Spotify | Should Investors Join The Band?

As the Swedish music service prepares to list its shares on the NYSE in the next few months, investors wonder about the sustainability of its business model: will the world’s largest streaming company stand up to quarterly pressures and convince shareholders of their long-term plan?

Ten years after its inception, Spotify has much to show for its success. The streaming service has become the largest music platform in the world with over 140 million users, half of them subscribing to its premium offering. The company is present in over 60 countries.

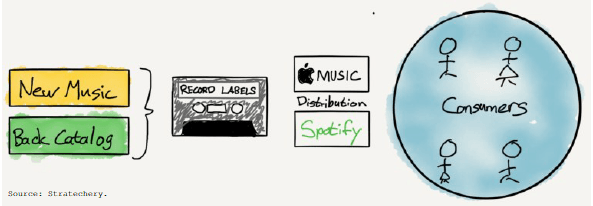

Spotify can be categorized as a three-sided platform, with record labels as the suppliers of most of the content, users who opt for different tiers of subscription, and advertisers. It operates as a freemium model, and although advertisement is a small source of revenues (approx. 10% [1]), it is a key component of its customer acquisition strategy. Network effects are low, although social features such as Collaborative Playlists and Friend Activity are purposefully increasing them.

The Swedish firm creates huge amounts of value for the two main sides of the platform. Users get immediate access to 30+ million songs for free (plus ads), or for a small fee of $9.99/month. Interestingly, the value for the user grows proportionally with time for two reasons. First, as long as the user streams music, she is not buying albums, and thus, the value of her alternative to the service (e.g. her private collection) decreases. Second, Spotify is fiercely leveraging data from users to bridge its transition from a pure search-and-play platform to a discovery platform. As the user spends more time on the platform, the algorithm recommends music more attuned to the user via features such as Discover Weekly, Release Radar, or Your Daily Mix.

For labels, streaming services have substituted its traditional distribution arm and now account for their largest source of revenues (over 45% for Universal Music Group [2]), far outstripping physical purchases and digital downloads. Although the music industry complaint for years about the disruption created by both iTunes (2001) and Spotify (2008), experts credit these technologies with saving the industry from the piracy threat and with enabling healthy levels of growth in past years [3].

Record labels, which are both platforms and Spotify’s main suppliers, have avoided the fate of other traditional media industries, such as publishing [4]. Music, as opposed to news, doesn’t necessarily lose value with time. That enables labels to sit on top of huge back catalogs (with copyright of 70+ years) that provide them with a regular source of revenues, which in turn helps them sign on new artists. This explains why the industry has consolidated into the “Big Three” labels (Universal Music Group, Warner Music Group, and Sony Music Entertainment), accounting for over 80% of the industry.

For both sets of platforms, music is a commodity [4]. Both the Big Three’s and Spotify’s economic incentives are aligned to maximize average revenue per user and increase access to the service, i.e. getting as many people as possible to pay for streaming. Multi-homing makes economic sense for labels for that reason, which in turn prevents users from subscribing to more than one service since the offer is not differentiated enough (as opposed to film and TV platforms).

However close their fates align –and even if the Big Three own a sizable stake on Spotify and want to avoid going back to the old days of Apple’s monopsony–, labels are partially responsible for Spotify’s current unprofitability. Their agreements are pegged to consumption (i.e. revenue sharing) [5], and although new deals include “margin relief” clauses, scale alone won’t help Spotify grow margins at the pace investors might expect them to. On the competition side, pressures on pricing and offering keep heating up, with diversified players such as Apple and Amazon looking at music streaming as a loss-leader segment to enhance their broader product ecosystems [6].

As the Swedish platform gets ready to IPO, several growth strategies are on the table. Spotify can focus on expanding its geographic reach both organically (Apple Music is available in 50+ countries that Spotify is not [7]) or through partnerships (for example, the recent minority stake swap with Tencent [8]). They can also increase rates of conversion to premium via market segmentation and attractive bundles with other services, such as their Hulu bundle for students [9].

But ultimately, Spotify’s sustainability depends on them finding novel models to reduce their reliance on labels, either by entering new verticals (e.g. video, podcasts, news) or by signing their own artists and developing exclusive content to drive differentiation, which might prompt a reaction from the Big Three. So far Spotify has thrived by building a better user experience compared to Apple or Amazon, but their future (and independence) might depend on them evolving into a full entertainment platform or a record label itself.

Sources:

[1] https://www.billboard.com/articles/business/7833686/spotify-2016-losses-financial-results-revenue

[3] https://www.ft.com/content/a548d874-bd60-11e6-8b45-b8b81dd5d080

[5] https://www.ft.com/content/e90f1ef4-17f2-11e8-9376-4a6390addb44

[7] https://www.musicbusinessworldwide.com/apple-music-is-now-in-57-countries-that-spotify-isnt/

[8] https://press.spotify.com/es/2017/12/08/spotify-tencent/

[9] https://news.spotify.com/us/2017/09/07/spotify-and-hulu-streaming-bundle/

Great post, Juan, thanks! I had not thought of the possibility of Spotify needing to evolve into a record label of its own, but that makes total sense if it is to try to control the content. It will be interesting to see, after the IPO, if the Big Three do buy sizable shares in Spotify and if they do what sort of power they will be able to wield over the company and the future decisions that it will make. In some ways, by going public, Spotify is almost giving the possibility of power back to the studios as if the Big Three are willing to invest enough into the company they will have a substantial say into the future business model and workings of the organisation. I wonder if the risk of that is worth the reward of going public.

