It Takes More Than Coins to Change Consumer Behavior

Coin fails in its attempt to change consumer payment behavior

Mobile and technology have changed almost every aspect in our daily lives. Consumers are getting smarter: from online shopping to calling taxis on mobile. Companies are also getting smarter: collecting and analyzing data to customize the consumer experience.

But will payment adopt this trend as well?

Just like Evernote surrendered to pen and paper, mobile payment companies are struggling to compete with simply swiping a credit card. Despite the numerous mobile payment companies from Apple Pay, Samsung Pay to Walmart Pay, less than 20% of U.S. smartphone users have tried out mobile payment at least once.1

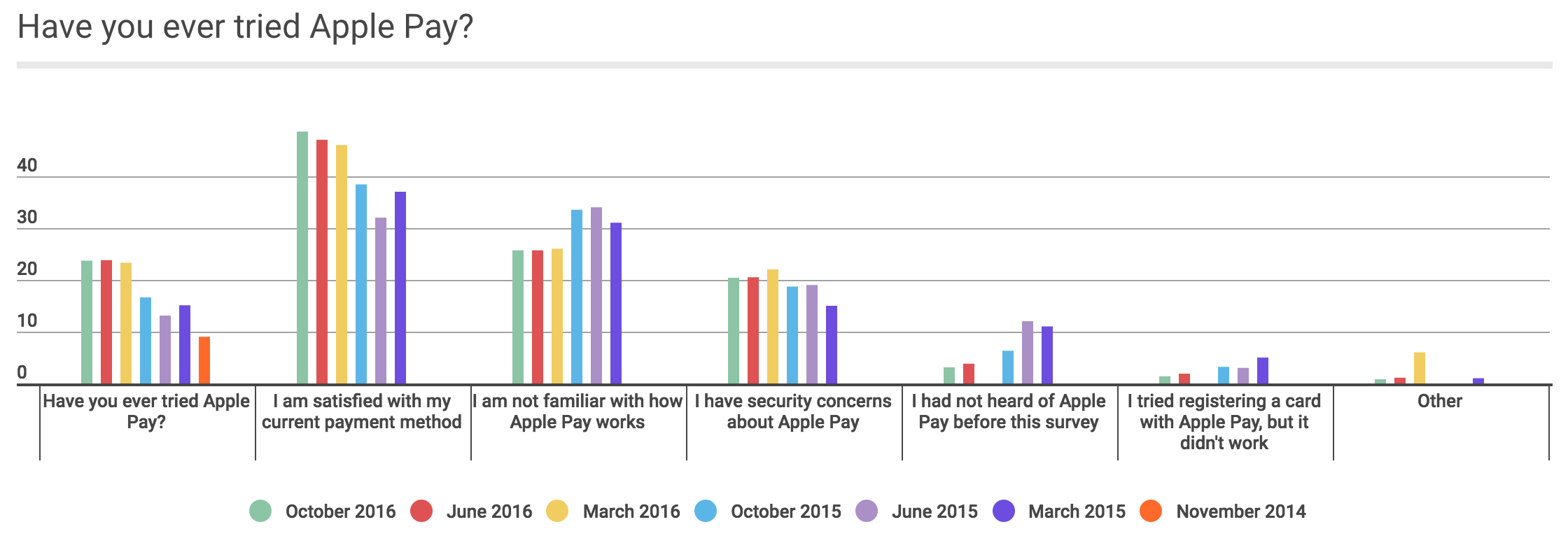

Do people not use mobile in-store? 84% of smartphone shoppers use their devices to help shop while in a store.2 But only a few use their devices to pay. The dominant reason for not using mobile payment is because people are ‘satisfied with their current payment method.’3 It is challenging to convince that mobile payment is more convenient and easy to use when the delta of seconds between swiping a credit card and tapping your phone is not significant.

Why People Don’t Use Apple Pay (Source: PYMNTS.com, October 2016)

Coin chooses to take only half a step

Coin has been driven to develop technology that makes payments more simple and secure.4 The company is not trying to take one giant step and replace the physical wallet with a digital one. Instead, Coin is trying to reduce all of the credit, debit, gift and loyalty cards that clutter up our wallets to a single piece of plastic.5 It does not attempt to change the behavior of swiping a card.

This concept created a lot of buzz with its video that portrays the user experience. With this video, Coin received pre-orders in November 2013 using its own crowdfunding campaign, and blew past the $50,000 goal in less than 40 minutes. Not only did Coin raise an incredible amount without any prototype, but it also created several competitors who jumped into develop the same concept.

