How Big is Amazon’s Opportunity in Healthcare?

In October 2017, reports surfaced stating that Amazon’s entry into healthcare was imminent. Overnight, stock prices for top pharmacies, PBMs, and wholesalers plummeted, losing a sum total of ~$40B in market capitalization [1].

But how well-equipped is Amazon to disrupt the entire healthcare supply chain?

Having worked as a healthcare consultant, and as a member of a family entrenched in the business of healthcare, I can say: this is one of the most critical unknowns facing the industry.

Rumors that Amazon is gearing up for a major entry into healthcare have existed almost as long as Amazon has. In 1999, Amazon acquired a 40% stake in DrugStore.com [2], but shut down the operation a few years later [3]. Recently, Amazon insiders leaked that “for the last few years, Amazon has held at least one annual meeting… to discuss whether it should enter the US pharmacy business” [4]. Outside the US, Amazon recently teamed up with Japanese pharmacy chains Cocokara Fine Inc and Matsumotokiyoshi Holdings to provide home delivery of prescription drugs [5].

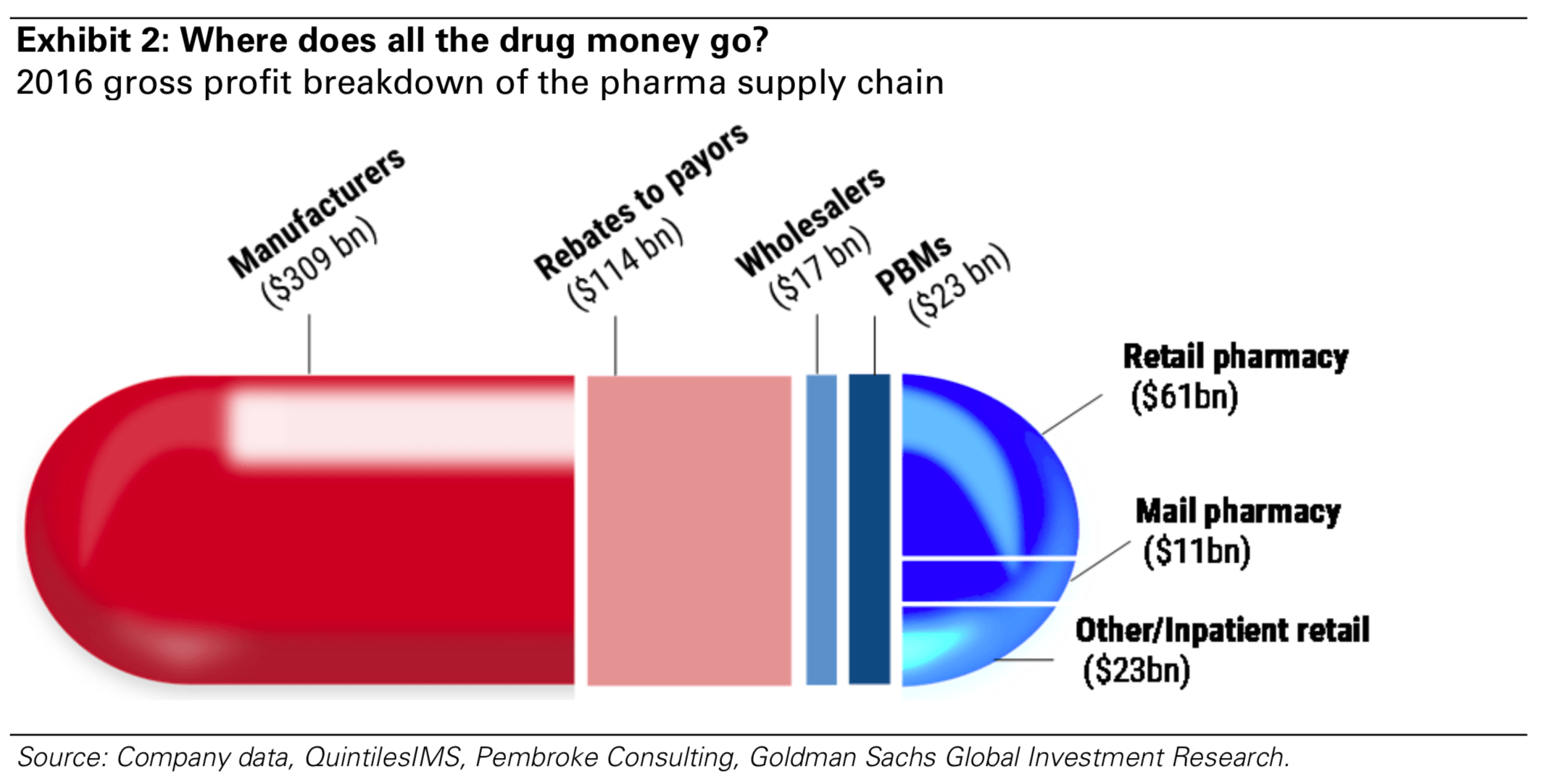

The interest is warranted. Total US gross spending on prescription pharmaceuticals in 2016 was $560B, with $135B captured by the supply chain.

