In Too Deep? The Future of Flood Insurance in the Face of Climate Change

Perhaps no industry is more exposed to climate change than the insurance sector. Climate change accelerates the frequency of natural disasters, ranging from hurricanes, flooding, severe drought and wildfires, with more than half of all natural disasters linked to financial disasters linked to climate change [1].

In the U.S., more than 100 million people live along coastal areas [2] and 9 million live on low elevation zone areas that are less than 8 feet above the local tide lines [3]. Given the scale of the population exposure to flood zones, the financial and logistical challenges involved in assessing and addressing flood risk due to global warming have been immense. The U.S. has experienced its worst run of natural disasters over the last two decades, with the greatest financial losses stemming from flood-related disasters such as Katrina ($150 billion), Sandy ($50bn), Hurricane Andrew ($45bn), Midwest Floods ($34bn), Ike ($30bn), and more than a dozen others that have yielded losses of over $10bn[4].

Pricing Risk: Funding the NFIP

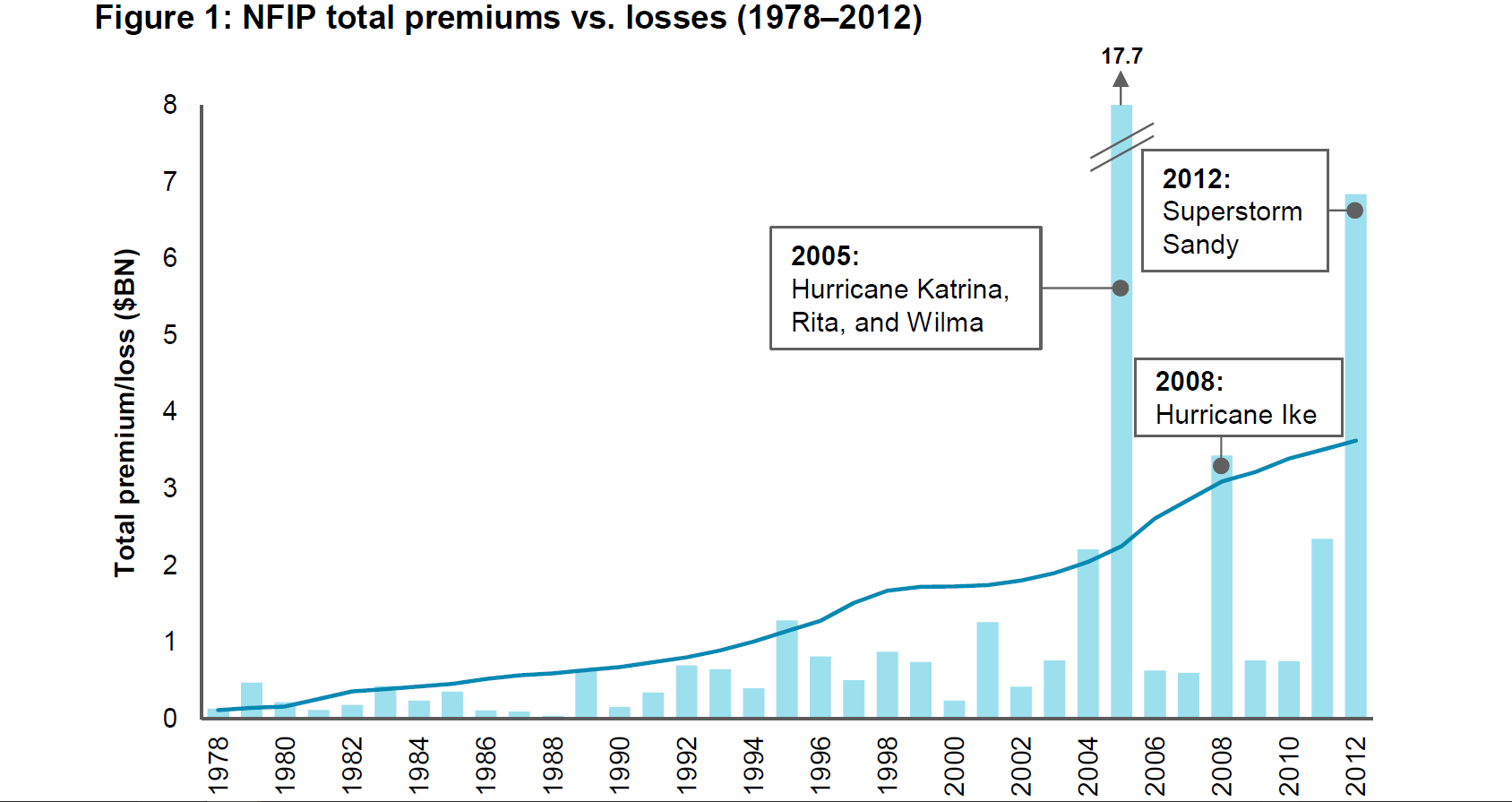

The bulk of flood insurance in the U.S. is underwritten by the National Flood Insurance Program (NFIP), a division of the Federal Emergency Management Agency (FEMA). In 2016, the NFIP underwrote nearly 6 million flood insurance policies and collected $3.5bn of flood insurance premiums. Unfortunately, the premiums are nowhere near enough to the scale of risks assumed. The value of flood-insured assets along the U.S. Coastal areas is roughly $10.6 trillion, with $1.25 trillion directly assumed by the NFIP [5] highlighting the scale of insurance funding gap. In the last decade, the NFIP has incurred $30bn in losses and still owes $24bn in outstanding debt to the U.S. Treasury that it is unlikely to repay.

Climate Change and the Challenge of Insuring Flood Risk

Insuring flood risk is particularly challenging because of the scale of the underlying financial risks, and the difficulty in mitigating the risk profiles of those affected since this would require mass relocations of millions of people living in flood plains in the U.S. Forecasting the risks becomes particularly challenging in the face of climate change, but it is expected that by 2050, annual flooding losses in the world’s coastal cities is expected to hit $1trillion globally, with nearly 40% falling on four cities, three of which are in the U.S, i.e. New Orleans, Miami, and New York [7].

Insuring flood risk has some fundamental issues. First of all, assessing flood risk is difficult since it requires complex assessment methodology that needs to take into account the geographic distribution of flood maps of the entire country to a very high degree of accuracy, typically within a meter – and also requires assessment at a property level to determine the specific premiums that a particular premiums that a specific property should be charged. Without subsidization, the cost of any kind of insurance premium should – at a very basic level – match the value of the insured asset versus the probability weighted risk of the incidence occurring. Part