Square’s New Circle: Banking on Data

Square brought small business payment terminals into the modern day. The simple, clean Square dongle has become widely recognized as the icon of new-age payment. Now, the company is eyeing its valuable set of transaction data to make loans. Square’s visibility into otherwise secretive transaction data allows them to loan to business owners on the basis of business performance.

Could this be the future of lending?

Square

Jack Dorsey transformed payments with the introduction of Square in 2009 [1], after launching social media giant Twitter. Square turned convoluted, outdated payments systems into simple, smart payment processing. As the value of its underlying transaction data increased, Square was presented with a unique opportunity to leverage the data for a new line of business: merchant loans.

Jack Dorsey, CEO of Square. (Source: https://news.coinsquare.com/digital-currency/jack-dorsey-square-cash/)

Jack Dorsey, CEO of Square. (Source: https://news.coinsquare.com/digital-currency/jack-dorsey-square-cash/)

Using Machine Learning to Generate Revenue

Why Square Capital Works

Square’s core payment processing is a competitive and low margin business that requires economies of scale to grow. The success of their payment terminals generated a large set of transaction data, which can be used to diversify their offerings to merchants and grow their revenue base.

One of Square’s most profitable endeavors has been Square Capital, a new approach to small business lending [2]. Traditionally, small business owners would seek out banks or family & friends to provide growth and working capital loans. Square’s bet is to use machine learning to predict which businesses are most likely to pay back loans, make those loans, then close the loop by automatically collecting payments from the merchants through the Square platform.