A downstream play seems like low-hanging fruit.

The downstream side – consultation, retail pharmacy and home delivery- seem inevitable, because it so synergistically fits with existing strengths of Amazon’s digitized supply chain. Consider the new Amazon pharmacy world, imagined by Nabeel Ahmad of Huron Consulting:

Personal health data could be combined with shopping patterns to identify an individual as at-risk for an illness. If the condition worsened and the individual needed to see a doctor, an appointment could be scheduled via a virtual personal assistant, during which, the doctor could order a prescription using voice commands, and two hours later the medication could be delivered to the patient’s door. [7]

The connecting thread throughout this hypothetical is transparency. Discussed within the broader vision for digitized supply chains, Stefan Shrauf of PWC writes “transparency enables companies not just to react to disruptions in demand but to anticipate them, modeling the network, and adjusting supply immediately as conditions change.” [8] If Amazon built a system in which some or all of its 80M Amazon Prime subscribers [6] were refilling prescriptions through a singular shopping portal, Amazon would establish unprecedented access to customer behaviors, pre- and post-purchase, upon which to run analytics and develop a proactive, predictive and flexible supply chain from storage center to customer. If the company paired that with telemedicine and brick-and-mortar pharmacy run through its new Whole Foods locations, it could limit the extent of behavioral change required by its consumers.

But it will require substantial change from consumers. In 2016, only 12% of prescriptions were delivered through mail, and that figure is declining [6]. The decline is primarily due to cost matching from brick-and-mortar pharmacies [9]. Without a cost advantage, patients are opting for the comfort of interacting with their pharmacist, over the convenience of home delivery.

According to a 2017 study by Wells Fargo, over 50% of those polled are interested in refilling prescriptions through an Amazon digital pharmacy [10]. But how much of that rests on the promise of lower co-pays? Consider the demographics: 73% of prescriptions are filled by patients 45 and older [11]. Is that contingent more likely to be converted by digitized purchasing interfaces or lower costs? I would argue for the latter.

Which brings me to a final question: can Amazon substantially reduce cost to consumers without playing in the upstream?

Goldman Sachs argues that Amazon can reduce cost-to-consumer by owning formularies and promoting generic alternatives [6]. McKinsey, alternatively, sees the key to cost reduction in whole-scale refinement of the supply chain, squeezing margins for intermediaries and reducing manufacturer’s profits [12]. There are merits to both arguments. But if McKinsey is correct, and the holy grail to cost reduction lies upstream, I believe Amazon has a tough road ahead.

Upstream, digitization is the only advantage and a limited one.

Downstream, scale is an advantage for Amazon. Top players CVS and Walgreens own only 41% of the total market [6]. Wholesale, on the other hand, is both huge and consolidated: the top 3 players capture 88% of distribution [6]. They supply not only pharmaceuticals, but medical supplies and devices, and serve both retail pharmacies and hospitals. This scale allows wholesalers to overcome razor-thin margins – less than 2% on average [7]. For Amazon, scale would be required, but it wouldn’t differentiate.

This leaves digitization as the key differentiation on which to compete. But in the context of upstream pharmaceutical supply chain, there are limitations.

Transparency: HIPAA patient information confidentiality restrictions would limit the ability to see consumption data for individual patients unless the pharmacist was under the Amazon umbrella or the patient gave explicit permission [7].

Warehouse Automation: storage and transport of prescription drugs is highly regulated and scrutinized by the FDA. As a result, experimentation is highly limited and time to market with any change to operation is extremely slow [12].

Additional questions to consider:

- Other than reducing costs, how else could Amazon improve the purchasing experience for hospitals and other retail pharmacies to prompt switching from existing distributors?

- Same question for manufacturers… How could amazon improve the selling experience?

