Lazada – Alibaba’s point of entrance into South East Asian eCommerce

South East Asian equivalent to Alibaba and its role in building Chinese eCommerce, Lazada has pioneered online shopping in the region by building its eCommerce platform and becoming the online destination site for consumers and one-stop gateway to the region for local and international brands.

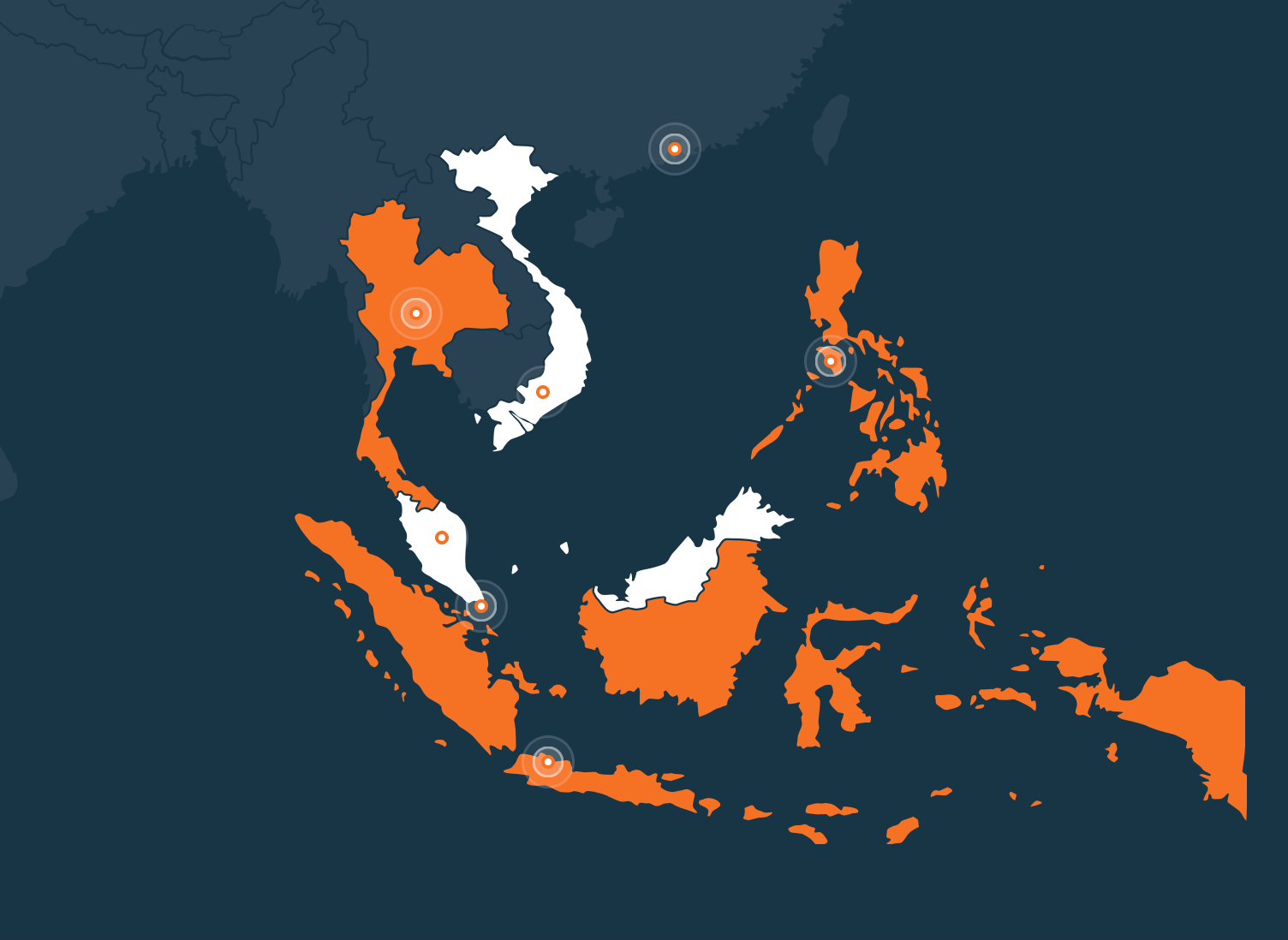

Lazada launched in 2012 and ever since became Southeast Asia’s number one online shopping and selling destination, operating in 6 countries across SEA. Pioneering eCommerce in the region, Lazada offers customers an effortless shopping experience across mobile and web platforms, multiple payment methods and extensive customer care. In the meantime, retailers have simple and direct access to over 550 million consumers in six countries through one retail channel. Lazada features an extensive product offering in categories ranging from consumer electronics to household goods and fashion.

