Google’s Chromecast: Masters of Scale

How the Chromecast captured an estimated 22% market share of OTT streaming devices in under three years.

In July 2013, Google launched the first generation of the Chromecast, a compact hardware device that connects televisions to wifi to enable streaming of digital media from users’ phones to their TVs.

The Chromecast was designed to compete with other media streaming devices including Roku and Apple TV as well as smartTVs and connected gaming consoles. Google identified media streaming devices as a channel that would attract users to the company’s larger services ecosystem on the biggest screen in consumer’s households. By creating a software platform around the hardware device, Google brought users into the virtuous flywheel of their many platforms and services including the Chrome browser, YouTube, Google Play apps, Google Photos, and Google productivity software.

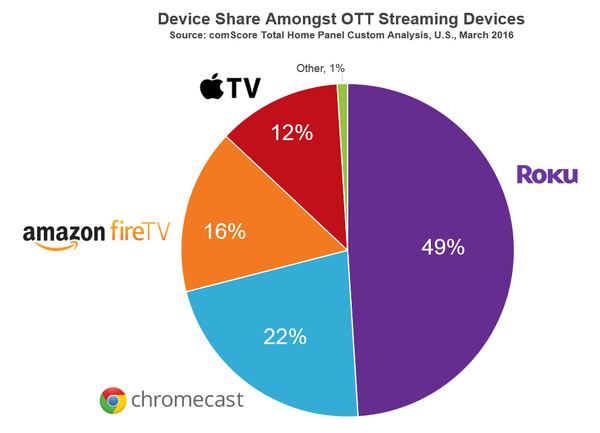

The Chromecast sold out quickly after its launch in 2013, and as of July 2016, over 30 million Chromecasts have been sold (across generations of the device). Google made strategic decisions in order to gain significant market share in the digital media streaming device market (which in 2013 was dominated by Apple and Roku). As of March 2016, Google had approximately 22% market share. Let’s take a look and see how they got there:

First, Google set the price of the Chromecast at just $35, which served as an accessible entry point for non-consumers of digital media streaming devices. This revolutionary price point was significantly below the retail price of Apple’s and Roku’s competitive devices on the market.

Second, Google placed a strong bet on the Chromecast user interface (or lack there of). Instead of building a new operating system for Chromecast and providing a remote for navigation, Google used the existing and familiar smartphone ‘s interface as the remote for Chromecast. User’s “cast” video from apps on their phone onto the TV. This enabled a very friction-less onboarding process for new Chromecast users. Further, Chromecast is operating system agnostic as it is compatible with iOS and Android devices. This operating system compatibility reduced barriers to adoption for consumers – anyone could use a Chromecast regardless of their existing smartphone ecosystems.

Lastly, Google began to license the Chromecast technology to TV and speaker OEMs. These OEMs licensed the ability to use Chromecast to connect the devices they manufacture. While these devices would compete for the same users as Google’s own Chromecast, this strategy would allow Google to reach as many consumer end points as possible (and therefore bring as many users as possible onto Google’s existing services and platforms).

Google also focused on building a content ecosystem around the Chromecast device, connecting users with many verticals of content providers. Upon launch, Chromecast leveraged Google’s existing platforms, including the Chromecast browser, YouTube, and Google Play apps. Focus on these services strengthened product engagement with existing Google users. Further, including these apps out of the box with the Chromecast increased new user acquisition. Google also attracted users to the Chromecast platform by launching the product with partnerships with key content providers such as Netflix, Hulu, HBOGo, and Pandora. Over time Google added thousands of more Chromecast-compatible content apps within many verticals to ensure users stay within the Chromecast ecosystem because they can access the broadest and deepest range of content.

While the strategic decisions surrounding the Chromecast drove user adoption, the team did not adequately solve issues around virality, network effects and multi-homing. While there are indirect network effects between users and content providers, there are not strong direct network effects between users. Google could attempt to solve for this by leveraging user watching behavior insights to create a recommendation engine for content based on a user’s activity and preferences.

Further, the cost of the Chromecast is very low, which does not bode well for consumer switching costs. At most a third of the cost of an Apple TV, the Chromecast could serve as an additional device to the Apple TV, Amazon Fire TV stick, or Roku.

By investing in Chromecast’s hardware and software capabilities, Google may be able to increase switching costs for users through the Chromecast Ultra, which is positioned as a premium product ($59).

References:

https://www.comscore.com/Insights/Blog/Roku-Leads-OTT-Streaming-Devices-in-Household-Market-Share

http://www.recode.net/2016/7/28/12318412/google-30-million-chromecast

Great post Michelle, thank you! Google did indeed do a remarkable job gaining marketshare in this highly competitive space through low-end disruption and tight integration within and across platforms. I agree that multi-homing will continue… do you think it’s possible/likely for one digital media streaming device to win? Or does the fragmented nature of high quality content production (i.e. many great producers) suggest there will be a longterm fragmented market of streamers? If Chromecast/FireTV/AppleTV is in fact an ancillary, data-collecting initiative for Google, Amazon, Apple, etc. that feeds into their larger strategies, perhaps they will be fine with low network effects and high multihoming? In short, I wonder if there will be a winner-take-all situation.