Predicting your casualties – how machine learning is revolutionizing insurance pricing at AXA

Insurance giant AXA, frequently classified as ‘archaic and static’, is now embracing machine learning and real-time driver data collection to determine individual car insurance premiums.

The auto insurance pricing model disruption

Historically, auto insurers have relied on linear regression of a limited number of risk factors, partly reported by the policyholder on a basis of trust, to determine an individual’s insurance premium [1]. Fierce competition among insurers and low customer switching costs have since emerged as the main drivers that force insurers to determine a competitive insurance price which covers their incurred costs [2].

An adequate prediction of future insurance cost on a case-by-case basis is thus becoming a business imperative [1]. Against that backdrop, machine learning algorithms present an incredible opportunity as they are capable of calculating risk premium estimates based on real-time analysis of massive amounts of policyholder data. Data collection is facilitated through ‘telematics’, devices that are installed in policyholders’ cars and collect data that make driving behavior measurable (e.g., speeding, harsh breaking) [3]. In combination, this allows for more flexible and accurate auto insurance pricing models such as ‘safe driving discounts’ or ‘pay-by-mile’, that take individual behavior into account [4].

How AXA is using machine learning

AXA has started to position itself at the forefront of embedding machine learning (ML) in their auto insurance pricing approach.

In the short term, they are forming strategic partnerships with fast-moving tech startups and building on open source ML algorithms to introduce their new pricing solutions with particular focus on their strategic test markets – Western Europe and Malaysia. In the UK AXA’s partner ‘By Miles’ is providing the device, software, and app to collect and visualize real-time driver data [5]. In Malaysia AXA has developed and introduced its own app ‘AXA Flex Drive’ which is compatible with the telematics data collection device from its local partner ‘CSE Connex’ [6]. AXA is working on complementing the traditional list of relevant risk factors (e.g., driver age) through new items such as real-time vehicle diagnostics and maintenance results. The collected data is processes through the open-source deep-learning framework ‘tensor flow’ [7].

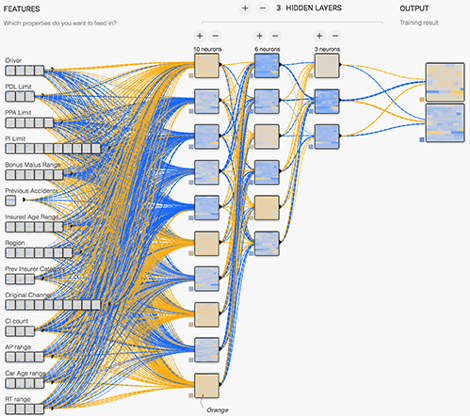

In the mid-term, AXA is pursuing its broader vision to drive the transition from being a ‘bill payer’ to becoming a true partner for its policyholders across all their auto insurance products [8]. Execution on this strategy is planned to take place locally with individual solutions and partnership introduced per country. On a group level, AXA will work on refining its deep learning model (see Figure 1), extending data sources, and building additional partnerships with telematics/ML providers to increase the accuracy of its risk premium predictions [9].

Defining the future of auto insurance with machine learning

To build a long-term sustainable competitive advantage through machine learning, I believe AXA must take three additional steps to complement its short- and mid-term efforts: 1) Take policyholder data collection in house; 2) Synchronize rollout of ML/telematics solutions to all its geographic locations; 3) Become the key player in accident prevention through real-time insurer-to-driver feedback.

The reasons for taking these specific actions can be summarized as follows: 1) Owning proprietary data allows AXA to collect and learn from large amounts of data that are not publicly available, which lowers the risk of being disrupted by new market entrants that train their ML algorithm through data made available by non-exclusive partners; 2) Being the first-to-market with integrated ML/telematics solutions like AXA Flexi Drive across regional markets can provide the necessary impulse for price-sensitive policyholders to switch to AXA and stay due to its strength in rapid innovation for accurate pricing; 3) Taking responsibility for goals beyond its own profitability, AXA can demonstrate superior customer focus and contribute to the joint goal company-customer-government goal of radically reducing fatal accidents – a concrete suggestion is to embed safety push messages in the AXA application (e.g., fatigue warnings) and offering alternatives to unsafe driving (e.g., taxi contractor).

Protecting interests of the ‘see-through’ consumer

With policyholders granting insurers real-time access to sensitive data, the two most pressing questions are 1) Do we need to create a relevant ethical and regulatory framework to restrict and audit machine learning/telematics applications in (auto) insurance? and 2) How can the individual be protected from unforeseen uses of the data collected (e.g., use as evidence in lawsuits, speeding tickets)?

