The insurance industry is poised to be one of the major industries most effected by climate change. Insurance companies are paid to bear risk and many of the insurance policies that they hold are becoming increasingly risky as a result of the effects of climate change, including more powerful storms and rising sea levels. Over two decades ago, the then president of the Reinsurance Association of America was quoted to say “It is clear that global warming could bankrupt the industry.”1 Today, we are presented with meaningful examples of the financial threat to insurers with mega-storms like Hurricane Sandy and other natural disasters “generating $35 billion in privately insured property losses” in 2012.2

Allstate Insurance is the second largest property casualty insurer in the US, with $24.8 billion in net premiums written in 2013.3 In 2015, Allstate wrote 6.5 million homeowners insurance policies on privately owned property.4 Separately, Allstate estimates its agencies have “approximately $1.3 billion of non-proprietary personal insurance premiums under management, primarily related to property business in hurricane exposed areas.”5 Going forward, what are the risks and opportunities of climate change for a major insurance player, like Allstate? What is Allstate doing now and what future actions will it take to address climate change?

Climate Trends and Liability

Climate change threatens insurance companies’ fundamental business model for property insurance. The business model consists of insurance companies assessing the risk on a property, in terms of consequences and probability of particular events, and then calculating a price for the insurer to assume the risk for the customer. Embedded in that price are assumptions about how much the insurer will need to pay out to all policy holders over time.

Stated plainly, climate change affects the costs incurred by Allstate to support insurance policies. Climate change increases the consequences and probability of property damage, thus impacting the significant portion of Allstate’s business which involves writing casualty insurance policies.

