Blockchain Powered Asset Tokenization Protocols Threaten Goldman Sachs’ Investment Banking Business

Tokenization of assets, including equity and debt, will disrupt investment banking.

Open innovation has a strong foothold in the tech industry. Big tech companies create application programing interfaces, or APIs, to tap into the knowledge base of outside software developers. By doing this, centralized companies are able to access external pools of knowledge that enhance the value of their own proprietary application. One prominent such example is Facebook’s ‘Like’ button API. Facebook made integrating the ‘Like’ free and easy because it let them tap into apps’ users, giving them access to massive data they didn’t have access to before.

This type of open innovation isn’t unique to Facebook – most all tech companies do it. This isn’t, however, the case for all industries. Tech lies on one end of the open innovation spectrum while the financial sector lies on the other. This is especially true for underwriting services provided by large investment banks like Goldman Sachs. Cofounding Decipher Capital – a VC fund investing in blockchain-enabled projects – coupled with being an investment banker at Goldman gives me a unique perspective into how and why blockchain enabled technologies, specifically asset tokenization protocols, will disrupt investment banking.

This inevitable disruption is best understood by looking at the status quo. Today, Goldman tends to underwrite deals exceeding $100mm. Deal size and limited capacity forces it to be selective with the clients it takes on. Administrative, management, labor, and the other costs related to underwriting a deal don’t change based on deal size – they’re more fixed than variable. As such, Goldman is incentivized to chase larger deals to maximize unit economics. This business model has worked till now because raising capital is expensive and time-consuming, incentivizing companies to minimize the frequency while maximizing the size of capital raises.

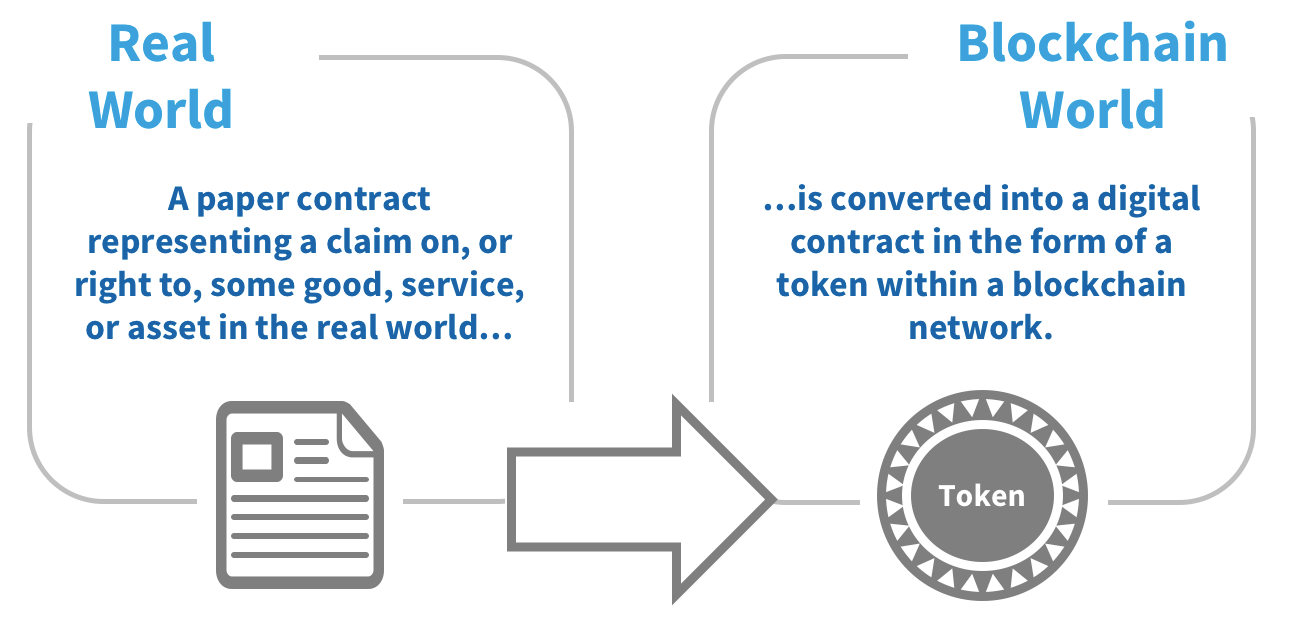

That said, it won’t be like this for much longer. Decentralized, open-source smart contract protocols are enabling the tokenization of real-world assets – including equity and debt.