of the challenge in flood insurance is that the incidence of flood risk has increased significantly as a result of climate change, but the insurance premiums that the NFIP charges are typically locked in for extended periods. Thus, thirty years ago, a household may have been located in an area with a 1:500 flood risk area (i.e. with the risk of flooding estimated at 1 in every 500 years), but the risk may have changed during the same time to 1:30 due to climate change. The magnitude of this change highlights how significant the change in premiums needs to be to actually address the risk. Removing the subsidies would drive up the premiums for a house by tens of thousands of dollars a year, with many households in the U.S. potentially expected to pay over $100,000 in insurance premiums. These premiums are out of reach of many households, and this has led the NFIP to maintain old premiums for households under it’s “grandfathering” practice [5].

The financial risks faced by the NFIP are urgent and immense. In the long run, it will be necessary to push for more regulation to ensure that the subsidies in flood risk are eliminated so that premiums reflect the fully-baked in costs of the financial risks assumed by property owners. However, political pressure to maintain existing rates means that this strategy is untenable. In the short-to-medium term, the NFIP should pursue a number of options to start addressing flood risk, including:

- Instituting and promoting flood prevention measures at a property level, including adjusting premiums to reflect changes taken by homeowners to reduce risk such as: setting up basement enclosures, elevating buildings and moving contents higher above ground

- Adjusting flood maps to properly reflect flood risk

- Including the impact of climate change on premiums by including the risks associated with future sea-level rises and increased risk of storms

- Instituting mandatory insurance in flood areas to reduce the degree of subsidization

- http://news.nationalgeographic.com/2015/11/151105-climate-weather-disasters-drought-storms

- http://www.climatecentral.org/news/new-analysis-global-exposure-to-sea-level-rise-flooding-18066

- http://www.climatecentral.org/news/new-analysis-global-exposure-to-sea-level-rise-flooding-18066

- https://www.trustedchoice.com/insurance-articles/weather-nature/most-expensive-disasters/

- http://www.ucsusa.org/global_warming/science_and_impacts/impacts/flood-insurance-sea-level-rise.html#.WBz8JPkrJPY

- (2013). Flood Insurance – Strategies for Increasing Private Sector Involvement

- http://www.climatechangenews.com/2013/08/19/flooding-could-cost-us1-trillion-a-year-by-2050/

I’ve always been interested in learning more about the flood insurance business. Frankly, I am shocked to learn that premiums have been locked despite there being such a drastic change in the flood risk across the country. From what you wrote, it seems like NFIP finds itself in a very difficult situation: they don’t have the power to change premiums (I’m guessing this power lies at the congressional level given the FEMA connection) but are expected to provide coverage despite the persistant climb in flood risk.

