around waiting for quotes. Hastings needs a better, faster interface. They need to use their historical data to determine the smallest number of indicators that they can use to achieve efficient pricing. Then they need to make as many of these answers automatic as possible (like the origin of the building example used above), so as to come close to eliminating the burden on the customer. Hastings may be in a tough spot because they don’t have the money to make investments. But I’d also say that the internet start-ups you describe likely also need(ed) to raise funds to design their initial software. Ironically, the big companies are the ones that feel most hamstrung because they have their decades of data and processes locked up in legacy systems that have been combined through mergers and acquisitions over the years. The big companies have the resources, but they have a confounding complexity of existing piping that drives their business. Smaller companies may actually be in a better place to make the needed transformation.

TRUST

An insurance product is nothing less than a promise. You can’t see it or pick it up, but people are paying money and giving their data so that you can fulfill a promise. If you cannot pay the claimant when they deserve it (say irrational pricing ends up bankrupting you), or if a consumer’s data gets in the wrong hands (if you pool inappropriately with external carriers), you have done a significant disservice to the people who were explicitly counting on you.

For all of the reasons mentioned above, I would not pool data with other carriers, and I would look for external funding to help us develop the quoting and service interface that will keep us competitive not only with our current peers but with the emerging ones.

Traditional insurers are very much at risk due to new fintechs exploring the insurance business like Trov, Gather, Friendsurance, etc. Nonetheless many of the big traditional players have quickly responded up-ing their game in the digital world like Geico and Progressive. Companies like Allianz and Hartford have the leading efforts in digitalizing the small commercial insurance scene offering quoting and underwriting online in a very simple process. Even though the purchase of commercial insurance is now made to be simple Small Business Owners still feel the product itself is very complex and hard to understand (What is covered? The meaning of technical terms, etc.) What I believe the big traditional companies can use to their advantage is their wide agent network, call centers and branches to create an omnichannel experience to ensure a great customer journey where all questions can be answered.

Traditional Insurers with great digital offers for Small Commercial Insurance

https://www.thehartford.com/business-insurance

http://allianz1business.allianz.it/#/

ttps://www.hiscox.com/

Warren Buffet is a smart guy and he has made a lot of money as a result. While I agree with Daniela that it’s possible the wide agent network could be an advantage to a traditional company, I think it is more likely that that network (and more importantly, the people that are a part of that network) will be a hindrance. Insurance has typically been a services industry and I think it will be very difficult for a management team that has “grown up” in the traditional insurance industry to see and act on the fact that insurance reps may not have a place in some customer segments given the rising alternatives. Change management is hard and emotion and experience bias are difficult to overcome so while all of the data might be clear that some segments would be better served by solutions such as biBerk, my guess would be that traditional insurance companies won’t adapt fast enough to beat out rising digital players.

Very interesting, and lots of good parallels to the development of the SMB online lending space. While I agree that SMB insurers offer a strong value prop to business owners, I think the conclusion that you’ve drawn – about mid-sized insurers inevitably dying off – is a bit draconian.

Proponents of the online lending space drew similar conclusions a couple years ago about community and regional banks’ abilities to respond to marketplace lenders offering a less cumbersome application process. What industry observers have seen, however, over the last year is that smaller incumbents have actually built their own online capabilities faster than expected (we’re doing a case on one such MA-based community bank in Entrepreneurship Management this spring). One way to do so here without significant upfront technology costs is to license white-label or co-branded online application services from a sort of “insurance-as-a-service” company. (If such a company doesn’t exist yet, I might start it 😉 )

To respond to your last question, I’d also be curious about whose balance sheet the insurance liability actually sits for digital insurers. If it sits on the balance sheet of an upstart digital insurer, you’re in essence asking the VCs to subsidize high losses rather than exercise underwriting discipline from the onset. On the other hand, some upstart digital insurers are partnering with large insurers or reinsurers including Hanover Re and Munich Re to use their balance sheets; I do not think these companies will tolerate significant upfront losses on claims to accumulate data for future underwriting models.

McKinsey is build this exact insurance-as-as-service platform and white labelling it. However, the integration costs are super high because all these mid-sized (and large sized) insurance carriers have legacy technology systems at that are also all different from each other. Its tough for white labels to enter this space and offer any cost advantage to bespoke solution providers, given the high integration costs that will be incurred with each new customer (not to mention months of pain staking wire connecting!)

I love this topic and think that small insurers are definitely at risk in the digitization age. Just as millennials are moving toward online shopping and online banking, millennial business owners will come to expect easy, almost-instant online procurement of their business insurance plans. The fact that Hastings has moved toward an online portal is promising, as it indicates that they can begin to collect data on their customers. Even without historical data, starting off with increased risks and decreasing those risks over time as more data is gathered would be wise on their part to keep up with the modern age. Although they will likely incur more costs due to risky businesses, some of these can be offset buy the decrease (and even eventual complete phase-out) of agents. As they train their data, business defaults will also decrease. I see their switch to digitization and AI as an investment into their future and definitely a necessity.