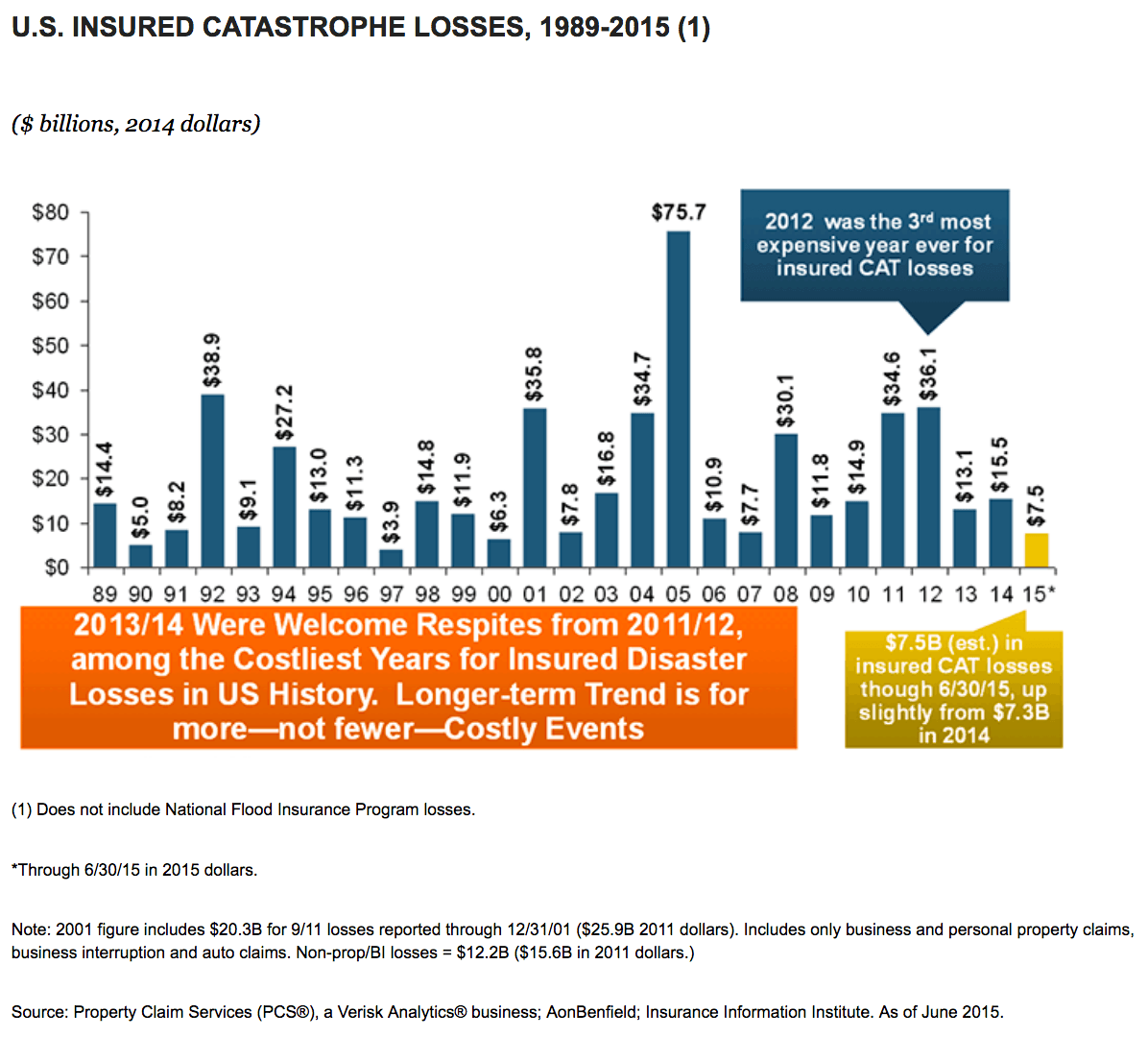

As shown below, the amount of insured catastrophic losses in the US over the last 25 years reflects increasing volatility with the most extreme spike in 2005 for Hurricane Katrina with $75 billion of losses and then $30+ billion of losses in each of 2008, 2011, and 2012.6 The graph below shows increased frequency and expense of catastrophic events in the US that may not have been accounted for in prior risk assessments. These losses suggest that some meaningful portion of Allstate’s 6.5 million homeowners policies have and will be effected by changing conditions.

Policy Adaptation

Allstate has adapted its policies in response to the effects of climate change in recent years. However, the insurance industry as a whole has been relatively slow to adapt to climate change, despite its serious impact and long term awareness of the issue. Allstate produced a corporate responsibility policy that states “Climate change could pose considerable challenges to the insurance industry due to increased volatility and frequency of extreme weather, and the effect it could have on pricing and availability of insurance products.”7 Allstate’s overall strategy includes short and long term items that fall into a few specific categories:

- Restricting or denying policies in vulnerable geographies: Allstate is seeking to minimize its risk by limiting exposure to areas where weather is expected to become increasingly extreme, specifically stating that Allstate is “continuing to restrict new homeowners business in certain geographic areas [. . .].”5 The effects of these practices are already manifesting themselves in the market with Allstate “canceling or failing to renew policies in many Gulf Coast states because of the risk of hurricane damage.”8

- Raising premiums and introducing new deductibles: In order to compensate for the costs associated with increased probability and severity of climate change related consequences, Allstate is taking actions like raising premiums (increase the amount it takes in annually) and “implementing tropical cyclone and/or wind/hail deductibles where appropriate,”5 (decreasing the required payout when such events damage insured property).

- Purchasing reinsurance: Allstate is “purchasing reinsurance for specific states and on a countrywide basis for personal lines of property insurance in areas most exposed to hurricanes.” Reinsurance (effectively insurance for insurance companies) is a product that insurance companies can purchase in order to provide additional risk protection on the policies they hold.

Future Progress

Going forward, Allstate will need to continue to build upon the actions it is already taking and expand their efforts to protect the company and customers. Specifically, Allstate will need to constantly reevaluate and update their risk assessment models to adapt to new data and information about the state of climate change and ensure adequate pricing strategies. Additionally, Allstate should consider introducing strengthened financial incentives (e.g., lower premiums and deductibles) to help change customer behavior and encourage customers to invest in fortifying their properties against the impacts of climate change. (798 words)

Footnotes / Sources

[1] Los Angeles Times. 2014. “How the insurance industry sees climate change – LA Times,” http://www.latimes.com/opinion/op-ed/la-oe-linden-insurance-climate-change-20140617-story.html, accessed 03 November 2016.

[2] Eduardo Porter. 2013. “Insurers Stray From the Conservative Line on Climate Change – The New York Times,” http://www.nytimes.com/2013/05/15/business/insurers-stray-from-the-conservative-line-on-climate-change.html, accessed 04 November 2016.

[3] Investopedia. 2016. “Top 10 Insurance Companies By The Metrics | Investopedia,” http://www.investopedia.com/articles/active-trading/111314/top-10-insurance-companies-metrics.asp, accessed 03 November 2016.

[4] The Allstate Corporation Notice of 2016 Annual Meeting, Proxy Statement and 2015 Annual Report, p. 108.

[5] CDP, Climate Change 2015 Information Request, Allstate Corporation

[6] Insurance Information Institute. “Catastrophes: U.S. | III,” http://www.iii.org/fact-statistic/catastrophes-us, accessed 03 November 2016.