[Total word count: 793]

Sources:

[1] The New York Times, 2017. “Hearing Amazon’s Footsteps, the Health Care Industry Shudders” Link

[2] The Wall Street Journal, 1999. “Amazon Purchases 40% Stake In Web Upstart Drugstore.com” Link

[3] GeekWire, 2011. “Walgreens to shut down drugstore.com, 4 years after $429M acquisition” Link

[4] CNBC, 2017. “Amazon is Hiring People to Break into the Multibillion-Dollar Pharmacy Market” Link

[5] The Japan Times, 2017. “Amazon launches same-day delivery service for food and medicine“ Link

[6] Goldman Sachs, 2017. “If Healthcare is Amazon’s Next Frontier, Partnership May Be What the Dr. Ordered”

[7] Huron Consulting Group, 2017. “How Amazon Could Revolutionize Healthcare”

[8] Price Waterhouse Cooper, 2016. “How Digitization Makes the Supply Chain More Efficient, Agile, and Customer-Focused”

[9] National Community Pharmacists Association (NCPA), 2013. “A Comparison of the Costs of Dispensing Prescriptions through Retail and Mail Order Pharmacies” Link

[10] The Street, 2017. “Why Amazon May Want to Crush Walgreens and CVS By Selling Prescription Drugs” Link

[11] US Department of Health & Human Services – Center for Disease Control and Prevention – National Center for Health Statistics, 2016. “Health, United States 2016. With Chart on Long-term Trends on Health” Link

[12] McKinsey & Company, 2013. “Strengthening health care’s supply chain: A five-step plan”. Link

The question about Amazon’s entrance into the healthcare space is an interesting one, as its entrance will undoubtedly disrupt the industry. To me, Amazon’s core mission to be the place where people can buy anything they need to online. Amazon’s hurdles are both behavioral and legal – you mention the consumer’s current hesitation to purchase prescriptions online (especially difficult given the demographic of the main target market) as well as the entrenched supply chain and government regulation that makes disruption more difficult.

If it goes upstream, such as wholesale, I think Amazon’s is entering a space with large, entrenched players. As such, I think Amazon should play the role it always has, getting customers to buy things online they otherwise wouldn’t. Given it’s recent acquisition of Whole Foods, I think there is a strategic advantage to integrate Amazon’s evolving brick-and-mortar presence with an entrance into the pharmacy retail space. Amazon is currently working to integrate Whole Foods into its Amazon Prime operations, taking their existing customers online. There is a prime opportunity for them to integrate retail pharmacy and make those customers comfortable with shopping online.

I believe it’s only a matter of time before Amazon makes a concerted push into healthcare. Healthcare spending represents ~18% of the US economy and Amazon won’t neglect this and I think it will make an entry into multiple parts of healthcare. Amazon has started selling durable medical equipment online, begun developing internal pharmacy benefit plans and AWS just started a move into healthcare IT in partnership with Cerner [1]. In response to your question, “how well equipped is Amazon to disrupt the entire healthcare supply chain”, I think most downstream pharma and elements of healthcare IT are fair game.

With regards to the pharma supply chain, I certainly agree with your assertion that downstream is the place to be and that cost is an important element. The question I have is whether you’re underestimating (i) the importance of convenience (which can improve prescription compliance, improving outcomes and lowering overall cost of care) and (ii) the role of the provider and their importance in pushing an Amazon-like delivery solution? On the latter question, I think that providers will be able to drive significant changes in consumer behavior, providing Amazon has a product that integrates easily with their system and is convenient for consumers. One startup that has made inroads (and is known to Amazon) is NimbleRX [2], which offers same day, free delivery to patients in the Bay Area and runs a wholesale pharmacy integrated behind the scenes with physician practices. The company just raised $28M of Series B funding [3] . Their competitive advantage is reputedly this smooth provider linkage and relationship; I wonder whether Amazon could scale this kind of provider-focused business model rapidly and lower logistics costs to provide a wholesale pharmacy capable of overcoming the consumer behavior barrier you’re concerned about?

1 – https://www.bizjournals.com/kansascity/news/2017/11/27/cerner-reportedly-will-partner-with-amazon-on.html

2 – https://www.nimblerx.com/

3 – https://www.cnbc.com/2017/10/23/nimble-drug-delivery-startup-scores-28-million-in-funding.html

Thanks very much for the article – really interesting to think about Amazon’s approach to entering the healthcare space, particularly in light of recent noise around a partnership with/ acquisition of Cerner (leading hospital electronic health records provider).