(700 words)

References

[1] Verbelen, R., Antonio, K., Claeskens, G., “Unravelling the predictive power of telematics data in car insurance pricing.” Journal of the Royal Statistics Society, Applied Statistic 67(5) (2018): 1275–1304

[2] Smith, K., Willis, R. & Brooks, M., “An analysis of customer retention and insurance claim patterns using data mining: a case study.” Journal of the Operational Research Society 51(5) (2000): 532

[3] Deloitte, “Auto insurance telematics – The three-minute guide.” https://www2.deloitte.com/us/en/pages/deloitte-analytics/articles/auto-insurance-telematics-the-three-minute-guide.html, accessed November 2018.

[4] M. F. Carfora et al., “Soft Computing – A Fusion of Foundations, Methodologies and Applications.” Soft Computing 22(236) (2018)

[5] Insurance times, “AXA partners with insurtech start-up to target less frequent drivers.” April 12, 2018, https://www.insurancetimes.co.uk/axa-partners-with-insurtech-start-up-to-target-less-frequent-drivers/1426847.article, accessed November 2018.

[6] AXA “The 1st Telematics Motor Insurance That Rewards You For Being A Safe Driver.” https://www.axa.com.my/axa-flexi-drive-telematics, accessed November 2018.

[7] Sato, Kaz. “Using machine learning for insurance pricing optimization.” Google Cloud, March 29, 2017, https://cloud.google.com/blog/products/gcp/using-machine-learning-for-insurance-pricing-optimization, accessed November 2018

[8] AXA “How can insurance make roads safer for all?” https://group.axa.com/en/newsroom/news/20170511-insuring-safer-roads, accessed November 2018

[9] Van Egghen, Robert. “Axa using AI to boost manager performance.” 5 April 2017, https://www.essentia-analytics.com/essentia-news-and-media/axa-using-ai-to-improve-investment-performance/, accessed November 2018

Use of data collected from telematics with machine learning to customize insurance premium for customer seems viable and could be the future of overall insurance industry. However, I believe there are several issues that may need to be addressed.

1. Which party “AXA or customer” should be the one to bear cost of telematic?

2. Placing telematic to track customer car usage may create tension on privacy of individuals

3. As customers in the insurance industry usually a price-sensitive consumer, the use of machine learning may not create an edge for AXA, since the business will likely flow to provider of the lowest premium.

Great paper – I agree that better underwriting can generate a sustainable advantage for an insurance company. I wonder about the social implications of putting trackers and cameras in every car. Would the resulting underwriting become more discriminatory (like the pre-ACA U.S. health insurance system where insurers were denying patients based on pre-existing conditions)? Are there other concerns with a private corporation having a comprehensive record of every driver’s activity data?

Fascinating topic! It seems extremely technical, but somewhat of a no-brainer for AXA to use machine learning to improve its models and give it a pricing “edge” versus the competition, but I also have to wonder if there is an element of “false precision” that comes from these models. For example, how accurate is long term/short term historical data actually useful in predicting future probabilities of accidents/claims in an industry where the tech in cars is rapidly evolving to reduce/eliminate these risks? Is machine learning any better at making these estimates than more traditional methods? Just a thought.

Thanks, Talitha! The idea of social responsibility and consumer privacy protection are paramount in this discussion, and I think the two can be related. Specifically, I believe that consumers are less averse to being monitored when they believe that they are serving a greater cause. This is especially true with the millennial generation, who want their companies to stand for more than profit. By using the data to do more than orchestrate a pricing model, AXA has the potential to achieve their profitability desires, save human life, and earn customer loyalty!

Thank you for a great article on a very interesting subject! Telematics is probably the future of auto insurance, and as you mention is increasingly used by major insurance providers. As to your question about ethics, this is a very interesting topic in the insurance world in general – since one of the main reasons for insurance to exist is to collectivize the risk, more information is not always good. If you are perfectly able to predict the risk of any one customer being in an accident, why would you not charge the full cost that you are expecting to that one customer? This can have fatal consequences especially in medical insurance, where someone with a high risk of cancer might be denied, or priced out of, any kind of medical insurance. In my mind this is an area that needs to be regulated, and quite heavily so, to avoid significant costs to society.

It’s really interesting topic and application of machine learning algorithms. However, I would be curious to discuss how introduction of self-driving cars would change the industry. If the level of casualties decrease dramatically with self-driving cars, then would AXA even have a business at all?

Also, assuming AXA eventually would have data on every insured person in a real time, how would this change the nature of their business? With such data access most likely their estimation of probability of accident with any person would be so precise that AXA practically would not insure risky persons, because would know almost fo sure if the person is going to have any accident at some point or not.