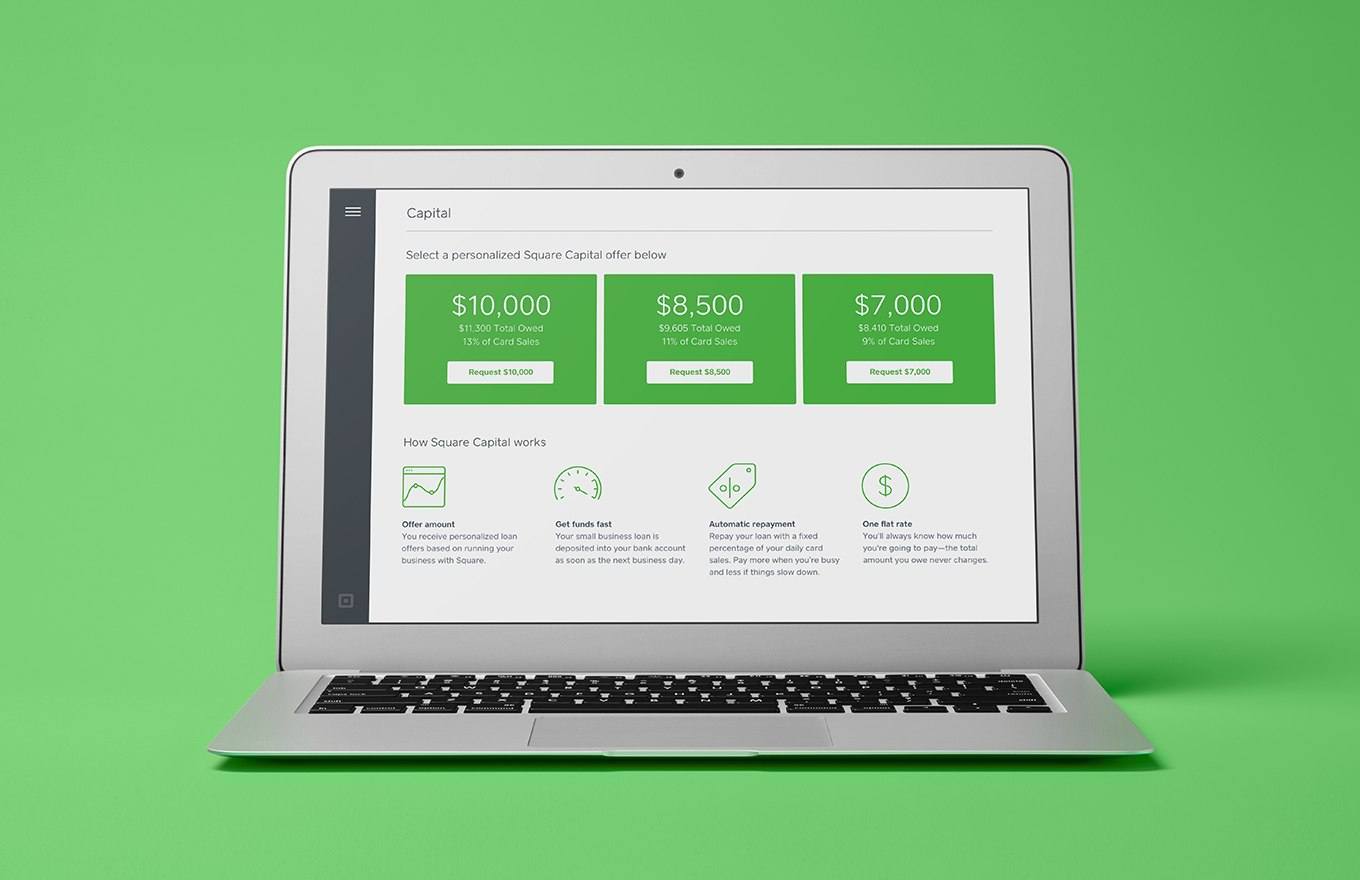

How Square Capital Works

Square’s former Head of Data Science, Thomson Nguyen, says the company’s advantage is their ability to provide a fast, flexible, and seamless funding experience [3]. Square’s team of data scientists use their proprietary set of transaction data as a leading indicator of credit worthiness, generating models to surface potential borrowers [4].

Using Joe’s Pizza as an example:

- Joe’s Pizza uses Square to collect payments for pizzas

- Square sees steady revenue growth and makes a pre-approved offer

- Joe takes a $120 loan at a 10% rate

- Square automatically deducts 2.75% payment processing fee & $10 from every $100 in sales

- Process continues until Joe has paid back the $120 loan

Square stands to make safer loans than traditional lenders who have far less visibility into Joe’s business. This creates a positive feedback loop which further enhances Square’s learning model for future loans.

Square Capital lending platform. (Source: https://squareup.com/)

Continuous Improvement Using Networks

Beyond direct loans, Square also adds value to merchants and potential borrowers by providing insights on how to improve pricing and operations [5]. Using their large database of aggregated knowledge, Square could suggest to Joe the pricing benchmark for his neighborhood is $3.50/slice. This knowledge-share is a win-win proposition, as a growing merchant base will result in a bigger set of potential borrowers.

The company is also seeking to leverage network effects within their community. Similar to lending, machine learning can be used to identify efficiency opportunities by matching up businesses within the Square ecosystem (Joe’s Pizza can get a discount from Sarah’s Sauces). The ability for Square to facilitate collaboration among its businesses can be very powerful at scale.

Moving Forward

In 2017, Square filed to be a bank with the FDIC to be able to fund loans using deposits [6]. However, they withdrew their application earlier this year in an attempt to strengthen the application [7], indicating machine learning alone is perhaps not enough to be the foundation of a sustainable banking system.

In the short term, management should consider augmenting their dataset with data available elsewhere. For instance, they can bring in external weather, holiday, trend, and census data to further improve the accuracy of their model. Thinking ahead, if Square’s goal is to eventually be a bank, they need to figure out how to loan to merchants outside of their ecosystem. As fellow payment competitors PayPal and Stripe move into the lending space [8], Square needs a strong and defensible way to protect their lending product. While Square holds an obvious advantage with their base of 2 million sellers [9], they need to think about how to form strategic partnerships to serve the broader multi hundred-billion-dollar small business lending market [10].

The final point of consideration is learning models are susceptible to real world swings, which can be incredibly difficult to predict. Square, like many financial technology companies, was founded after the 2008 recession and its models were not built to include macroeconomic trends. Large economic fluctuations could heavily affect discretionary spending, particularly at restaurants, bars, and small businesses, which make up a large portion of Square’s customer base. They should look to build in contingencies in case of system wide changes.

Future of Lending

Machine learning can help companies create entirely new lines of business. Square has strong potential to grow their business offerings through continuously expanding data sets. In Square’s pursuit of becoming a bank, can data alone be enough to reliably judge the future potential of a business? As a leader in the space, how should Square thinking about lending, capital, and credit outside of Square?

(785 words)

References

[1] Crunchbase (2018), “Square”, https://www.crunchbase.com/organization/square#section-overview, accessed November 2018.

[2] Square Inc. (2018), “Square Capital”, https://squareup.com/capital, accessed November 2018.

[3] Institute for Applied Computational Science at Harvard University (2017), “Machine Learning for Small Business Lending // Thomson Nguyen, Square Capital” https://iacs.seas.harvard.edu/event/machine-learning-small-business-lending-thomson-nguyen-square-capital, accessed November 2018.

[4] Berkeley Data Dialogues (2016), “Modeling Default Risk for Business Loans”, https://datadialogs.ischool.berkeley.edu/2016/schedule/modeling-default-risk-business-loans, accessed November 2018.