I think you’re right to point out that upstream would be a tough slog given concentration among ABC, MCK, and CAH. But one big question I’m faced with is what would make Amazon better than the incumbents in downstream. A few success criteria that come to mind, and thoughts about the incumbent landscape, are:

– Physical footprint: established players have thousands of retail locations (vs <500 Whole Foods locations), which as you've pointed out are the preferred means of receiving drugs among the general population.

– Time sensitivity: the major use case for mail order pharmacy as I understand it is for recurring/ chronic prescriptions, where the predictability of refills nullifies much of the benefit of same- or next- day delivery. Not to mention, a logical response among incumbents to the prospect of Amazon entry would be to offer matching delivery speed, which CVS has done recently [1]

– Lack of consumer involvement: in my view as a consumer, Amazon excels not just because they offer fast shipping (which is increasingly table stakes for ecommerce) but also because of the simple consumer interface and preponderance of options. Given the limited role of the consumer in selecting prescriptions, will these consumer-facing advantages get Amazon very far in the pharmacy space?

– Biologics/ specialty pharmacy: the real growth in pharma spend $ is in biologic drugs, which are often provided by specialty pharmacies (including those owned by incumbents such as CVS) and entail a suite of coordination and higher-touch capabilities beyond shipping boxes to consumers. Would Amazon leave this part of the market to incumbents to focus on the small-molecule/ largely Gx pharmacy business?

The above list isn't meant to be comprehensive, and I don't doubt that Amazon could make a push into the pharmacy business. They could certainly afford to cross-subsidize the offering and starve the incumbents of their profit streams, which while seemingly anti-competitive hasn't triggered a regulatory response to date in their other business lines. But I'm still not clear on why Amazon will be the winner in downstream pharmacy vs other lines of business they may choose to pursue (EHR seems more promising given the IT-intensive nature of the business and woefully poor offerings on the market). My interpretation of the share price hit that incumbents took upon Amazon's announcement was more a recognition that profit pools will be squeezed and incumbents will have to cut costs and improve service offerings to shore up their defenses against a seemingly profit-agnostic entrant rather than a recognition that the incumbents are destined for the dustbin of healthcare history.

1. http://fortune.com/2017/11/06/cvs-free-same-day-prescription-delivery/

Great piece! As a big fan of Amazon Prime, I’m excited to see how this will play out over the next few years. I really liked your take on which part of the pharmacy value chain Amazon will target, and I’ve included a few thoughts below:

In the short term, I think Amazon will ultimately favor other expansion efforts over pharmacy (e.g. Amazon Fresh, Whole Foods integration, expanded Prime Now delivery). However, in the long-term I think this could be an attractive growth opportunity for an increasingly diversified Amazon Prime offering. As Amazon considers their entry strategy, it seems to me they should lean more toward entering through a strategic partnership with an upstream provider, such as a pharmacy wholesaler or pharmacy benefit manager (PBM). This would allow Amazon to more easily navigate a complicated legal environment and offer its robust distribution network to a mid- to large-size partner. Indeed, analysts at Goldman Sachs have declared that, for Amazon, “partnership may be what the Dr. ordered” [1]. The analysts go on to say, “In such a partnership, AMZN could manage the customer experience while the PBM processes, adjudicates, and fills the claim, still giving AMZN access to patient data and the potential to cross-sell related products” [1]. It seems that Amazon is already testing potential pharmacy partnerships—since November 2016, Amazon has partnered with a drugstore in the greater Seattle area to sell non-prescription drugstore products (including over the counter drugs) to Prime members in the area.

If Amazon chooses to pursue another part of the value chain, it may consider leveraging its expertise in logistics and growing B2B presence to more efficiently serve wholesalers and PBMs. In its first year of operation, Amazon surpassed $1B in B2B sales through its Amazon Business platform [2]. If able to effectively manage the complex legal requirements of distributing and selling pharmaceuticals, Amazon may be able to add value to small and independent drugstore chains by offering higher service levels. Still, this seems like a niche play, and I would tend to agree that Amazon’s greatest sustainable value-add in pharmacy appears to be derived from its consumer-facing operations.

1. Jones, Robert et al. “Alexa, refill my Lipitor.” Goldman Sachs. August 10, 2017. Accessed November 27, 2017.

2. https://www.digitalcommerce360.com/2016/05/04/amazons-billion-dollar-b2b-portal-growing-rapidly/

I completely agree with your prognosis that the downstream market seems as though it will be significantly more attractive to enter for Amazon than the upstream market. In addition to the current concentration among existing wholesalers and low profit margins, the manufacturing process could entail significant legal and regulatory exposure that I do not believe it is within Amazon’s core competency to manage.

