Bringing Mortgages into the 21st Century

Wells Fargo must adopt new technology to maintain leadership in the mortgage market.

For most people, purchasing a home is the largest and most important purchase decision they will make in their life. These are long, highly considered purchase processes where various constituents of the value chain (e.g., real estate agents, lawyers, loan officers, mortgage underwriters, appraisers, inspectors, closing agents) are involved and earn fees for their services.

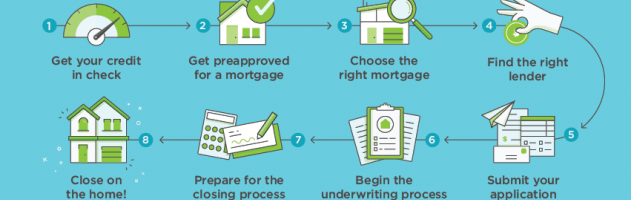

Many pieces of the process have been digitalized to increase efficiencies and reduce the overall cost to serve customers. Think of how far the process of simply searching for houses has come thanks to the innovation by Zillow/Trulia and the like. The mortgage process (graphic below) [1], however, is still behind the times, largely due to the complex and manual closing process (steps 7 & 8). Why has the closing process not been digitalized? Can digitalization make the home buying experience easier and more efficient for consumers? Is digitalization in the best interest of lenders?

It’s hard to understate how massive the home mortgage market is. Total mortgage originations in the United States are estimated to have reached $1.9 trillion in 2016. Wells Fargo is the current leader with approximately 13% market share, or roughly $250 billion of originations in 2016 [2].

There have been talks for a long time of “eMortgages” and “eClosings,” where the process could be fully digitalized from start to finish, but this vision has not come to fruition… until recently. The first-ever fully digital mortgage closing took place on July 28, 2017 [3]. This was made possible based on the digitalization of the arcane yet essential act of notarization. “A notary’s duty is to screen the signers of important documents for their true identity, their willingness to sign without duress or intimidation, and their awareness of the contents of the document or transaction.” [4]

The purpose of the notarization process is to deter fraud. In the past, notaries were required to be physically present in the room at the closing. Many lenders, including Wells Fargo, actually elect to pay for notarization on their customers’ behalves, to mitigate risk and reduce the friction customers face in an already complex and expensive process. When you’re doing millions of mortgage originations each year, you can imagine this being a material cost center for Wells Fargo.

Given recent technological innovations and regulatory changes, a notary is no longer required to be physically present at the time of closing. Notarize, a Boston-based start-up, has brought an innovative product to market to finally deliver on the vision of fully digital closings. Notarize’s mobile application enables people in all 50 states to have a document legally notarized from their smartphone or tablet via webcam, 24 hours per day, seven days per week. [5]

This was made possible due to a change in the regulatory landscape. On July 1, 2012, Virginia became the first state in the U.S. to authorize remote online notarization, which officially allows a signer in one location to have his or her signature notarized electronically from another location. Since then, four additional states (e.g., Ohio, Texas, Nevada, Montana) have also authorized webcam notarization, with many other states in the process of consideration. [6]

The digitalization of the notarization process is an extremely important innovation for mortgage lenders and borrowers alike. With many waves of technological innovation, an opportunity for market leaders (like Wells Fargo) to be disrupted by smaller, more nimble competitors is also created. Lenders who can offer modern, digital processes to reduce friction and provide an overall more efficient closing experience will have a significant competitive advantage over others who cannot. This of course also provides a more streamlined experience for the lenders who are now able to save on costs and time, which has a direct impact on their top and bottom lines. [7]

Wells Fargo has yet to adopt this technology into their processes. As the market leader, Wells Fargo should not only adopt but lead the transformation in this space, which will improve their financial performance and ensure their competitive moats are maintained longer-term. Furthermore, the benefits of digitalizing the notarization process extend far beyond mortgages. More than 1.25 billion documents are notarized each year in the United States, affecting lenders, title companies, law firms, private wealth firms, virtual mail providers, among many others. [8] Given Wells Fargo’s broad product portfolio, their investment in digitalizing this part of the contract process could have an extensive effect on their business. However, given these advancements are still relatively new to market, how should Wells Fargo’s management think about implementation with respect to risk mitigation and the varying nature of consumer comfortability using technology?

(762 words)

Sources:

- “How to Get a Mortgage.” How to Get a Mortgage, NerdWallet, 10 Aug. 2017.

- MBA Mortgage Finance Forecast. Mortgage Bankers Association, 2017, MBA Mortgage Finance Forecast.

- “The First-Ever All-Digital Mortgage Closing.” Wall Street Journal, 11 Aug. 2017.