Lazada saw an opportunity in SE Asia’s massive, underpenetrated market:

- Compelling macro secular trends – including GDP growth projections above 8.0% and more than 550m potential customers.

- Nascent market opportunity – characterized by low and rapidly growing smartphone penetration and tinny share of eCommerce as % of retail.

- Outsized growth in SE Asia eCommerce market.

- Increasing income levels that drive further growth.

Despite the massive potential, SE Asia’s structural challenges represented significant barriers to entry:

- Payments – low credit card penetration, preference for local payment solutions and cash on delivery method.

- Logistics – underdeveloped infrastructure, scattered logistics networks, geographic diversity.

- Supply Chain – fragmented local merchant network, inexperienced local merchants, inefficient supply chain.

- Regulatory – challenging import / customs environment across markets.

- Culture & Talent – user behavior vary across and within 6 markets, limited and inexperienced local talent pool, language differences.

Lazada addressed these challenges to become the only eCommerce platform operating across 6 distinct markets in South East Asia and as such created a hard-to-replicate platform.

- Gateway to SEA via a single touchpoint:

- The only eCommerce platform with pan-SEA reach

- Leading brand name: #1 across all launch markets

- Local operations, fulfillment and distribution

- Optimized marketing platform

- Immediate access to 550m potential customers

- Comprehensive marketing strategy across social, mobile and TV

- Best-in-class logistics & supply chain network

- Own warehouses, last mile hubs and largest network of partnerships with local and regional 3PLs

- Customs expertise that enables Lazada to serve all countries seamlessly

- Broad spectrum of supply chain solutions: inventory, cross-docking, drop-shipping, consignment, FBL (Fulfilment by Lazada)

- Secure & trusted payments platform

- Pioneer of COD (Cash on Delivery) with close to 100% coverage in all countries

- Localized payments methods catering to each market

Lazada is building an ecosystem that generates network effects as the platform continues to scale. Broader product assortment brings more customers, attracting more merchants and in turn creates a virtuous cycle driving free traffic, improved curation and higher price leverage.

Seeing the potential of Lazada’s platform, Alibaba recently acquired a controlling stake in the company and is expanding to South East Asia through integration with Lazada.

Nice post Katarina, thank you! Lazada seems like an interesting success story for Rocket Internet. Two questions come to mind… Do you think Lazada could reach its potential in SEA without Alibaba acquiring them? How does Alibaba intend to handle Lazada: integrate or leave autonomous? It seems like SEA is a uniquely challenging market for the five reasons you mentioned, and I wonder how much the acquisition will better address these challenges and benefit consumers.

Thanks for your questions, Erik.

To your first question – from what I’ve seen, the path to profitability in these markets is very long and companies burn a lot of money in building up not only their name and educating the local consumer about the advantages of e-commerce, but also in building infrastructure (ie logistics networks) which are often underdeveloped or not present at all. Given these enormous costs, many players have gone out of business because of lack of funding and believe of some investors about the first-mover disadvantages (given the need to invest in education / infrastructure that benefit all players in the market). I therefore think only a company with big pockets can succeed and that Lazada without backup of Alibaba or another player (ie Amazon) would not be able to survive on its own.

To your second question, Alibaba is currently leaving Lazada as a stand-along entity, but has began to integrate certain aspects of the back-end, marketing, etc to leverage its deep knowledge and economies of scale. I believe integration will proceed in the future but Lazada will remain operating under its own name and rules of local markets (which as we saw in eBay / Alibaba battle are very important to grasp).