Li & Fung – The Downfall of a Platform

On March 6th of this year, the supply chain management giant Li & Fung will be unceremoniously removed from the Hang Seng Index, a globally recognized index of Blue Chip Hong Kong Companies, to be replaced by Greely Automobile. It will mark the another step in the steep decline of a company which was once synonymous with outsourcing and cheap Asian manufacturing.

Li & Fung- The Downfall of a ‘Perfect Platform’

On March 6th of this year, the supply chain management giant Li & Fung (L&F) will be unceremoniously removed from the Hang Seng Index, a globally recognized index of Blue Chip Hong Kong Companies, to be replaced by Greely Automobile.[i] It will mark the another step in the steep decline of a company which was once synonymous with outsourcing and cheap Asian manufacturing in the US.

The Platform

Li and Fung had perfected a platform of outsourced manufacturing, connecting large western retailers to a vast network of factories throughout China and southeast Asia. Going a step beyond simply placing orders on the retailer’s behalf, L&F provided unmatchable speeds by breaking orders up and placing individual specifications to numerous disparate factories based on available capacity. This system had the mutual benefit of providing the factory owners with ever increasing utilization to spread their fixed costs over, while providing their retail customers reliable access to cheap manufacturing. [ii]

History

Li and Fung traces its history back to the turn of the 20th century as a brokerage firm provide translation services for traders operating between the United States and China. After one of the founders’ grandsons, Victor Fung, left his job as an HBS professor in 1976, he returned to Hong Kong and along with his brother turned the company into an indispensable piece of the globalization of manufacturing. [iii]

They began this by connecting western firms to their growing network of factories throughout China. In the earlier years, this was as simple as connecting single companies to single factories for orders, however as L&F became more sophisticated they began cementing their role as a platform instead of intermediary by breaking up customer orders. With a deep knowledge of their network of factories, L&F quickly learned they could expedite customer orders by slicing it into smaller groups and sourcing them individually to factories which had available capacity.[iv]

This ingenuous system revolutionized retail outsourcing in the 1990s. L&F could guarantee deliveries of massive orders in weeks, where previously it would have taken months. Likewise, factories throughout L&Fs network began to recognize huge increases in profitability through the uptick in utilization. Importantly further, L&F’s system broke up each order into a unique supply chain for that specific experience that was cobbled together for this one order, nearly erasing the ability for a customer to go direct to their suppliers and cut out the intermediary.

L&F took a vested interest in ensuring that their network of suppliers was reliable and capable of handling the orders they received. L&F therefore inspected individual factories and provided a tacit seal of approval by incorporating them into their supplier network. This seal of approval became so valued by factory owners during the 1990’s that many accepted extremely coercive terms to join. As the suppliers network grew, so too did L&F’s relative market position to dictate terms to retailers.

Troubles

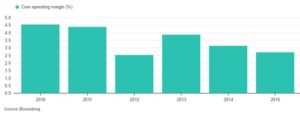

By 2010, the company began to face troubles. Raising costs in Chinese manufacturing, L&F’s primary region of suppliers, forced the company to chase cheap manufacturing trends to Vietnam, Indonesia and Bangladesh. With less expertise in these regions, L&F struggled to replicate their successes of the 1990s and profits soon began to drop.[v]

Even more concerning, in a string of accidents between 2010 and 2014, a number of factory workers were killed in fire and collapses in what many including the New York Times described as ‘sweat shop’ style conditions. Supplier vetting had once been a hallmark of L&F, reassuring customers that their products were being produced by a reliable and quality manufacturer. The push for geographic expansion in the 2000s appeared to have reduced L&F’s ability to inspect and monitor their network, removing a major source of value creation their platform provided. Responding to investor and customer pressures in the West, a number of retailers began curtailing their orders through L&F in the aftermath of these incidents.[vi]

By 2017, L&F has been reduced to a shell of its former self. It appears that the reduction in information asymmetry between retailers and suppliers has allowed a number of customers to remove themselves from the L&F platform and still recognize cost savings through cheaper offshore manufacturing. The rise of Alibaba in China, and to a lesser extend Amazon, has provided L&F’s network of manufacturers with alternative options to fill capacity gabs, greatly reducing L&F’s bargaining power. While the future is still unknown for the survival of the company, their recent removal from the Hang Seng Index symbolically represents the end of their golden age a perfect supply chain platform. [vii]

[i] https://www.wsj.com/articles/DN-CO-20170212-001715

[ii] https://hbr.org/1998/09/fast-global-and-entrepreneurial-supply-chain-management-hong-kong-style

[iii] https://hbr.org/1998/09/fast-global-and-entrepreneurial-supply-chain-management-hong-kong-style

[iv] https://www.wsj.com/articles/retail-sherpa-li-fung-grapples-with-client-loss-1432243801?mg=id-wsj

[v] https://www.wsj.com/articles/retail-sherpa-li-fung-grapples-with-client-loss-1432243801?mg=id-wsj

[vi] http://www.nytimes.com/2013/08/08/world/linking-factories-to-the-malls-middleman-pushes-low-costs.html

[vii] https://www.bloomberg.com/gadfly/articles/2017-01-24/li-fung-may-find-an-unlikely-ally-in-trump-china-tariffs

Really interesting post, thanks for writing. Given that one would assume the business had really strong indirect network effects, it’s amazing how poorly it all seems to have come unraveled. I think that my take-away here is that it’s a lesson in what happens when you suddenly fail to create value for constituents on one or both sides of the platform. The high profile incidents and perception issues on the demand side, combined with competing options on the supply side. I wonder a bit how they could have avoided the decline: the demand side issues seem surmountable, and surely solid demand could have continued to generate value on the supply side, moreso than demand from small businesses on Alibaba. Or maybe not – maybe their only choice was to go head-to-head with Alibaba?

Interesting story Jack. Thanks!

In the BAV course I also read about the firm started posting negative growth for the first time in 2013. The case centered on its three-year strategic planning process and downstream acquisition strategy. It appears that they had also been overpaying for many acquisitions over the years. In any case, I think the root problem is that the global progress in IT had made the value of their platform way less distinctive than before.

The platform perspective is a valuable lens to analyze this company especially since we just did a case on this company in a strategy class and the analysis was significantly different. I wonder if the answer for them would’ve been to keep expanding their supply chain expertise globally ahead of the rise of costs in China etc or if their downfall was inevitable.

Thanks for the post! Last week I learned about L&F in two other classes, Strategic IQ and Business Analysis and Valuation, as well. Your story definitely provided another piece to form a more complete story about this company. I believe the biggest challenge L&F faced – the reduction in information asymmetry – is essentially the challenge for a lot traditional 2C businesses when new online players join the competition. L&F actually tried to vertically integrate the value chain, such as providing logistic services, and acquiring manufactures with brand names that end consumers would recognize. Yet it seems that their efforts didn’t pay out. I guess this also posts a question for other traditional/offline businesses that what is the way out to survive and transform in today’s digital world.

Nice post Jack. It seems that this was more of an execution issue than a strategy one on the supplier side since as you mentioned L&F was providing substantial value add to the factories. I imagine the level of inefficiencies in factories of Bangladesh and Vietnam was much more than they anticipated and hence were unable to improve the operations – the uncertain and unknown economic environments added to the complexity.

In the long run however I do think the platform has enough merits – for both sides to stay on – due to the vertical integration on client side services, sheer size of the supply chain, supplier network and years of experience