Schindler – A Captive Audience?

Company Overview

Schindler was founded in Switzerland in 1874 and is a leading global provider of elevators and escalators. It operates in more than 100 countries and has 54 000 employees.

Business Model

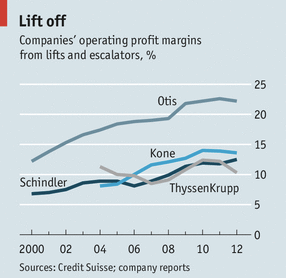

Schindler’s business model is split into New Installations (NI) and Existing Installations (EI). The focus of NI is growth in new markets with rapid industrialization. However, the margins in NI are slim. In contrast, EI has extremely high margins, driven by service and maintenance revenues. As a result, once new units have been installed, the aim is to convert these into long-term (often up to 10 years) and lucrative service and maintenance contracts.

The key advantage of this model is that once the service and maintenance portfolio has reached a ‘critical’ mass, Schindler is relatively protected from economic downturns given that its overheads will be largely covered by the margins of the service and maintenance portfolio. It does not need to rely on revenue from new projects, which are far more sensitive to macro economic and urbanization vicissitudes.

One of the main risks, however, is the erosion of the portfolio to third party service providers, which proliferate particularly in developing markets.

Operating Model

Schindler has created an operating model, which effectively aligns with the dual goals of its business model: to grow NI sales and to protect its EI portfolio. The operating model does this in four main ways:

- Targeted and patented innovation

Much of Schindler’s R&D is geared towards ensuring that third parties are both technically unable and legally prevented from maintaining Schindler’s units. As a result, if a customer buys a Schindler unit, they are obliged to sign a service and maintenance contract too. For example, Schindler has in recent years developed patented components.

These include traction media, a belt component, which replaced the traditional ropes in the shaft. In addition to being a new technology which competitors were unable to service, this technology significantly increased the margins of service. The belt would not rust like the ropes and therefore would not require frequent, costly trips from the service providers. This demonstrates a technology that protected the revenue from Schindler’s EI portfolio.

Another example of a Schindler-pioneered technology, which revolutionized the industry was its destination control system. This system requires building users to swipe an access card, which will direct them to an elevator where other users going to the same floors have also been grouped. This reduces the journey time for all users as the lift does not have to stop on multiple floors. This in turn improves the flow of people through the building as fewer queues of people build up waiting for the elevator. This was a patented technology, which meant that third parties could not maintain it.

In addition, this technology demonstrates Schindler’s focus on software rather than hardware, which has allowed it to grow its NI operations. Schindler’s R&D focuses on controlling the flow of people through increasingly complex buildings. The global urban environment is rapidly changing. Buildings such as ICC (Hong Kong’s tallest building) are used by 15 000 people – virtually a vertical city. Therefore, this form of software innovation from elevator companies is essential. This technology has allowed Schindler to grow its NI sales as it has been a clear differentiator from its competitors. In particular, this product helped Schindler gain traction with high-end residential and commercial developers who required sophisticated elevator technology to match their premium projects.

- Incentives and Productivity

Schindler’s workforce is focused on growing service and maintenance revenue, and incentivized accordingly. Sales teams are given monthly targets for conversion from NI to EI, renewals of contracts and recovery of units that have been lost to competitors. Their bonuses are based on meeting these targets and as a result they are monetarily incentivized to enlarge the portfolio. In order to meet these targets they are supported by trainings geared towards these areas, with a particular focus on customer service and how to drive customer satisfaction.

The service and maintenance engineers themselves are also trained intensively in order to increase their productivity and the quality of their work. Although these teams are on call 24 hours a day, 7 days a week, if productivity and quality can be improved, they can reduce the number of costly trips they need to make to service units and therefore improve their margins.

- Vertical integration

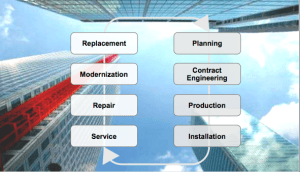

Schindler’s business model is based on it servicing the entire elevator and escalator life cycle (Planning – Contract Engineering – Production – Installation – Service – Repair – Modernization – Replacement). Schindler is entirely vertically integrated, owning all parts of the supply chain. Schindler have maximized their supply chain efficiency, in particular, by outsourcing its manufacturing to two factories in Asia, which provide for the entire global business.

By vertically integrating the supply chain, Schindler eliminates any dependence on buying off-the-shelf systems or components. For NI, this cements Schindler’s ability to differentiate its product line. For EI, it makes it more difficult for third parties to service Schindler products and also reduces the risk of competitors stealing new technologies.

- Product line – commoditization vs. customization

Schindler has 3 product lines, catering for low, mid and high rise buildings respectively. The mix of these products allows Schindler to maximize its profitability as it strikes a balance between commoditization and customization.

The low-rise product is a standardized product with little customization. The margins are relatively slim but it allows Schindler to penetrate emerging markets, which have fewer high rise buildings and gain an early footprint, capturing market share. The low-rise product therefore drives NI revenue.

The mid and high-rise products are much more highly customizable. Whilst this high level of customization often means these products are higher cost and therefore lower margin, it allows Schindler to cater for a wide variety of customers, from hospitals to stadiums to public transport. These projects are often highly visible and therefore, whilst often not boosting profitability, they are essential for brand building. In addition, given the greater complexity of these projects, customers are even more likely to sign EI contracts. The mid and high-rise products therefore drive EI profitability.

By leveraging these four elements of its operating model, Schindler is able to grow its new sales as well as maximize its lucrative EI margins, which in turn drive the long-term profitability of the company.

Sources

http://www.economist.com/news/business/21573568-things-are-looking-up-liftmakers-top-floor-please

http://www.schindler.com/com/internet/en/home.html

What an awesome business! Sounds like a cash cow once it has a sizeable established footprint in a market. Who would have known that elevators are essentially sold under the same business model as printers/print cartridges? This is a really cool example of a business that maintains a competitive advantage by vertically integrated production and developing/employing proprietary systems that cannot be serviced by 3rd parties. Do you think the risks of entering markets with weak IP protection are serious potential threats to Schindler’s maintenance focused business model, or do you think the elevator market is too niche to attract serious reverse engineering efforts?

Elevators are a great business! If my memory serves me well – elevator “OEM”s essentially make most of their profit on the service and maintenance part of the business as evidenced by the increasing amount of outsourcing penetration in the industry, which is still far below automotive manufacturers, for example. However, as you point out, I do worry about the proliferation of 3rd party service providers particularly in countries with weak IP protection (China for example), and the margin pressure that results. I would imagine that in those cases the only protection would be regulation – in other words, legislation that requires OEMs to service the elevators due to safety requirements. Do you know if 1) this is a trend being observed in emerging markets and 2) how enforceable these regulations might be?