Kansas City Southern Railroad Blues

Kansas City Southern deals with making America great again and the NAFTA renegotiation process.

How do you navigate an increasingly protectionist/isolationist political environment within the U.S. when one of the primary aspects of your business is facilitating trade between Mexico and the United States? That is the question Kansas City Southern (NYSE: KSU, “KCS”, the “Company”) currently faces as the United States, Canada and Mexico begin renegotiations of the North American Free Trade Agreement (“NAFTA”).

“The NAFTA Railroad”

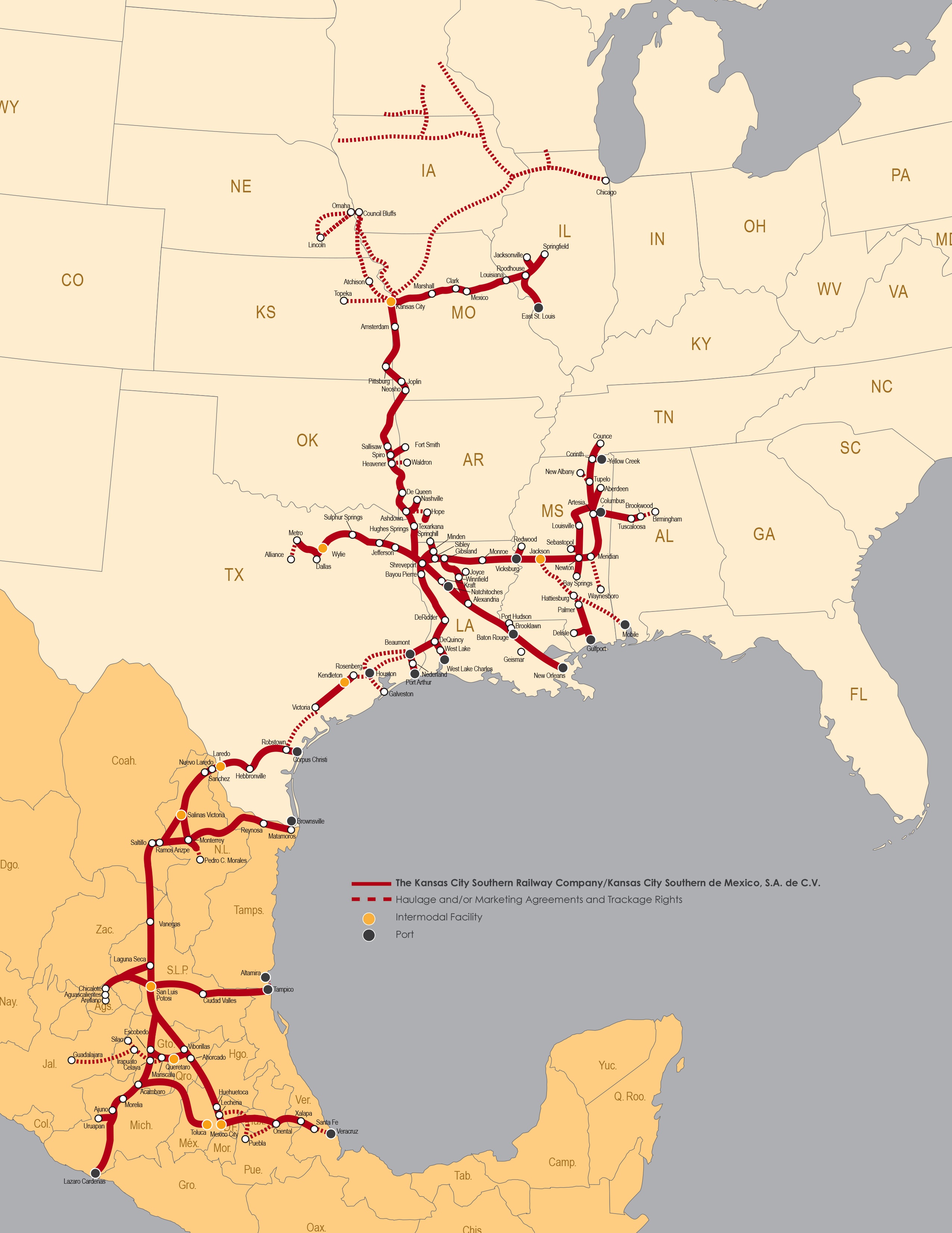

KCS is a railroad holding company with both U.S. and international operations with two primary subsidiaries: Kansas City Southern Railway Company (“KCSR”) and Kansas City Southern de México, S.A. de C.V. (“KCSM”). [1] Across all of the Company’s subsidiaries, KCS operates approximately 6,600 route miles of track, extending south from the Midwest and into Mexico, and maintains connections to all other Class I railroads. [1] See Figure 1 for a detailed map of KCS’s rail network.