Goldman hasn’t been sitting on the sidelines. They’ve reacted by actively participating in the blockchain space. Although the press has been focused on Goldman’s short-lived plans to open a bitcoin trading desk [4], its true strategy lies in its investments in blockchain companies. Goldman recently invested in Veem [5], and Tradeshift [6]. Both investments were made through its Principal Strategic Investment Group (PSI). PSI tends to invest in companies that they expect at least one other part of the bank to benefit from a partnership with the portfolio company [7]. These investments increase Goldman’s exposure to blockchain, but the underwriting business is unlikely to be a direct beneficiary of such partnerships. Goldman needs to spend more time integrating blockchain into the day-to-day operations of its underwriting business and not rely on strategic investments by PSI to keep this business competitive.

Final Thoughts and Questions

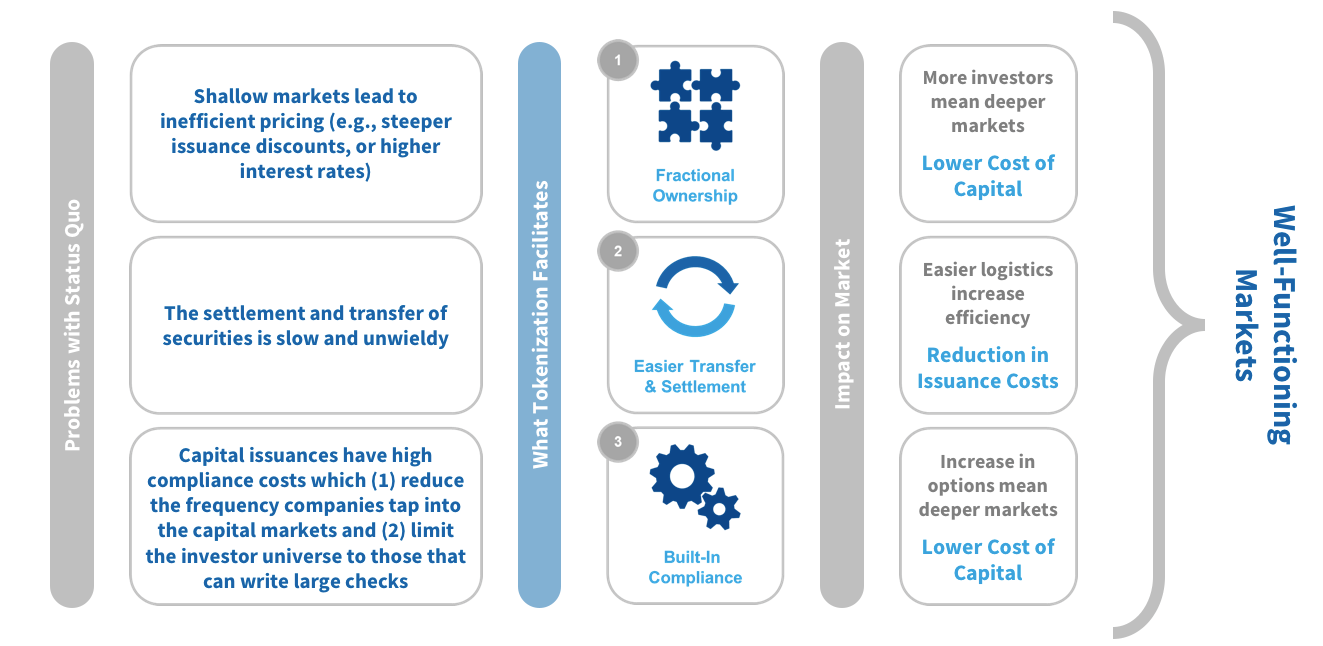

There is no doubt that tokenization has the ability to reduce capital issuance costs. At minimum, Goldman can implement blockchain to reduce the back-end costs of underwriting capital raises. The question remains, however, whether capital raised through tokenized assets will just be a niche alternative to traditional capital markets or whether it’ll be used by large public companies, or the clients served by the Goldman Sachs.