Although it makes sense for the organization to adjust flood maps to reflect risk, it appears that this data doesn’t empower the organization to impact change. As you mentioned, assessing flood risk is a challenging endeavor to take on, but it must be so demoralizing to see that work go to waste. The existing NFIP business model doesn’t seem to be sustainable long-term, in fact, they already have existing debt that they are unlikely to pay. I agree that the NFIP should institute mandatory insurance in flood areas and that premiums should reflect increased regional flood risk. I also agree that mass relocation is impractical, but perhaps insurance plans can have “baked in” incentives to encourage people to move away from high risk areas in the even that their current property gets hit by a major disaster.

Do people continue to rebuild and live along these high risk zones after a major disaster? If so, does the NFIP continue to offer flood insurance? While encouraging mass relocation will certainly have large macroeconomic impacts on the local and regional economy, I wonder if its more devastating to the economy to have to rebuild the same community after each new environmental disaster.

Very interesting article that shows how difficult it is for the P&C insurance industry to adapt to changing conditions. It is so early that statistical patterns cannot really be extrapolated.

Even though the public funding would ultimately provide relief in case of tail event leading to bankruptcy, I agree that some measures could be taken as soon as now. The article outlines some of those that make sense such as incentivizing for protection & remedy investments, similarly as you would pay smaller premia if you invest in a reinforced door.

These pro-active measures could be great mitigants but are likely to come with public dissent given climate change & floods always seem remote. Those measures could be enacted on the wake of large floods to use the public sentiment. For instance, you could also imagine a law that forbids to reuse flooded area for residential or heavy commercial purposes (e.g. limited to storage, parking, etc.).

Another interesting aspect that the article keeps silent is the impact on properties prices. I would be curious to see the impact on prices of actual or potential floods? The market probably adjusts better for actual flooded areas. I would have thought that given prices go down, people are likely to have a reversion to the mean behaviour whereby they tend to come back provided that the area is will located close to economic centers.

Another mitigant could be to have a supra-national solutions either public or private. By pooling risk at higher level, one could reduce the impact of tail events that would still nevertheless become more frequent. This could also improve returns on invested premia.

Large reinsurers (MunichRe, Lloyds, etc.) are currently running their model to see how they can prepare themselves best for this!

As Guillaume Gorge [1] noted “Insurance is built on a paradox”, insurers can get free financing from float but that is only after they have gained trust usually from large amount of locked long term capital. These models will change as well!

[1] Guillaume Gorge Insurance Risk Management & Reinsurance

Very interesting article. I am a little skeptical of the data that ties climate change to the increased frequency of natural disasters. It seems that scientists’ “confidence has risen” [1] when looking at techniques which link climate change and natural disasters. Intuitively, it makes sense. However, I think we will have to collect more data over time to prove this conclusively.

Taking this assumption as fact, FEMA’s response to this problem is concerning. The agency has launched a reinsurance initiative to insure itself [2]. If events continue to escalate in frequency and possibly severity, the agency is no longer exposing just itself, but global markets as a whole. I am concerned that instead of taking the actions you outlined, it is just delaying the eventual wakeup call – and increasing the exposure.

[1] http://news.nationalgeographic.com/2015/11/151105-climate-weather-disasters-drought-storms/

[2] https://www.fema.gov/national-flood-insurance-program-2016-reinsurance-initiative

This piece reminded me of the finance concept we learned surrounding idiosyncratic vs. systematic risk. In distinguishing between these two concepts, our textbook gave the example of theft vs. earthquake insurance (p335), explaining how the former should be relatively isolated while the latter may be widespread. Interestingly, while the risk of each incident is about the same, the implications are quite different, leaving earthquake insurers holding (or supposed to be holding contrary to the article’s evidence above) large reserves to cover the possibility of a large claim. While the likelihood of payout was generally pretty small (earthquakes don’t hit all the time), when it did hit it was a massive payout. In this case, flood insurance is akin to earthquake insurance. However, I worry that the concept of insurance to protect against uncommon events will instead morph into a different version whereby events are much more common and premiums are high and therefore unaffordable, (presuming actuaries model this in and they can be increase the price, though I note CEA’s point above). There are many possible implications, ranging from more frequent claims, to unsustainable business model (as David points out), to lower coverage if rates in fact were to rise. This leaves neighborhoods at risk and local/state governments to pick up the pieces (via taxpayer dollars).