Screenshot of YouTube:One Coin for All of Your Cards 6

Coin’s bold venture comes to an end

Despite all the anticipation, Coin kept 10,000 beta users waiting for 2 years before delivering its first product in 2015. Not long after, in May 2016, Coin was acquired by Fitbit in May 2016, but not for its all-in-one card product. Fitbit announces that the current Coin gadget will be left out of the purchase, and their expectation is that Coin will accelerate Fitbit’s ability to develop an active NFC payment solution.7

Here are a few reasons why Coin hit a roadblock:

- Coin ran into immense technical issues. It took the company two years to resolve all of them and finally develop the product they had promised. Yet, the swiping was not successful in a significant number of occasions. This hinted that more time and technology development will be required as it attempts to improve the product moving forward, allowing the competitors to catch up in the meantime.

- Credit card companies were enhancing security by implementing EMV chips. Coin managed to load EMV chip cards onto its device and have users tap the card reader as you would for Apple Pay. However, the real challenge was coming when all credit card companies implemented EMV chips and all the POS finally required all the cards to be inserted and not swiped.

- Coin might not be able to get any partners on board. Coin had not secured approval with any of the major credit card issuers and networks it hopes to work with, nor had the company gotten a sense of whether the industry would embrace it.

How can we bring payment into the digital world?

We should educate consumers on security. To remove the first barrier, we need to constantly communicate that the card information is encrypted and is securely handled. Similar to how consumers now feel more comfortable typing in their credit card information for online purchases, we want more users to increase trials and learn that mobile payment is as safe.

We want consumers to remember to use it repeatedly once they adopt it. Most consumers will think of ‘payment=card or cash’ rather than ‘payment=mobile’ so we might want an integrated mobile app that involves consumers throughout the whole shopping journey. If the app gets shoppers to create shopping lists, look at deals, and locate products along the way, there may have a high chance of reminding people to use their phone to pay.

We should also educate merchants. We want to have as many merchants on board as possible, without making them think they’re just sharing purchase data with the mobile payment company. Some ways of proving that we can add value could be to communicate that adopting mobile payment will draw more foot traffic or to offer data analysis around consumer behavior patterns.

(791 words)

References

- eMarketer: Mobile Payments in the US Growing Fast, but Still Far from Mass Adoption https://www.emarketer.com/Article/Mobile-Payments-US-Growing-Fast-Still-Far-Mass-Adoption/1014689#sthash.kOjGy2Pt.dpuf

- Mobile In-Store Research: How In-Store Shoppers are Using Mobile Devices https://ssl.gstatic.com/think/docs/mobile-in-store_research-studies.pdf

- Apple Pay Adoption http://www.pymnts.com/apple-pay-adoption/

- Coin Blog: Coin Wearable Payments Platform Acquired by Fitbit http://blog.onlycoin.com/coin-wearable-payments-platform-acquired-by-fitbit

- Y Combinator: Meet Coin http://blog.ycombinator.com/meet-coin-yc-w13-a-startup-creating-a-universal-credit-card/

- One Coin for All of Your Cards https://www.youtube.com/watch?v=w9Sx34swEG0

- Fitbit is Buying Coin http://www.theverge.com/2016/5/18/11700658/fitbit-coin-acquisition-announced

I’ve always found the scale of Coin’s failure fascinating. I find it hard to fault the consumers in this case; I believe the industry has not yet risen to the challenge of providing a truly flawless, integrated, and completely substitutive experience. In the case of Coin and ApplePay, it is still only accepted in a limited number of locations; therefore, you still need to carry around your old cards, completely defeating the point of reducing clutter. Think of digital receipts and why these have not taken off; each company wants you to give them your email address and there is no integrated solution out there.

The experience also needs to be easy and transparent; the complexity of Apple Pay is still too high in my opinion. I tried it once, and after fumbling with the terminal for a minute trying to get it to work, I gave up and returned to using the cards. I suspect many people would also be turned off by such an experience. Paying usually has a time constraint, and if you can’t figure it out within 30 seconds, you are going to go back to your backup method as a lot of times you have a line behind you or some other sort of time constraint. I would like to see these initiatives be developed more, as there is definitely strong market demand for these products and services.

Jaime

Thanks for writing this Lane! Reading this article, I wasn’t quite sure how much value Coin was actually adding by just creating a consolidation layer to the payment system. Agree users would like to have thinner wallets, but given the incremental change (switching from many cards to one card) I’m not quite sure if they would be willing to pay $100 for it. To me, it seems that their business model and customer acquisition model was not well thought through. It’s interesting to compare ‘consolidation wallets’ like Coin to the popularity and rise of mobile wallets such as Venmo. These mobile wallets are typically free for the user and create significant value with their easy of use and interaction. Venmo did an incredible job of creating a network of users on its platform and making its name synonymous with P2P payments. Given this large consumer base, it could now move into B2C payments and help monetize the platform

[1] http://www.tradestreaming.com/2016/02/08/venmo-wants-to-power-b2c-payments-not-just-p2p