(Word Count: 783)

Citations

[1] Decipher Capital, “Primer on Security Tokens”, August 2018.

[2] Decipher Capital, “Primer on Security Tokens”, August 2018.

[3] statista, “Underwriter fees in U.S. IPO, 2014-2016, by deal size”, January 2017, https://www.statista.com/statistics/533357/underwriter-fees-in-usa-ipo-by-deal-size/, accessed November 2018.

[4] Diptendu Lahiri, “Goldman drops bitcoin trading plans for now: Business Insider”, Reuters, September 5, 2018, https://www.reuters.com/article/us-goldman-sachs-cryptocurrency/goldman-drops-bitcoin-trading-plans-for-now-business-insider-idUSKCN1LL1M0, accessed November 2018.

[5] Veem, “Veem Secures $US 25 Million to Expand Global Payments for Small Businesses”, September 26, 2018, https://www.veem.com/veem-secures-us-25-million-to-expand-global-payments-for-small-businesses/, accessed November 2018.

[6] William Suberg, “Goldman Sachs-Backed Tradeshift Eyes Blockchain After Successful $250 Mln Funding Round”, May 30, 2018, https://cointelegraph.com/news/goldman-sachs-backed-tradeshift-eyes-blockchain-after-successful-250-mln-funding-round, accessed November 2018.

[7] Goldman Sachs, “Investing and Lending Principal Strategic Investments”, https://www.goldmansachs.com/what-we-do/investing-and-lending/principal-strategic-investments/psi.html, accessed November 2018.

As someone who is new to the blockchain world, I find it fascinating that we are considering blockchain as a part of the open innovation process for banks. While the financial sector seems to be more of a “status quo” industry, this article makes a compelling argument that banks should be receptive to these sorts of innovations, or prepare to be disrupted. I do wonder, based on what we’ve seen about the volatility of some of these blockchain/token companies, whether the technology will be “trusted” enough to be accepted and fully integrated into these large financial institutions and their processes.

What I find most exciting about blockchains use in this process has to do with the fractional ownership shown in Figure 2. Arguably blockchain itself provides that open environment which unlocks a separate investor group. From my basic understanding, fractional ownership allows smaller investors to partake in the process which in aggregate could unlock a significant amount of money that normally would not be invested in this way. While I think the author makes a great cost savings argument I wonder if the tokenization of equity actually translates to a normal equity relationship between the company and investor. The article further reinforces my instinct that I need to learn more about the technology.

What I find interesting is not how this can fully replace the capital raising business – there are so many other parts of advisory that go into an IPO or initial debt issuance that I find it unlikely for the service to be fully replaced and for the demand of those services to dissipate – but rather how blockchain technology can be utilized in follow on offerings, back office functions, and capital flows. The advisory services will in my opinion always fetch a premia in terms of fees, albeit unlikely at similar levels as currently. Where it is possible to make the commoditised services cheaper for banks to provide to clients will be interesting to see.

It will also be interesting to see how this will effect the European markets where fees are already only a fraction of US fees, and where it is already close to uneconomical to provide ‘vanilla’ financings. Will banks keep the incremental margin, or be required to pass it over to clients, thus further reducing the incentive to even provide this service from other than a franchise perspective?

This is a great article. Nice job! Having blockchain and tokenization to lower the barrier to entry in terms of cost and access for capital would be great for society. It would reduce the friction between investors and entrepreneurs and potentially could create more access to further disruptive technologies. However, there is one friction that bankers do provide value for and that would need to be addressed as this change takes place, which is in terms of educating the investor. Bankers on their road shows don’t just open the doors and make investors aware of the need for capital. Bankers also create information in the form of presentations, phone calls, and face to face meetings to educate the investor. I would be curious how, as this technology spreads, entrepreneurs can quicker and just as effectively educate the investor to convince the investor to provide capital. I would assume they can make videos and publish their investor decks but I would be interested to see if that is equally as effective as someone coming into your office.