Figure 1 – KCS Rail Network

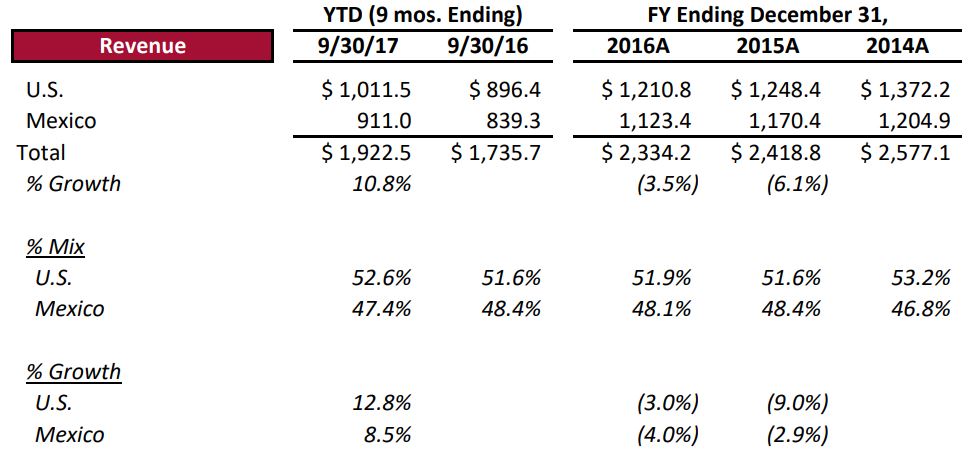

Notably, around 50% of KCS’s revenues are from the Company’s Mexico operations (see Figure 2 – KCS Historical Revenue Mix). KCS’s substantial exposure to the Mexican market is due to its KCSM rail operations, which operate the shortest passageway between Mexico City and Laredo, Texas. [1] The Mexican government granted KCS this essential corridor via a 50-year concession agreement in 1997 (expiry in June 2047; exclusive through 2027) – because of the agreement, KCS and Ferromex are the only Class I railroads that directly operate assets in Mexico. [1] Key terms of the agreement provide that KCSM has the “right to use, but does not own, all track and buildings that are necessary for the rail lines’ operation”, must pay a 1.25% annual concession duty on gross revenues, and adhere to certain investment commitments. [1]

With NAFTA’s passage in 1994 and the concession agreement signed in 1997, KCS went so far as to brand itself “The NAFTA Railroad” and remains one of the more interested parties in the NAFTA renegotiation process. [2] Investors certainly shared this sentiment with a drop in the Company’s stock price post-election from $92.55 to $82.48, erasing nearly a $1 billion in its market capitalization.

Figure 2 – KCS Historical Revenue Mix

“Personally, I Don’t Think We Can Make a Deal”

With the current administration’s approach to NAFTA vacillating from exiting the treaty to renegotiating the agreement in earnest but with limited confidence (Donald Trump – “Personally, I don’t think we can make a deal… I think we’ll end up probably terminating NAFTA at some point”), KCS has taken it upon itself to enter the political fray, advocating for sensible changes as it relates to the NAFTA renegotiation. [3]

Post-election, Pat Ottensmeyer, KCS’s CEO, was elected chairman of the strategic trade initiatives working group of the U.S.-Mexico CEO Dialogue, a U.S. Chamber of Commerce group aimed at facilitating a discussion between government officials from both countries with industry leaders. [4] [5] In this role, Ottensmeyer testified in front of the U.S. House of Representatives Committee on Way & Means outlining the benefits of NAFTA and recommending how the administration should approach the renegotiation, specifically emphasizing an expedient, trilateral dialogue which leverages existing amendment procedures. [6] Beyond interfacing with the government to ensure adequate reform, KCS has been proactive in engaging with its existing customers. [7] Thus far, conversations have been positive with KCS indicating that “…our customers in Mexico…have consistently asked us to keep making investments in Mexico, because they want to grow in Mexico, they want to invest in Mexico and they need us in order to grow.” [8] KCS’s investment in Mexico has totaled approximately $4.5 billion since 1997. [6]

Making Kansas City Southern Great Again

Given the Company’s stance on continued investment in its Mexican operations during the NAFTA renegotiation process, which is arguably required from a public positioning/competitive perspective, KCS should work to de-risk its capital expenditures (guidance of approx. $550mm to $560mm for FY17 on LTM 9/30/17 revenues of $2,521mm) by limiting its investment to projects where it can better share risk. [1] [9] [10] The Company’s investment of approx. $150mm in the Sasol yard is a great example of a de-risked project whereby KCS retains a lease revenue stream and is guaranteed both switching revenue on all of the carloads as well as a guaranteed number of carloads moving on the KCS network. [8]

Long-term, KCS should work to diversify its Mexican operation revenues by pursuing more MX-domestic revenue streams and customers. The Company provides limited explicit disclosure on the breakdown of its Mexico operation revenues between cross-border traffic and domestic traffic; however, the Company does provide disclosure on cross-border traffic revenues in the aggregate which is approx. $710mm over the most recent LTM period (albeit, this figure is understated due to it excluding traffic interchanged with a competing railroad at the border). [10] Cross-border revenues are most at-risk as it relates to NAFTA renegotiations – by further building out the Company’s MX-domestic revenue stream, KCS will decrease its sensitivity to NAFTA.

