GuiaBolso: How machine-learning is changing competition landscape for Financial Institutions in Brazil

Machine-learning is disrupting how companies manage credit default risks allowing medium banks and fintechs to produce robust prediction models obtaining supreme accuracy and speed. GuiaBolso, one of the main fintechs in Brazil, is leveraging its large customer information database with machine-learning to provide credit at more competitive rates than leading banks in Brazil.

Machine-learning potential in Financial Services Industry in Brazil

Traditional banks have historically served segments of the population they can conduct robust risk assessments on. This leaves a great part of the market unattended. Even so, the accuracy of their assessment is still limited because it’s hard to analyze information in real time2 and banks still rely on big teams to produce sophisticated prediction models.

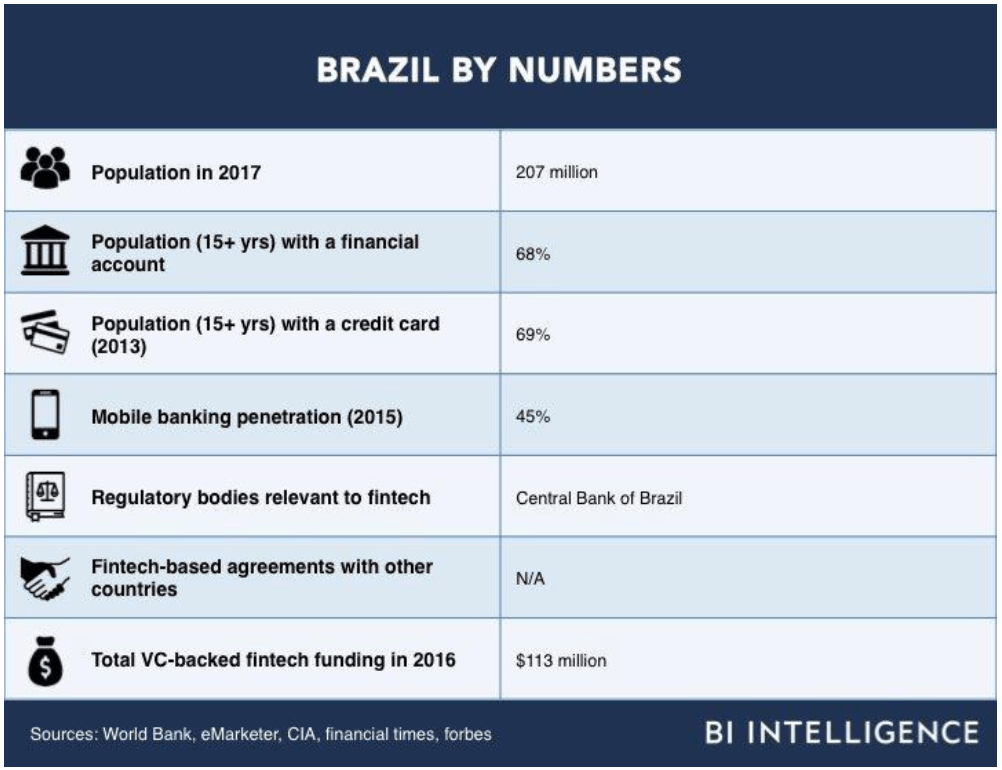

There’s a great opportunity to break into the untapped borrower market, which, even in developed regions, is huge. In Brazil, there’s still a great part of the population who’s not served by financial institutions – 32% of the population doesn’t have a financial account and the mobile-banking penetration is only 45%3 – indicating a significant market potential currently not served by Financial Institutions.

Exhibit 1: Brazil Financial Services Sector by Numbers

New technologies in Machine-learning are changing this landscape – Fintechs are using machine-learning to produce better predictive models that can better assess risk – allowing financial institution to offer credit for unattended parts of population who would otherwise be rejected by traditional institutions or to better assess risk of creditworthy customer and, as a consequence, offer better rates for customers that are currently served by traditional Banks.

Technically, AI help FIs better manage their credit risk by improving the accuracy of their existing risk models, and by finding relationships between financial and personal variables more quickly and effectively than a linear model could. AI can also monitor FIs’ credit models and sends alerts if it believes a model needs recalibrating, as well as recommendations for how to improve a model’s accuracy. A startup named James, who offer this technology to FIs, claims to have reduced default rates for these firms by 30% and boosted acceptance rates for loan applicants by 10%. This capability will become more significant as the economy increasingly digitizes and generates more data points4.

GuiaBolso: How a fintech is leveraging its extensive customer base to compete directly with the biggest Banks in Brazil

Guiabolso started as a mobile personal finance service offering financial management tools – integrating in an intuitive and organized manner information about a customer several bank-accounts, credit-cards, and other financial products. This innovative idea in the Brazilian market, made the app become the most downloaded finance app in Brazil in just a few weeks and now reach over 4.0 million app users5.