- What Is a Notary Public? National Notary Association, www.nationalnotary.org/knowledge-center/about-notaries.

- Notarize – Bringing Notary into the 21st Century. 4 Feb. 2016, notarize.com/blog/notarize-bringing-notary-into-the-21st-century/.

- Another State Says Yes To Webcam Notarizations. National Notary Association, 21 June 2017, www.nationalnotary.org/notary-bulletin/blog/2017/06/two-states-approve-webcam-notarization.

- EClosings Fact Sheet. Fannie Mae, www.fanniemae.com/content/fact_sheet/eclosings-overview.

- Putting Trust Back into Notarization. Notarize, 9 June 2016, notarize.com/blog/putting-trust-back-into-notarization/.

Really interesting to see the mortgage process broken down like this. I had heard of companies/startups like Clara and Rocketmortgage looking to digitize the process, with varying degrees of success. And it seems Zillow and Trulia have had some success at the top of the funnel. Clearly the process of digitization depends on both technology and regulation in this space, but if I’m Wells Fargo or any other company involved in this process I’d definitely also be looking at to what extent there can be tradeoffs between digitization and consumer trust. The notary may be more of red tape for the consumer, but if Wells Fargo were able to fully digitize other parts (such as choosing the right mortgage, or getting preapproved), are customers comfortable conducting more and more of the process online or from their phones? Or will people always prefer to work with a real individual in a physical environment for some aspects of this purchase?

Very informative article. I’m intrigued by the

I’m intrigued by the premise of digitizing the notary process but I worry that consumer adoption might be hindered by concerns about safety and security particularly around how to safely transmit and remotely share sensitive documents. And, as I think about more general uses for this new technology, I also worry that differences in web authorization by state could cause issues for consumers engaging in cross-state transactions such as the transfer of a car title from one person to another. However, given the volume of documents notarized each year, the potential for transformative change is huge so I look forward to seeing how firms like Notarize and others continue to innovate.

While the transformational power of digital notary services is undeniable, I worry whether an institution such as Wells Fargo is best suited to be an early adopter of such services. First is the concern for security. The product is new and relatively untested. Wells Fargo, who handles millions of closing, could put many of its customer to risk if the service somehow gets compromised. Second is the question of adoption – it’s not just enough that Wells Fargo provides the digital notary service, it will have to convince customers to also be an early adopter. While doing so could differentiate Wells Fargo from the competitor, it will require dedicating significant resources, perhaps away from the in-person notary they are currently providing.

May Wells Fargo can segment the roll-out to first target the digitally savvy customers, who have Wells Fargo mobile app, deposit checks online, etc. and phase-in other customers as the services gets more mature and use (and abuse) cases more fully played out.

As someone who has experience with the home-buying process and mortgages, simplifying the notary process would be a huge win for a number of reasons, many of which you listed above.

Two major thoughts came to mind when reading this analysis. The first is how slow government can be to allow new technologies to disrupt regulated industries. Although there have been a few states that are allowing webcam verification, I wonder how slow the rest of the states and federal government will be to allow this. I also thought about other technologies that might be used to make e-verification even more secure than an in-person notary. Bio-metrics is the biggest one that comes to mind — using iris-scanners, face-mapping, and fingerprinting technologies.

After reading the Wells Fargo case in class, I wonder how the company thinks about being a market leader vs a follower. I had the opportunity to work at a large US financial service provider prior to business school. Following the financial crisis and the penalties that we faced as a company, we adopted more of a follower mentality. There was an unspoken rule to be conservative. Although I personally did not agree with this approach, in some ways, I understand the root cause. In the case of notary adoption, I completely agree that it enhances the customer experience and should be adopted by Wells Fargo. However, the question, in my opinion, is “should Wells Fargo be the innovator or imitator. As the second mover, it can leverage the experiences of the first mover (which may be start ups) and mitigate risks to its brand and potential share price if there are challenges along the way.

I thought this was a really interesting article; I had always wondered what the true purpose of a notary was beside making any sort of paper work a giant hassle. It is a shame that it has taken this long for webcam technology, which has been available inexpensively, to be used for such a headache of an issue. I do however think that there are risk for notarizing documents like wills and powers of attorney but I think if they can get the technology and the ethics around the technology right this is a huge market.

I agree with your point that it behooves Wells Fargo to adopt this new technology. I would certainly be incentivized to use a mortgage company that did not require he complex physical notary process. It gives borrowers with approved credit history’s the ability to act quickly and decisively.

