Every day, people are got killed or injured on the road. National Highway Traffic Safety Administration (NHTSA) 2016 data shows 37,461 people were killed in 34,436 motor vehicle crashes, an average of 102 per day in the United States.[1] It has been a serious issue in the society and causing enormous financial risks for drivers since you cannot predict an accident.

The Vehicle Insurance Industry

Vehicle insurance was first introduced a long time ago to control such risks in the United Kingdom with the Road Traffic Act 1930.[2] But after more than eight decades of evolvement, the car insurance still implements the similar policy, which is to charge a predetermined premium to cover the potential losses caused in accidents during the coverage period. While the insurance company will give incentives to good drivers, who have not claimed accidents in certain period, by a discount of the quotation, the evaluation criteria is not sophisticated and lagged. A study listed the relationships between traffic accidents and the driver’s age, skills and the driving habits.[3]

But is there a more accurate and dynamic way to evaluate the risks? Can we utilize machine learning to conduct unsupervised learning to analyze data generated during the driving and predict the future risk?

“Snapshot” of Progressive Insurance

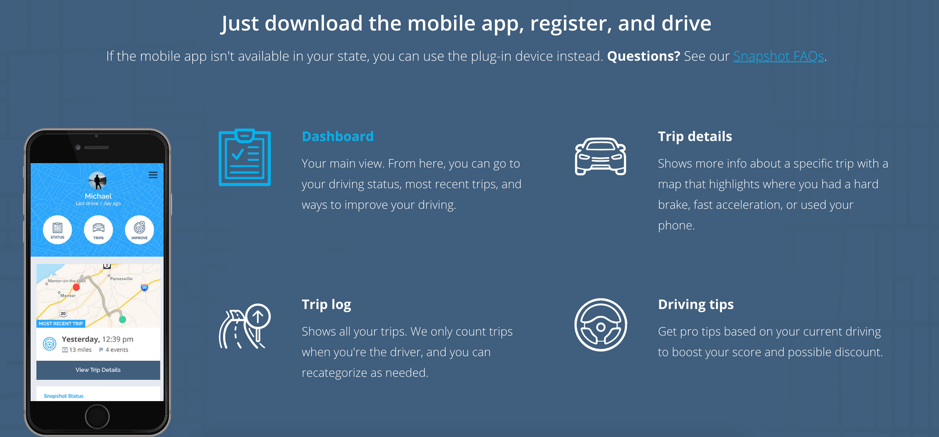

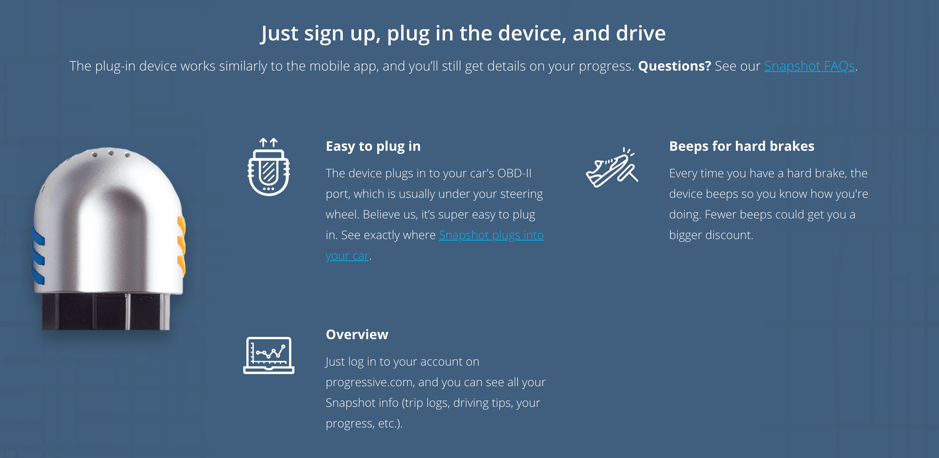

Progressive Insurance implemented a machine learning algorithms for predictive analytics based on data collected by Snapshot, a mobile app or a small plugin device in the car which collects the driving data during driving.[4] To encourage the use of Snapshot, Progressive offers “most drivers” an auto insurance discount averaging US$130 after six months of use.

With these customers’ benefits, Progressive Insurance claims that its telematics (integration of telecommunications and IT to operate remote devices over a network) mobile app, Snapshot, has collected 14 billion miles of driving data.[5]

By feeding the labeled data which correlate the accidents occurrence frequency with the accordant driving data, the insurer could obtain a pattern to predict a new customer’s possibility of causing accidents by simply gathering hours of his/her driving data. From a short term perspective, this practice could provide the company a metric to evaluate the customers, attract more “good drivers” to the insurances and, in turn, accumulate more data for more precise prediction which creates competitive edge.

