Metal Additive Manufacturing at General Electric (GE) as future Competitive Advantage across Business Units

GE stomped its way into the metal additive manufacturing space through major acquisitions. Why did they do this and what are they trying to accomplish?

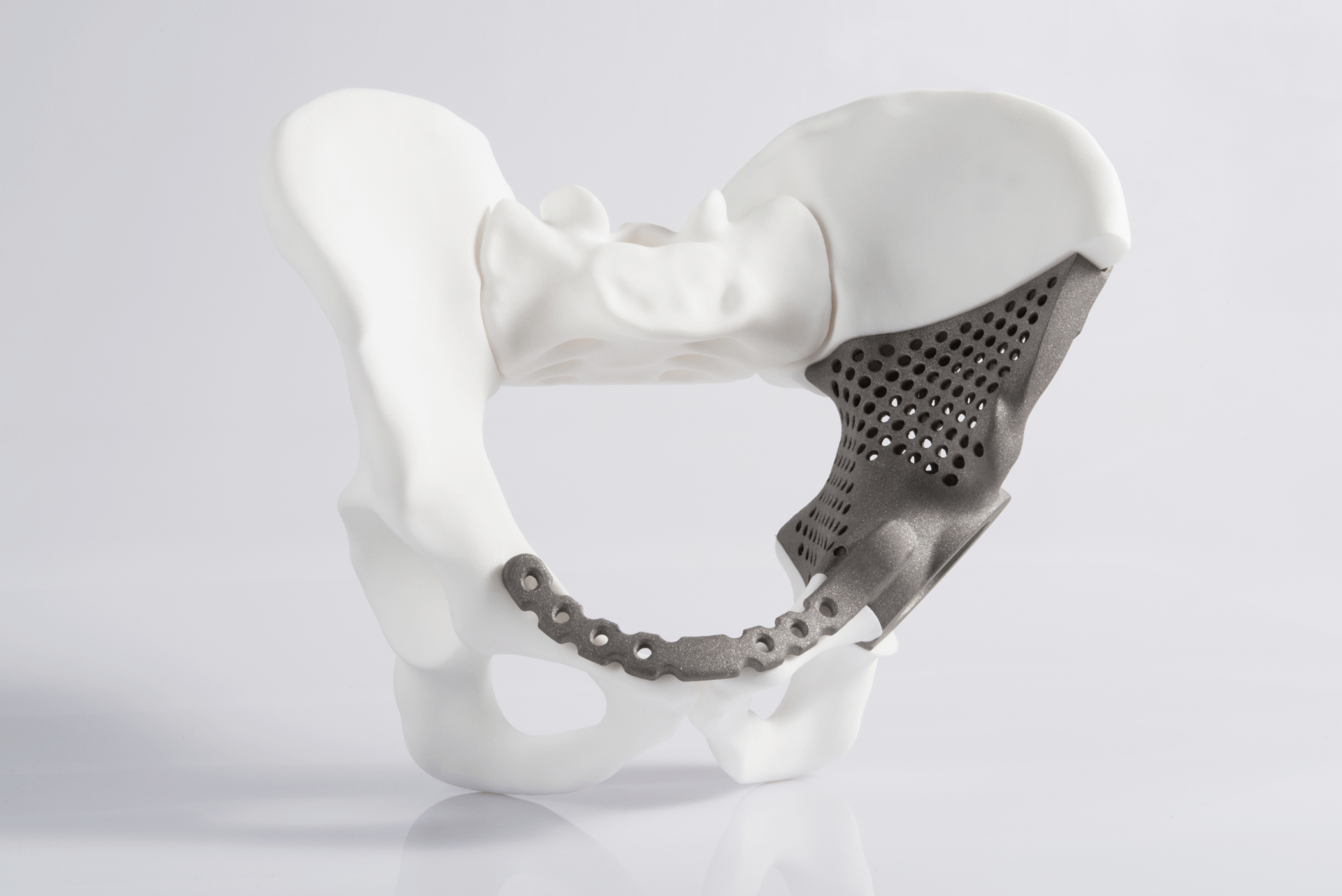

The issue of metal additive manufacturing – often referred to as 3D printing – is and should be at the core of GE’s strategy as the technology could radically change today’s production designs and manufacturing processes. While initial applications often focused on consumer application, as the technology matures additive manufacturing offers extreme opportunities also to industrial manufacturing. The main advantage of additive manufacturing versus conventional milling as a production process is the ability to create completely new part designs that outperform their predecessors in both stability and weight. While this advantage will make additive manufacturing relevant across a wide array of industries at some point, today’s applications are mainly focused on lower batch size processes. Medical applications like implants (Exhibit 1) – often unique in design, i.e. batch size of 1 – are on the forefront of this. With typical batch sizes of ~100-1000, even the aircraft industry has already adopted additive manufacturing for certain parts (Exhibit 2), driving life-time-value benefits that outweigh higher production costs. [1] Of course, the industrial use of additive manufacturing does not stop there. At the point in time where this new technology becomes sophisticated enough to provide cost benefits even for very large batch sizes, even behemoths like the automotive industry will be disrupted.

Considering all the above, missing the right time to build up internal resources on such a technological leap could end up fatal for a conglomerate like GE that relies on providing better and cheaper solutions to their customers.