[7] Allstate Corporate Responsibility | Climate Change. 2016. “Allstate Corporate Responsibility | Climate Change,” http://corporateresponsibility.allstate.com/environment/climate-change, accessed 03 November 2016.

[8] Richard Lou, et al., Municipal Climate Adaptation and the Insurance Industry, Emmett Environmental Law & Policy Clinic, Harvard Law School, Cambridge, Mass.: April 2012, p. 11.

Removing a portion of the business whose revenue stream has an outsized amount of variability is a wise decision on Allstate’s end. As stated in the article, Allstate’s biggest challenge will be to balance the use of reinsurance while shifting the business to other sectors with more stable cash flows. Because Allstate is moving out of areas such as the Gulf region, it creates an opportunity for other private insurers to move into the market and take on more risk. If technology improves over time such that it becomes easier to forecast future weather patterns, these new competitors will already have a foothold in this market. It is thus important for Allstate gradually make changes to its business model instead of knee-jerk reactions otherwise it will risk losing significant market share in the longer term.

Thanks for the great article and analysis. One piece of Allstate’s policy that intrigued me was #1: restricting or denying policies in vulnerable geographies. Allstate is free to choose which markets it wants to do business in, and there are benefits to this. Indeed, by choosing not to do business in especially risky areas, Allstate can effectively signal to would-be homebuyers that the area is not safe for a home.

However, I was surprised that Allstate was opting to cancel or fail to renew policies in certain circumstances. This seems like an incident of Allstate mispricing risk: perhaps they failed to account for the climate change impacts mentioned in the beginning of the post. Now, the homeowner may have mis-assessed the risk as well. But Allstate canceling the policy seems to be shifting all risk onto the homeowner, leaving him out to dry. If Allstate cares about the well-being of its customers, it should be careful not to punish certain customers for its own mistakes.

Allstate seems like it is taking very sensible steps to respond to global warming.

One thing Allstate could do to spur greater preparation for global warming is publicize further in what geographies it is restricting coverage and explaining why. While perhaps opening itself to some negative press, this move could help those communities that are most at risk of global warming’s effects face the future sooner and demand that their elected officials take more action now.

Another idea to highlight Allstate’s sophisticated analysis is to offer public bets on global warming’s effects. Especially in the United States where this is a vocal, influential minority dismissive of global warming’s effects, public bets could help make skeptics of global warming’s effects put their money where their mouth is and generate some positive buzz for Allstate showing its confidence in its assessments of global warming and willingness to take a stand behind them. (see this post describing public bets – often in the context of election forecasts – as a tax on ‘lies’ – http://marginalrevolution.com/marginalrevolution/2012/11/a-bet-is-a-tax-on-bullshit.html).

Great post! I’ve seen first-hand how insurers can really “punish” those living in riskier geographies with their high premiums. My family owns property in the Florida Keys and after several damaging hurricanes (we lost our house during a Tropical Storm in 1998), many property insurers would not insure us until we took certain measures to prevent future catastrophes.

Here is where I struggle with Allstate’s decisions to better position the company for the effects of climate change – rather than leave customers “out to dry” as @Dan Routh mentions above, I would rather see Allstate invest in better infrastructure for these risky geographies to better withstand extreme weather conditions. For example, much of the Florida Keys experiences high levels of flooding during rainy seasons and hurricanes, causing severe damage to homes in these areas. Perhaps Allstate should partner with development companies to help design and construct houses that are above sea-level to mitigate flooding going forward? Or, maybe they should encourage the local governments to install better draining systems throughout the cities to ensure that excess water moves out quickly? These types of investments would alleviate much of the high costs associated with hurricane damages, while also helping customers living in these geographies. Further, these changes would create longer-term solutions to climate change rather than just shifting the financial burden to home and property owners.

Great post – based on Dan Routh and Ship Mate’s reaction, I’m left wondering if there’s a policy-oriented angle to this question as well. A good example is the National Flood Insurance Program, a public-private partnership run by FEMA that imposes flood-plane management guidelines on communities and insures property owners against losses, up to a certain cap. Perhaps similar programs can be put in place for other types of severe weather events as well (although of course, the irony is that any legislation to expand such a program would require at least a tacit admission from politicians that climate change is real).

To Dan’s point about where Allstate chooses to do business, I am reminded that often those who are most prone to climate change-related damage are the ones least capable of recovering from extreme weather incidents, as lower-income families are least likely to invest in improvements to their properties and are unable to easily move to lower risk areas. I realize it is not Allstate’s responsibility to protect these customers, but if not private insurance, then who?