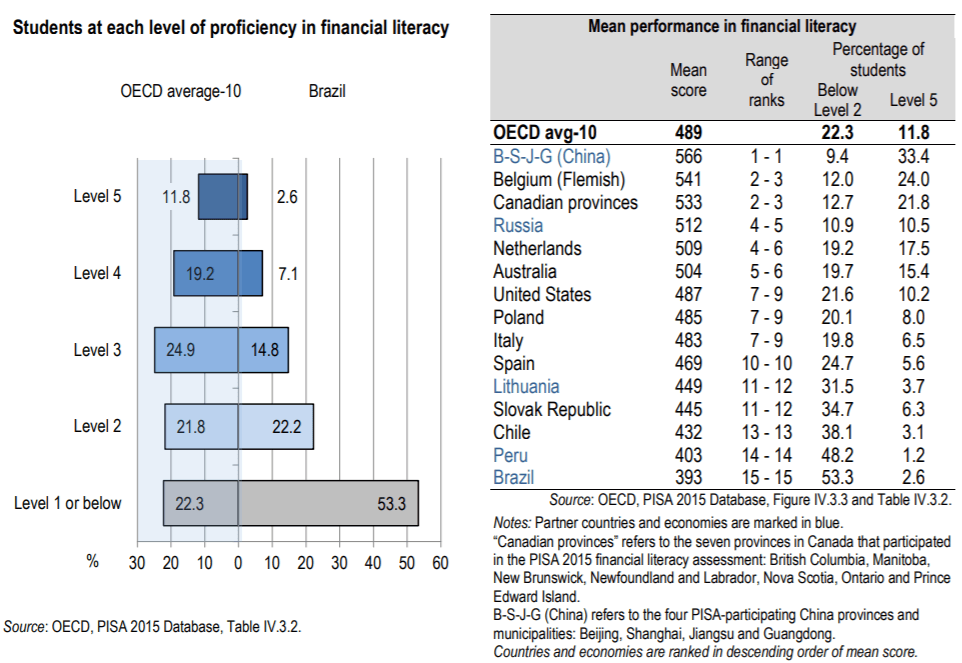

The great demand for the app can be explained by analyzing Brazil’s context, where financial literacy is still a big problem to be solved. Brazil’s performance in this context is well below the average according to a study conducted by OECD6.

Exhibit 2: Financial Literacy assessment by OECD

After reaching a considerable customer-base, the app started offering loans using a platform approach: connecting consumers to financial products offered by traditional institutions. Moreover, by offering free credit bureau reports, GuiaBolso gives users a complete view of their finances and provides bank partners with unparalleled data analysis and credit modeling powered by the combination of extensive data and AI7.

Now, GuiaBolso is attracting funding to offer loans themselves with lower rates than traditional banks. With this move, they will be directly competing with Financial Institutions that are integrated in the platform. According to its executives, the natural path is to transform GuiaBolso in a bank, offering even more financial products tailored to its customers with the support of its extensive data-base8.

Challenges and Next Steps

As a recommendation, to be able to continually offer better products to its customers the company must keep increasing its customer base. To continue helping Population with low financial literacy to understand and manage their finances is the way to do it. Even now that the firm can generate profit from its loans, the company need to keep its focus in its origins, having a great financial management app to continue to grow and be competitive in the long-term.

Besides, to remain attractive, even now that the company is going to offer its own loans to customers, the firm must still need to work as a Platform with other financial institutions. However, this can lead to conflicts:

How can Guiabolso manage the conflict of becoming a Bank, offering its own financial products, but also being a platform that connects customers with other Financial Institutions? Now that the firm will compete directly with the Financial Institutions in its platform, should the firm continue to market its credit-bureau reports to its competitors? (784)

[1] AI and Big Data Technologies Transforming Financial Services – Frost & Sullivan – TechVision Analysis D7BDInformation & Communication Tech. 28 Sep 2017 – https://cds-frost-com.prd1.ezproxy-prod.hbs.edu/p/71319/#!/ppt/b/slide?sid=D7BD-01-01-01-01&id=D7BD-01-00-00-00&hq=Financial%20Literacy%20Brazil

[2] Digital disruption of credit scoring – How developments in the credit scoring space are opening up new opportunities for incumbent lenders –Business Insider Intelligence – August 2017 https://intelligence.businessinsider.com/post/the-alt-credit-scoring-report-how-new-credit-scoring-methodologies-can-help-incumbents-pull-the-rug-out-from-under-alt-lenders-2017-6

[3] Fintech Snapshot: Brazil – Business Insider Intelligence – November 2017 – https://intelligence.businessinsider.com/post/snapshot-brazil-2017-10

[4] Gartner – Cool Vendors in AI for Fintech http://www.gartner.com/document/3872949?ref=solrResearch&refval=211553125&qid=bd7f8225654499cf68991b71fa522b2f

[5] “GuiaBolso raises $39 million to Expand Brazil’s Leading Digital Financial Hub” – Business Wire – October, 2017– https://www.businesswire.com/news/home/20171018006524/en/GuiaBolso-Raises-39-Million-Expand-Brazil%E2%80%99s-Leading

[6] Country Note: Brazil – Results from PISA 2015 Financial Literacy – OECD – https://www.oecd.org/pisa/PISA-2105-Financial-Literacy-Brazil.pdf

[7] CrunchBase: GuiaBolso – November, 2018 – https://www.crunchbase.com/organization/guiabolso

[8] “Guiabolso can conceive R$ 1 billion in credit by 2019, says executive” – BR Reuters – 06/06/2018 https://br.reuters.com/article/internetNews/idBRKCN1J22YS-OBRIN