_____

To address the issue of gathering additive manufacturing capabilities in the short- and medium-term GE is committing significant resources to i) develop capabilities in-house and ii) acquire capabilities from third-parties, namely through M&A activities.

M&A activities:

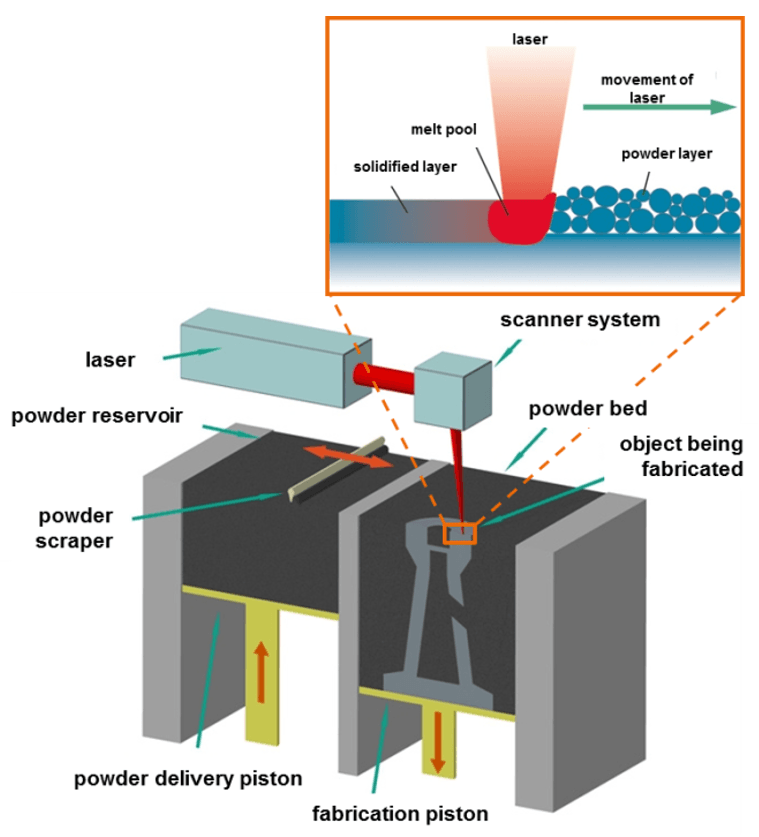

In 2016 GE bid for the Germany-based market leader SLM Solutions, but due to activist investor Elliott Advisors rejecting the bid, GE abandoned the acquisition. Only a few weeks later they then were able to acquire 75% of SLM’s competitor Concept Laser with a $599m bid [2], outbidding multiple private equity funds and other “strategics”. Concept Laser is a pioneer in the metal additive manufacturing space, promoting one of the two major metal additive manufacturing technologies – powder bed laser AM systems (Exhibit 3) [3]. Having purchased one of the leading powder bed technology firms GE went on to acquire a controlling stake of ~74% in Arcam [4], a key competitor who had invented the other major metal additive manufacturing technology – electron beam melting (Exhibit 4) [3]. The combined acquisitions in can almost be interpreted as a technology hedge for GE to stay relevant in metal additive manufacturing no matter which of the technologies will succeed eventually.

In-house efforts:

To address the importance of additive manufacturing GE established a new business unit “GE Additive” in 2016. Today, the business comprises Concept Laser, Arcam and AP&C, an additive materials provider. Besides managing the named sub-businesses, the Additive business units coordinates efforts with GE Digital, GE Power and GE Capital to provide the best possible solutions to customers. [5] Considering that all GE additive manufacturing machines stem from acquisitions the overall internal efforts appear to be insufficient, which explains the rationale behind the purchases.