[5] Square Inc. (2018), “Data Insights”, https://squareup.com/townsquare/category/data-insights, accessed November 2018.

[6] Rudegeair, P. (2017), “Jack Dorsey’s Square Makes a Move Into Banking”, https://www.wsj.com/articles/jack-dorseys-square-makes-a-move-into-banking-1504737851, accessed November 2018.

[7] Witkowski, R. (2018), “Square Quietly Withdraws Bank Application”, https://www.americanbanker.com/news/square-quietly-withdraws-bank-application, accessed November 2018.

[8] Lunden, I. (2018), “Stripe is Testing Cash Advances, Following Square and PayPal’s Moves Into Business Finance”, https://techcrunch.com/2018/09/24/stripe-advance-cash/, accessed November 2018.

[9] Bloomberg Technology (2016), “How Square Capital Manages Risk”, https://www.forbes.com/sites/andyswan/2018/08/31/square-growth/#3c4005f0291d , accessed November 2018.

[10] Bloomberg Technology (2016), “How Square Capital Manages Risk”, https://www.bloomberg.com/news/videos/2016-04-12/how-square-capital-manages-risky-small-company-loans, accessed November 2018.

This is a great follow up to the question surrounding the value of POS data during the beer simulation game! In many ways, by directly understanding their consumers revenue sources, Square is best positioned to evaluate the viability of a potential borrower. My one concern with Square dipping its toes in this water is their lack of knowledge of activities outside of transaction data. If company X has an outstanding mortgage of $X, it won’t show up in its transactions data, but it does impact the long term viability of the company and potentially its ability to repay. Transaction data can tell you a lot about a business, but I’m hesitant to say it can stand on its own. If Square is serious about drastically scale its model, I think the company should utilize a few more non-transaction related data points in its process.

This is great!

I think Square’s strategy is brilliant and it is natural for the company to leverage the data that it is has. Your point on Square’s ability to improve its operations is actually quite pertinent and could definitely help companies in better forecasting and pricing strategies. It could also help companies to make more targetted offers to customers at specific times of the day, months, seasons etc. On the banking model, i am not sure how Square will be equipped to manage the regulatory compliances and treasury management so soon. There will be a lot of credit analysis that will have to be done beyond payments data. I am wondering whether it will be better to partner with banks and help them with disrburse loans rather than taking on the risk yourself.

I am so happy someone spoke about this. I think Square, Amazon, and other companies with large access to data are prime to capitalize on this information and offer lending (and other banking) products to businesses (especially in small and medium business).

In terms of whether data is enough, I think this data is Square’s and Amazon’s competitive advantage over traditional banks. In fact, many banks across the US (and globally) are scrambling to figure out ways to gain access to this data and be able to expand the scope of their lending services.

However, the real hurdles I believe will be 2: (1) in changing the mindset of SMBs to take up these lending projects (which currently they will since they’re being offered at good rates) but the second and more important hurdle is (2) when the banking institutions catch up and are able to access this data (by buying it, by aggregating it through potential consortia with other banks, etc) and begin offering better lending products, how will that affect Square and Amazon’s positions in these financial products? Or will Square’s speed to market make the banking industry’s foray into this irrelevant?

Exciting world to be in regardless!!

So cool! Really enthused that someone wrote about the intersection of machine learning and lending. To answer your question, can data alone be enough to reliably judge the future potential of a business: It depends on the stage and type of business. I think for high growth companies, like 42Technologies :), data alone is not enough to determine the future potential of a business. More qualitative measures such as the quality of the CEO and team are probably more relevant. For more stable / mature businesses, I suspect that data may get a lender 80-90% there. The final 10-20% will still be based on human judgment to understand the “character” of the borrower.

What I love the most about Square’s approach is the granular data that they are able to gather on SMB lending and credit performance in the United States. Despite the veneration of small business owners in the United States as the “backbone of the American economy,” there is a massive dearth of actual data on the disbursement and performance of SMB loans to businesses across the United States. It will be interesting to see how approaches using machine learning like Square will increase the efficiency of underwriting and servicing within this market.

Fascinating article. I do worry that the skill-set of being a bank requires a different skill-set and core competency (avoiding the 1% bad scenario) than that of an upstart tech company. I could see them doing better with all of their data at recouping investments, but curious within the cost bar the share that is due to “bad debt” vs. “customer acquisition” – which might be higher at least initially if they start with less credibility as a bank. I wonder if there’s a way that Square could leverage their technology but offload a greater share of the loans to third parties. This would also allow Square to maintain it’s relatively capital-light business model (vs. all the capital you’d need to have if you were a lendor)