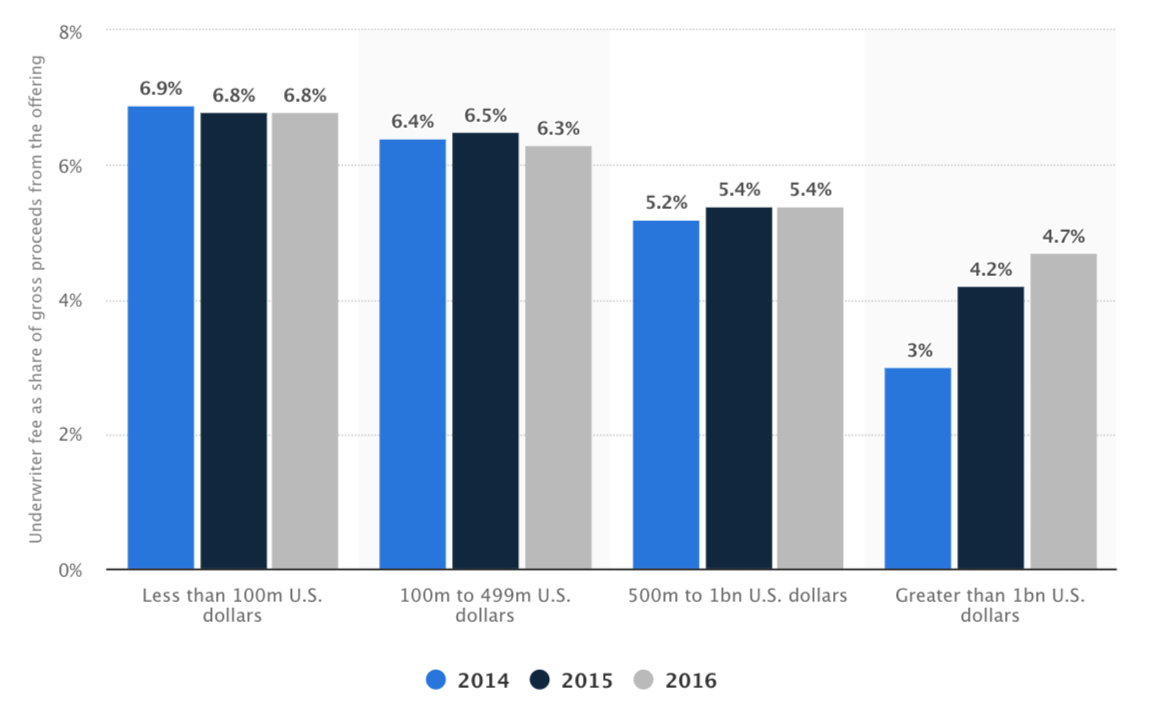

Very insightful article on a tangible use for blockchain technology. There is no doubt that capital raising as it stands today is an inefficient and expensive endeavor. As cited, paying a gross spread of 5-7% on initial public offerings, on top of the initial offering discounts of 15-20%, means companies ultimately see as little as 75% of the money they might otherwise be able to raise for various projects. While I agree that some of these fees are earned since the bankers provide a service by educating investors, to M’s point, I think the bigger issue is the inaccessibility of the capital markets by most firms. Investment banks and most investors do not put their capital behind companies who are not able to meet the strict reporting and asset requirements laid out by various regulatory agencies – I think blockchain could help us better assess risk and remove some of the prohibitive red tape surrounding the process of raising capital to give more companies a chance to participate and more investors the chance to earn a return on their capital.

I agree that Tokenization can reduce capital issuance costs. However, it is really hard to liquify long term physical assets which makes up most of traditional large institutes’ current holdings. Goldman’s investment in the space does lend credibility to long term viability of tokenization, which can ignite an initial round of public interest, and commitment to the space.