_____

In the next two to five years GE’s management should try to integrate both the Concept Laser and Arcam businesses into one entity to build a central additive manufacturing knowledge center. This knowledge center should continue to serve external clients, but increasingly work with GE’s other business units such as GE Aviation and GE Healthcare to enable sustainable competitive advantages for those businesses. While external customers are extremely important for the young GE Additive business to drive innovation, over the medium term a critical measure of success will be how effective the Additive unit can be for the success of the overall business, rather than “only” being a 3rd party technology for the wider industry.

_____

Given the current situation of GE (share price down ~55% year-to-date) should the company continue to invest into technology like additive manufacturing that will only show its full potential in a couple of years or rather focus on the current cash cows of the conglomerate?

Looking back should the CEO have tried to develop metal additive manufacturing capabilities in a meaningful way internally rather than investing in acquisitions to receive those capabilities (considering speed, cost, complexity of the acquisitions)?

_____

(727 words)

Exhibits:

Exhibit 1. Additively manufactured medical implants

Exhibit 2. Additively manufactured aircraft parts

{kind=link}

Exhibit 3. Powder bed laser additive manufacturing technology

Exhibit 4. Electron beam additive manufacturing technology

Sources:

[1] Choon Wee Joel Lim, Kim Quy Le, Qingyang Lu and Chee How Wong, “An Overview of 3-D Printing in Manufacturing, Aerospace, and Automotive Industries”, IEEE Potentials, 35(4), 18-22. doi: 10.1109/MPOT.2016.2540098

[2] Reuters, “GE buys Germany’s Concept Laser after SLM bid fails“, https://www.reuters.com/article/us-lng-global-supply-analysis/in-race-to-fill-lng-supply-gap-project-goalposts-have-changed-idUSKCN1NH0LA, October 27, 2016, accessed November 2018.

[3] Benedict, “GE moves forward with takeover of 3D printing companies Arcam AB, Concept Laser”, http://www.3ders.org/articles/20161214-ge-moves-forward-with-takeover-of-3d-printing-companies-arcam-ab-concept-laser.html, December 14, 2016, accessed November 2018.

[4] GE Press Release, “GE Agrees to Purchase Controlling Shares of Arcam AB”, https://www.ge.com/additive/press-releases/ge-agrees-purchase-controlling-shares-arcam-ab, November 15, 2016, accessed November 2018.

[5] https://www.ge.com/additive/ge-technology

Great article! Wunderbar! I think this article precisely hits on the difficulties of looking forward to disruptive forces that may dramatically impact a company’s steady cash flow-driven business. In the case of GE, there are many issues facing the company that would lead one to believe that there should be a focus on cash flow, yet the CEO has pushed through with multiple acquisitions. What I would be curious to understand is whether any of those recently acquired additive manufacturing business lines are on the selling/chopping block given the recent CEO shift.

I can’t imagine that one should ignore the impending disruption of additive manufacturing, even blue chip giants such as General Electric. Given the company’s vast resources, ignoring the inevitable wave would be like playing the ‘oudler’ in French Tarot, even though you have the ’21 of trump’ handy. By the time you eventually do decide to play your best cards, you may be too far behind to catch up to the competition.

Very cool! Are there capabilities in which additive manufacturing can solve for ‘big’ parts? This seems great at a small scale. But I wonder if GE indeed has identified enough use cases for this. Some of those may include ‘bigger’ parts. In general, I agree with GE’s strategy in investing in the technology of the future, and figuring out the concrete applications later, perhaps.

Very interesting! I think your analysis highlights a broader problem across different industries: how should companies develop the skills to capture the value that new technologies offer? And to your question, I don’t see how in-house efforts will allow GE to accomplish this goal.

Large organizations, as GE, are bureaucratic, slow, and resilient to change. These characteristics are opposite to those that characterize the revolutionary trend of 3D printing. For that reason, I believe that M&A is the best way to take advantage of these new technologies.

Given the nature of GE’s businesses–high-design, low-tolerance products that are produced along the same specs for all units sold of a certain model (i.e. that do not require or benefit from mass customization)–I’m not sure additive manufacturing is the kind of obvious game-changer that requires getting ahead of. Though the acquisitions may be fruitful for the IP they involve, a “wait-and-see” strategy may be the better move, particularly while the company has more immediate-term stresses to handle.