Viewing from a longer term angle, the data generation process could encourage the drivers to monitor and optimize their driving habits, thus decreasing the entire accidents. As for the insurer, implementing further data science techniques, actuaries could obtain a wholistic view of the possible return and risk, driving them to make wiser investments.

Future Implementation

Data drives the future productivity and innovation.[6] Progressive Insurance could implement the “Snapshot” as an hub for the customers. Insurance companies like Progressive Insurance are highly regulated and, meanwhile, must process thousands of transactions and customer requests every day. This is the best scenario for machine learning technology to thrive.

For instance, the technology can make a huge contribution to reduce insurance fraud. The total cost of insurance fraud (non-health insurance) is estimated to be more than $40 billion per year. That means Insurance Fraud costs the average U.S. family between $400 and $700 per year in the form of increased premiums.[7] This number is only going up, and the overall cost of investigation rising with it. Machine learning is able to auto-validate policies by ensuring that key facts. Moreover, for the vehicle insurance, the “Snapshot” could feed accurate data to prove the claims. Once validated, this information can then automatically be fed into the downstream payment system and money sent in a matter of minutes without any human involvement.

Moreover, using the machine learning embedded Natural Language Processing technology, insurance companies could address the fundamental customer services without any human involvement, which largely reduces the labor cost of these insurance companies.

What’s Next?

Machine learning is the megatrend that will drive insurance companies to innovate their practices on Behavioral Policy Pricing, AI automated Customer Experience and Faster Claims Settlement. But how can insurance companies really connect the trillions of data to predict future? Will these systems be manipulated by customers?

Word Count: 789

[1] For the original NHTSA report for 2016, see https://crashstats.nhtsa.dot.gov/Api/Public/ViewPublication/812451

[2] “Road Traffic Act 1930”. www.legislation.gov.uk. Retrieved 2018-03-28.

[3] Berg HY., “Reducing crashes and injuries among young drivers: what kind of prevention should we be focusing on?” See https://www.ncbi.nlm.nih.gov/pmc/articles/PMC2563439/

[4] Snapshot program introduction, see: https://www.progressive.com/auto/discounts/snapshot/

[5] Accenture report “Machine learning in Insurance”, see https://www.accenture.com/t20180822T093440Z__w__/us-en/_acnmedia/PDF-84/Accenture-Machine-Leaning-Insurance.pdf

[6] Royal Academy of Engineering, UK report “Connecting data driving productivity and innovation”, see https://www.raeng.org.uk/publications/reports/connecting-data-driving-productivity

[7] FBI report, “Insurance Fraud”, see https://www.fbi.gov/stats-services/publications/insurance-fraud

Wow! 14 billion miles of driving data! It’s pretty impressive that Progressive has taken these steps to develop and implement their machine learning efforts.

Your article clearly articulated the business case and application towards the auto insurance industry. It also left me considering how Progressive might apply similar technology to other product lines (e.g., home, life, etc) and what the ethical implications are.

For instance, they could take activity data (e.g., FitBit / Apple watch) and combine with other inputs to better predict the health of individuals with life insurance policies. However, this application seems to have some sinister ethical implications. That being said, if they reward people for being “healthy” drivers with discounted auto insurance, should they reward people for healthy lifestyles with discounted life insurance?

Lots to think about – thank you for starting the conversation!

While I can definitely see the utility of this data, I also have some data privacy concerns. Could this data be subpoenaed for use in court against a driver? Would a driver be able to opt out of data collection, or would it become a requirement? From a regulatory and privacy perspective, I would want to know more about how the data would be shared between insurers, how it would be stored over time, and who would have access to it.

Thanks for sharing this interesting information! This is a really interesting use of machine learning, and I can see how it can be a competitive advantage for Progressive. While other auto insurance companies may not be able to tell a good driver from a bad driver – and therefore has to charge everyone an average rate – Progressive can actually change its pricing strategy to attract the good drivers because of its Snapshot data. Assuming consumers learn about this feature, good drivers will be incented to go with Progressive because they can afford to offer a lower price for insurance to those consumers

My concern would be the application of this technology in the health insurance space. Imagine a world where your health insurance company can access your fitbit or iphone health data to understand your eating and exercise habits, and adjusts your insurance premium based on that information. While most people can get over the fact that Progressive has tons of data about your driving habits, I think people would be more hesitant to accept health insurance companies having similar information about them