Thanks for sharing Mike! The rise of technology certain presents numerous dilemmas between the efficiency and safety that occurs during transactions especially in the home buying market. I believe ultimately technology will win out, for better or worse. Do you see Wells Fargo buying out a company like Notarize or developing the same technology in house? I think a multi step verification process is essential to the success of these platforms. Do they utilize finger print or face recognition software? Thinking one step further, are we headed to a world where our phone act as not only our primary computer but as our primary form of identification and transaction?

Great article, Mike! The mortgage process certainly seems to be an area ripe for technological disruption. It’s interesting that this startup has devised a solution for the notary component of the mortgage process, as it seems to be a relatively low-time endeavor with massive downside if a mistake is made. I can imagine management at Wells Fargo (and potentially even consumers) are uncomfortable with upending a process that some view as essential for anti-fraud and security. How can consumers and lenders be sure that this technology is impervious to hacking or malware? In any case, it’s interesting to see how much digitalization has enhanced the homebuying experience overall. Websites like Trulia have enabled consumers to view price history, features, etc. of homes with a level of transparency and granularity that should make the market more efficient overall.

To Viper’s comment, I wonder if acquiring Notarize may actually be a very good move for Wells Fargo in this scenario. I was also wondering while reading the article what the best approach would be. The reason I think bringing Notarize in-house and then building it out to be customized to maximize utility for Wells Fargo might be the way to go relates back to our case on United vs. Asahi. United relied on external providers to build out advanced technology and machinery, which certainly helped them but then allowed these providers to go sell this same technology to competitors like Asahi. I think if Wells Fargo wants to be first-mover in this space and really take advantage of being the only ones to deliver a more seamless experience for customers, they should try to own the technology as much as possible. Otherwise, Notarize may provide a customized solution for them and then sell a very similar product to Wells Fargo’s competitors.

Thanks Mike for the thoughtful and well-articulated piece. While I agree that the digitized notary experience is the future for this space, I would push back on the assumption that Wells Fargo needs to lead this charge or focus a lot of attention here. There appear to be so many more pressing and near-term opportunities for digitization along the mortgage process that could have more substantial cost savings. The mortgage timeline is still around 50 days, and the process is very human capital intensive, costing $8,000 per completed mortgage [1]. In addition, individual sales agents are originating more loans on their own than some of the leading online brokers out there, which leads me to believe there are areas further up the chain from closing to focus on [2].

That being said, it obviously behooves Wells Fargo to pay attention to this part of the chain, and it appears they have to some extent already, naming Pavaso, a provider a digital process and collaboration solutions for real estate, as an approved vendor for eClosings in May 2016 [3]. And, if they are going to continue down this path of digitized closings, it may make sense for Wells Fargo and other mortgage players to look into blockchain technology as a source of verification. That may be an even longer regulatory approval march, but certainly a more cost-effective and secure method.

[1] Ellie Mae, “Origination Insight Report”, June 2016. , Accessed November 2017.

[2] LaRue, Aaron, “Why startups can’t disrupt the mortgage industry”, TechCrunch, posted Apr 21, 2016. , Accessed November 2017.

[3] Swanson, Brena, “Wells Fargo’s Pavaso approval brings digital mortgages a step forward”, Housingwire.com, May 31, 2016. , Accessed November 2017.

Digitalizing the notarization process could certainly streamline the complex and convoluted mortgage process. Importantly, your article highlights the need for digitalization more broadly across the financial services industry. However, I’m left wondering two things. First, is this truly a cost center for Wells Fargo? Said differently, do banks pass along the cost of notarization to the consumer? If so, this may be a contributing cause to the inertia to adopt this new technology. Second, in the context of mortgages / home buying, is the notarization process truly a “headache” for consumers? Securing title insurance as part of a new mortgage is also a relatively inefficient process. However, relative to the other steps in the home-buying process (e.g. choosing the real estate, finding your mortgage lender, etc.), getting title insurance (and potentially notarization) seem less ominous. This could be another limiting factor in the adoption of technology in this part of the supply chain – consumers are simply not sufficiently fussed to incentivize greater efficiency.

Thanks for a great article Mike. I find this super interesting and to Bo’s comment above: I totally agree that there is more time and money to be saved in making the overall mortgage process more efficient and less human capital instensive, and that’s exactly what some AI/Machine learning solutions are looking to do. One concern I have in this trend towards digitization is that of security, given the recent Equifax breach, how comfortable would you be in having digital documents and records for your home, that were notarized over webcam, and how do you protect the process from fake signatures etc. There’s a whole e-mortgage ecosystem developing with companies such as Approved.com, Roostify.com and countless others, so my real question is what’s your plan of action, and when do we go pitch to VCs.