On the other hand, I concur with your analysis that there should be an opportunity for Amazon to take share on the consumer side. It doesn’t surprise me that currently most consumers do not utilize direct shipping – existing pharmacists have an incentive to push consumers into the pharmacy where they generate higher margin sales and develop more stickiness through person-to-person pharmacist / customer relationships. I think the ultimate difference with Amazon though is the appeal to a consumer of rolling their medical purchases into their existing Amazon consumption behavior. I do think there is a difference between creating a Walgreens / CVS account just to order one recurring medication from them versus being able to add an order to your Prime checkout basket. Amazon might even have an opportunity to create a system where patients could have doctors place the order directly with Amazon (would be same to medical provider as sending the prescription to the customer’s pharmacy), which makes it even easier for the customer. The growing supply of generic drugs in the US makes this even more attractive, since brick-and-mortar pharmacies will not have the same value-add quality differentiation in the generic market that they might have in more specialized medications.

While Walgreens / CVS could respond to a shift in customer preferences by increasing marketing of their own direct shipping options, I think it is clear that Amazon would have significant advantages in terms of distribution economics. As part of their current business model, pharmacies are paying the working capital cost to hold inventory at local retail locations, but it is not readily clear that their inventory management systems would allow them to seamlessly utilize this inventory for home delivery. For example, whereas Amazon could centralize shipping logistics at their distribution centers, existing pharmacies would have to add some functionality to their existing operations for pharmacies to take brick and mortar inventory and package it for last-mile delivery, which the pharmacy then either has to contract or build out.

While I don’t doubt that Amazon could capture market share in parts of this segment if they so chose, the first question I have is whether or not those revenues would actually be profitable. In a little bit of a catch-22, Amazon would be the most competitive on low-cost, generic drugs, but those are also the products with the lowest merchandising margin and thus might not leave room for significant all-in profitability after accounting for shipping. The second question I had was whether Amazon would open itself to legal or regulatory liabilities even if it only participated in the downstream retail function as you described.

Hey! Thanks for this piece. Very interesting to read about Amazon’s entry into this space. Dozens’s of online pharmacy businesses mushroomed in India in 2015 and promptly faced the wrath of regulators (Indian pharmacies require pharmacists to physically validate the prescription) and had to be shut down or change their business models.

B2C/Downstream:

A behemoth like Amazon entering this space will push regulators to adapt and ultimately lead a multitude of benefits for the customer and the industry at large: (1) increase transparency and affordability of out-of-pocket medicines particularly in a country like the US where drug prices are high and generics are still not the majority of sales. (2) encourage sales of generics as their visibility could be improved (3) reduce the power and role played by the pharmacist (3) increased convenience – eg. an Amazon dash button for medicines

However, I question if this is the best option for Amazon as I believe that it does not allow Amazon to leverage many of its strengths and adds a host of risks. I agree with the point of view in some comments above that Amazon would be better served chasing some other low-hanging fruits.

1) Regulation and legal liability: Drugs are completely different in my view from consumer goods where the impact of a wrong order, expired drugs, drug defects can be much higher and lead to significant legal implications for Amazon. Today Amazon does not take responsibility for the products it sells – will Amazon take responsibility for its drug sellers? Will Amazon enter the business itself? This is not Amazon’s current skill-set.

2) Legal implications of aggregating data, reviews and showing ads: One value proposition of using Amazon is the availability of reviews, ratings and “recommendations” based on past user data. However, prescriptions are very sensitive data. While there is a massive data arbitrage opportunity – for everyone from insurance providers to pharma cos, it is unlikely Amazon will be allowed to do anything beyond being a simple website where drugs can be searched and sold. Unlike CPG, drug purchases are not an individual’s decision and are completely controlled by the doctor. Any attempts by Amazon to influence the patient’s decision can lead to legal liabilities for Amazon.

3) Pricing: Price opacity in the pharma industry is intentional and the transparency that Amazon introduces, while great for customers, could be met with opposition by pharma cos owing to pressure from other channels – esp. for biologics and non-OTC chemical drugs competitive. Additionally, a lot of Amazon’s pricing power comes from its ability to influence the customer via position on site, ads, etc – so in this case, my hypothesis is that Amazon will have scale power but for the above-mentioned reason, no influencing power.

B2B/Upstream:

B2B is a whole different ball-game compared to B2C – owing to the business being focused on negotiations, customization, etc. For similar reasons to the B2C, I think B2B for CPG/Industrial supply chain is the first thing Amazon should focus on, fine tune the model before even considering B2B pharma.