Open Questions

What other actions can KCS undertake in order to de-risk its Mexico operations from potential NAFTA interruptions?

[Word Count: 782]

- Kansas City Southern. 2016 Form 10-K Annual Report. January 27, 2017. https://www.sec.gov/Archives/edgar/data/54480/000005448017000007/kcs1231201610k.htm, accessed November 2017.

- Dornbrook, James. “KC Southern CEO: A lot at stake if there’s a ‘bad outcome’ on NAFTA.” Kansas City Business Journal, April 20, 2017. https://www.bizjournals.com/kansascity/news/2017/04/20/kansas-city-southern-ceo-ottensmeyer-nafta.html, accessed November 2017.

- Donnan, Shawn. “Donald Trump revives threat to pull US out of NAFTA.” Financial Times Limited, August 23, 2017. https://www.ft.com/content/cfdcec24-87c2-11e7-bf50-e1c239b45787, accessed November 2017.

- Stephens, Bill. “Railroads await specifics on Trump plans for taxes and trade.” Trains, January 20, 2017. http://trn.trains.com/news/news-wire/2017/01/20-hunter-and-ceos, accessed November 2017.

- Kansas City Southern. “Kansas City Southern President and CEO Ottensmeyer Tapped to Lead U.S.-Mexico CEO Dialogue Strategic Trade Initiatives Working Group.” U.S. Chamber of Commerce News, January 12, 2017. http://www.kcsouthern.com/media/news/kcs-news/kansas-city-southern-president-and-ceo-ottensmeyer-tapped-to-lead-u-s-mexico-ceo-dialogue-strategic-trade-initiatives-working-group, accessed November 2017.

- Ottensmeyer, Pat. Oral Testimony of Patrick J. Ottensmeyer, President and CEO, Kansas City Southern, Modernization of the North American Free Trade Agreement. July 18, 2017. https://waysandmeans.house.gov/wp-content/uploads/2017/07/20170718TR-Testimony-Ottensmeyer.pdf, accessed November 2017.

- Hutchins, Reynolds. “KCS tries to assure NAFTA-worried shippers.” Journal of Commerce, January 20, 2017. https://www.joc.com/rail-intermodal/class-i-railroads/kansas-city-southern-railway/kcs-tries-assure-nafta-worried-shippers_20170120.html, accessed November 2017.

- Kansas City Southern. Stephens Fall Investment Conference Transcript. November 8, 2017.

- Kansas City Southern. 2017 Form 10-Q Quarterly Report. October 20, 2017. https://www.sec.gov/Archives/edgar/data/54480/000005448017000171/kcs10q09302017.htm, accessed November 2017.

- Kansas City Southern. Third Quarter 2017 Earnings Presentation. October 20, 2017. http://investors.kcsouthern.com/~/media/Files/K/KC-Southern-IR-V2/quarterly-results/2017/q3-earnings/q3-2017-analyst-presentation-ksu.pdf, accessed November 2017.

Cycle Time — great post! Most discussions regarding isolationism focus on the companies that manufacture in one country and leverage an international supply chain to sell to consumers in another country. Lost in this conversation is the precarious position that the logistics companies facilitating this international trade are in, given the current climate.

In response to your open question, KCS can also de-risk its operations by identifying their largest American clients that currently manufacture in Mexico and may relocate operations to the United States (e.g. Ford Motors). By deepening these relationships, KCS could put itself in position to retain this business even if manufacturing moves to the States. KCS could go as far as advising these companies on potential US manufacturing locations (that conveniently still fall on the KCS railway line). Although the shipping distances will be shorter and therefore revenue will decrease, retaining these accounts is crucial.

Great topic and post!

If NAFTA is terminated or renegotiated to President Trump’s liking, there will likely be a drop in cross border trade. KCS needs to figure out a way to position itself to fill in this lost revenue with more US-US and Mex-Mex routes while still maintaining relationships with its leading cross-border customers, as a future administration could reinstate policies that promote cross-border trade.