David, this in a very interesting article. From one perspective, citizens around the globe (especially in the US, considering the facts in the article) are constantly at risk of losing their properties due to natural disasters, which are more likely to occur in case the climate change effects are not mitigated. On the other hand, as you said, insuring flood risk is extremely challenging because of the complexities on forecasting the outcomes associated with climate changes and because of the massive premium needed to cover for potential losses.

I think that one alternative to reduce the financial burden on the NFIP is to create a national contribution that would require each household (excluding those citizens in very poor financial condition) to collect a monthly payment aimed at covering for the costs associated with natural disasters. According to the results of the last Census, the United States has approximately 115 million households. If on average each household paid $ 20 per month, the federal government could collect almost $ 30 billion annually, an amount that could offset the NFIP current losses. I know this recommendation also carries several risks and limitations, but I think this is a debate that governments around the world should at least take into consideration.

Excellent article, thank you for sharing. Aligning premiums with risks comes with a few concerns. Climate change has diminished the usefulness of historical data for actuarial purposes. Risk is higher, but uncertainty is extreme. This leads insurers to price for radical scenarios, causing much higher prices. We’re already seeing that for property insurance. The effect would be more severe for flood insurance, because claims are almost always total losses.

Flood insurance priced accurately would cost as much as many houses (the median U.S. home costs $189,000). Your recommendation to enforce mandatory flood insurance in prone areas would force massive relocation, because the houses would simply not be worth it. Eliminating these risks would be financially beneficial for the government and insurers. Personally, I think it’s ridiculous that people rebuilt in the bottom of the New Orleans “soup bowl”. But people love their communities. There are serious human and property rights concerns with this proposal, but I think it’s worth an international discussion.

Extremely interesting, and certainly an important business issue to consider. I am curious on your point regarding more accurate premiums. In a world where we expect higher premiums, I would expect flood insurance would be less attractive for the end consumer. It will certainly be an interesting social dynamic to see how populations move throughout the world based on projected weather impacts. Your work also has interesting parallels to the market for earthquake insurance. I would be interested to see how many of these outcomes overlap for that market, though would expect that it would be similar in many ways.

This piece is very interesting and highlights one of the critical businesses that has a lot to think about with rising sea levels. It’s intriguing to look at how a firm assesses flood risk in the face of our changing global climate. Not only are the worlds sea levels rising but the occurrence of volatile weather patterns are increasing as well. This I’m sure makes the job of the flood insurance company even more complicated. Also, I have a question about the psychological impact that purchasing flood insurance has on a homeowners view of global warning. Once somebody has purchased flood insurance, the presumption would be that they are now indifferent to whether their house floods or some would even welcome it in order to get a large payout and a new house. Therefore, are those who insure themselves against floods making themselves ambivalent towards climate change?

I am simply fascinated by the level of complexity of this problem. Global warming aside, forecasting weather is an extremely imprecise practice especially over long time horizons. Just try to look up the local weather on day 10 of the 10-day forecast. Add to that the issue you raise of the present funding gap between insured assets and insurance premiums and the future acceleration of destructive weather caused by climate change and you end up with a worryingly unstable flood insurance market. I am curious to see how flood insurers respond to their increasingly risky exposure and at what point communities in flood-risk zones move in response to increasing flood probabilities. These questions are related and will involve civilians, insurance businesses, and local governments working together to address entirely.

David – this is an extremely interesting blog. I have lived in both South Florida and New York City. I was actually living / working in the southern part of Manhattan when the city was hit by Hurricane Sandy, flooded, and left without power. It was a pretty crazy experience – no power, no open stores, and limited people in one of the world’s greatest cities. The situation in South Florida is even worse, given how much of the state sits below sea level. I was shocked by some of your discoveries re: the insurance industry, especially that the NFIP still owes $24 billion to the US government. It doesn’t seem like there is any near team solution given the NFIP’s funding issues and people’s inability to afford higher insurance premiums on their homes. Is there another alternative or solution that will work going forward? Thanks for bringing attention to this topic!

I am concerned about what I feel will be the inevitable consequence of the current NFIP system: insolvency and people left holding the bag after a major disaster. I am particularly interested in this because I left Baton Rouge to come up to Boston literally 12 hours before the worst floods there took out an entire suburb. Denham Springs (eastern part of Baton Rouge) experienced 90% loss of housing with the remainder in poor shape as well. No one even took flood insurance since they never expected it and as you can imagine, FEMA is now trying to take care of the situation. Unfortunately, these kinds of events have to start occurring more frequently in order for true political change can occur.