Thanks, Juan. Spotify has been very successful to date, but I personally don’t see it as a viable long-term player. I ultimately think they will get acquired as they face rising competition from Apple and Amazon who have virtually unlimited cash to invest to crush (or buy) Spotify. There’s not really multi-homing in this industry, but the switching costs are pretty low (just cancel your Spotify membership). The company will need to find a new way to differentiate, whether it’s through exclusive partnership with sought-after artists or DJs or through becoming a more full-fledged entertainment platform.

Very interesting read – I had never thought of a future where Spotify turns into a record label but it seems like a very logical direction to move. Perhaps they could start my focusing on unknown or lesser known artists to test the model and slowly move toward popular artists. Either way, I think you’re definitely right that they must make some type of big move in finding a novel model. We all saw how quickly users switched from Pandora to Spotify and they certainly don’t want the same fate.

Great point on Spotify being a “content discovery platform” instead of a pure-play music retail service via streaming. The recommendation algorithm behind the content discovery feature in turn benefits from the “learning effect” as covered in the Qihu case: as Spotify logs and analyzes a larger and larger sample of user preferences and listening patterns, its recommendation algorithm becomes better and better, forming a competitive moat against new entrants and potential complementor-turned-competitors in the digital content streaming industry.

Fascinating read – thank you!

Great post! A very interesting point to think about how the fact that music labels invested in Spotify may create conflicts of interest or hamper Spotify’s growth. I also agree that the answer for Spotify may be to create their own content or act as their own label. We saw this with the TV streaming platforms, who needed to find new ways to differentiate themselves through original content. If this is the case, do you think we will start to see more multi-homing with music platforms like we do with TV platforms today? And will consumers pay for multiple TV and music streaming apps?

Great post Juan! The push to become more of a discovery platform rather than a search and play tool seems like it could hold a lot of promise for Spotify — I would guess that they have the user base (and thus the data) to presumably build better algorithms than their direct competitors at this point (although that may change with Amazon’s Alexa and other smart speakers prioritizing their own streaming services). It would be interesting to explore whether Spotify could sell these algorithmic insights back to the labels to help them further optimize their music offering to what certain segments are demanding (at an even finer level than the traditional gross sales by song model e.g., Spotify knows when in a song players are hitting skip for instance). Scary to be up against Amazon and Apple in anything though!

Thanks for sharing. I agree with everything that you have laid out above. I believe that there are several pieces to the puzzle missing before Spotify can truly flourish. One additional issue worth mentioning is the company’s incredibly high user churn rate, which I believe is north of 50% annually. The company must continually refill its leaky funnel, which is costly and unsustainable. To fix this problem, Spotify must figure out a way to make its platform stickier. You could imagine a scenario where Spotify offers exclusive content, similar to Netflix, thereby making users more likely to stick around. This is just one idea for one problem the company faces. Lots to be seen with this company in the coming years.

Great one Juan. I wonder about the recent blurb from Spotify execs about the issue with delivering Spotify the platfrom through other players’ platforms. By adhering to other players’ rules, terms of use, apps ranking etc – Spotify losses margin and also risks brand control and effective control over value proposition to consumers.

Hi Juan – great article! I think that the long-term issues you lay out are very real, but I’m wondering if Spotify not also has some very urgent short-term challenges ahead. Specifically, I’m thinking that Spotify is being cornered as the only major music streaming service that doesn’t have it’s own HW: Amazon has been super successful with it’s Echo and Alexa built into third-party speakers like the Sonos One … and Apple just launched it’s HomePod.

If virtually all speakers become smart and those are owned – or voice controlled – by players that also provide smart speakers, Spotify seems to be in a pretty bad place.

Thanks Juan! When I interned at Spotify, the name of the game was content discovery – they believed if you were able to better predict and offer good suggestions to people who wanted new music, that would be enough to earn their loyalty. But without any user-side network effects keeping the relationship sticky, I find it hard to imagine that Spotify is going to be able to differentiate enough to keep their premium base. And although it does not have to be a winner-take-all market, as Zach mentions above they may face unsustainable pressure from bigger players with much deeper pockets.

Great post! I believe there is definitely a strong comparison to be made to Netflix as other comments have suggested. Sustaining an advantage based on licensed content will only last so long. Spotify will eventually need to develop original content – essentially becoming a record label. Spotify has heavily leveraged machine learning algorithms to build out their customized playlist features. Highly personalized playlists are a form of original content that I personally believe only Spotify currently does well. The data they have collected on user’s listening habits could enable them to make excellent picks should they choose to also develop original content.

Great post, Juan, thanks. This Spotify IPO is certainly interesting for many of the reasons you pointed out. I found this interesting: http://www.ifpi.org/downloads/GMR2017.pdf a music industry report. Music producers are still not happy with how the industry has evolved and are looking to work with Spotify and other streaming platforms to re-claim more value for itself. The evolution of Spotify’s business model and the future of this industry is very exciting.