I like that the CEO is taking an active stance in the ongoing negotiations. As the recent decline in stock price exemplifies, this is a material issue to the company’s value. I would advise that KCS form or rally existing industry groups that would be effected by NAFTA termination to publicly lobby the government to change course. Similar to the solar panel industry’s lobby against a potential tariff on imported panels, emphasizing domestic job and productivity concerns would be an attractive ploy

This is great. Had no idea the percentage of revenue coming from Mexico. Are there any high level estimates as to the % impact on the broader US economy and KCS specifically if NAFTA is pulled back?

I’m also curious if this would impact all the other big railroad providers (e.g., BNSF, UP) equally or if KCS has unique exposure to Mexico.

Great reading. It is very interesting to see how interruption in NAFTA would have tremendous consequences on KCS. I do agree with the fact that the company would be forced to focus on developing its operations in the US and in Mexico as two separate businesses for each local market, which would make few sense from a strategic and organizational standpoint and would incur significant restructuring cost. I would also expect a downturn in some sectors of the Mexican economy should trade with the US be drastically reduced, which would in the end make the railroad industry in Mexico not a place to be. I am thus very skeptical as for the future outlook for KCS, in a scenario of interruption of NAFTA.

An interesting analysis would be to look at KCS and firms like them pre-NAFTA, and how operations changed since then. I’m also curious what other things KCS would be able to accomplish through lobbying moving forward – specifically agreements that are less broad and sweeping than something like NAFTA, but maybe with specific countries like Mexico.

Kyle, well done. A masterpiece as always! I think your suggestion to increase the company’s focus on domestic operations would certainly be an appropriate step to take in the event that a NAFTA repeal seemed likely. Another approach the company could take would be to leverage it’s influence among its clients, who are ostensibly large multi-national firms with major operations in both the US and Mexico. It could build a coalition of commercial enterprises that oppose any renegotiation or repeal of NAFTA on both sides of the border, putting political pressure on Trump to remain in the agreement.

Very interesting and well-researched!

It makes sense that KCS is seeking to limit risk by focusing on domestic markets in both Mexico and the US, especially given their extensive rail connections internal to each country. Would it make sense for the railroad to invest in other logistical infastructure in Mexico, such as ports, in anticipation of factory output increasingly traveling to overseas markets as opposed to the US?

I also wonder if there are financial instruments KCS could use to hedge on the risk of NAFTA being dropped. Some sort of insurance arrangement could potentially offer some risk buffer if the worst were to happen, giving the company additional capital and time to find new market opportunities.

This is a really interesting article. I like your proposal that KCS diversify the revenue of its Mexico business through pursuing domestic Mexican contracts. I think the company should employ the same strategy in the U.S. in order to de-risk the operations of that business as well. That said, KCS should not abandon cross-border traffic altogether. These cross-border contracts are likely with large customers that could represent a material portion of KCS’ revenue. KCS must continue to serve the demands of these customers as long as the regulatory/trade environment allows. And, as a long-term operator along this corridor, KCS is invested in cross-border trade irrespective of the current uncertainty.

To de-risk its Mexico operations, KCS may also consider acquiring another railroad in Mexico. Doing so would bulk up the Mexico operations, perhaps making them viable as a more “standalone” business. Additionally, building on your suggestion that KCS invest in projects where it can share risk, the company may consider partnering with the Mexican government to invest in projects that support domestic businesses. These projects may include shared investment of the upfront capital (reducing the amount of cash KCS has to invest in the project) or a sort of guaranteed revenue stream similar to the Sasol project you mentioned (de-risking the cash flows from the project).

The Mexican government may find such projects attractive as they would promote economic growth within the country, and KCS benefits through growing its Mexico business with domestic customers.

Extremely well written and engaging! I agree that KCS should focus on domestic operations for both Mexico and the US. Although, I am skeptical that Mexico is interested in an only domestic business. As you mentioned, the Mexican government is interested in cross-border logistics because they are helping the economy grow. I believe focusing on lobbying efforts within the US government is the best use of time and money to keep the NAFTA agreement in effect while also investing more heavily in the US domestic market. Building more relationships and contracts within the US will provide stability if the NAFTA agreement is taken off the table.

Another comment mentioned the installation of ports or other infrastructure in Mexico to trade with other countries aside from the US as an alternative. I believe this is too large of a risk to undertake due increasing trend of isolationist policies globally.

This was a very interesting read on a player which I had not considered in the current political discourse. Kansas City Southern is currently in a difficult position if NAFTA were to be nullified. I think the company is doing the right thing by working with industry and political leaders across all three countries. However, in the event that a trade deal is not reached, I think KCS’ current business will be safe (particularly in the near-term), but future growth in inter-country trade will be at risk. The author also brings up a good point that KCS needs to continue to invest capital in the region, but with tight guardrails.