Manulife: Transforming a Century Old Stalwart

The transformation of a 130-year old financial institution into a digital-centric organization.

How does a 130-year old financial institution transform into a digital-centric organization in the face of rapidly evolving competitive dynamics and customers preferences? It’s not easy, to say the least. But, Manulife is making a committed effort to do so.

In November 2016, I wrote my first blog post at HBS (link) about how Manulife, one of the world’s largest insurers and wealth managers, is adopting digital technologies to redefine its business. Here we are, a year and a half later, and I’m writing on the same company for my very last blog post at HBS, assessing how much further Manulife has come on its digital transformation journey.

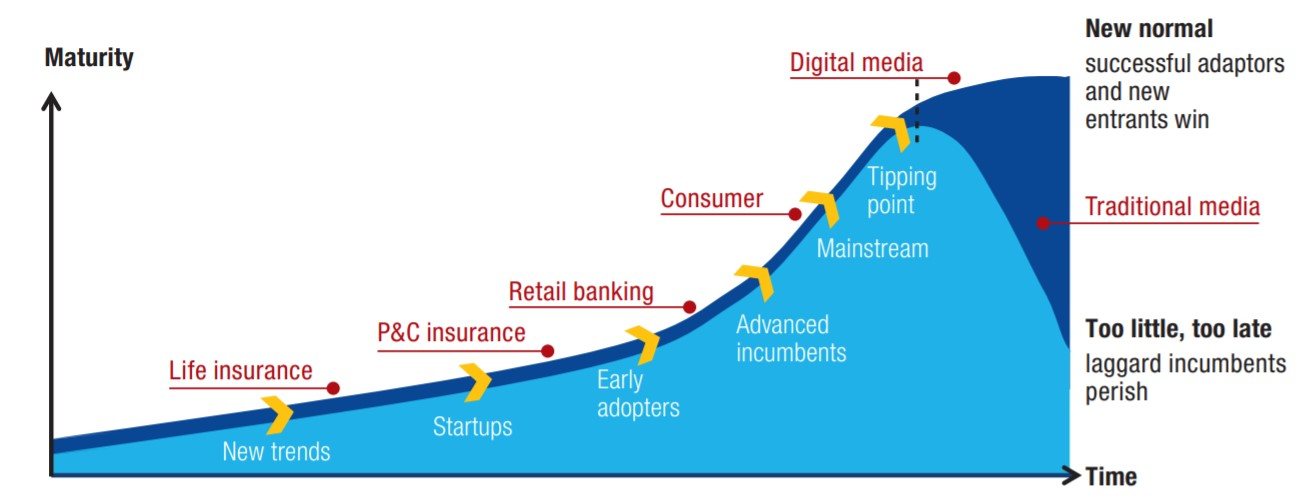

The pressures on the financial services industry and the urgency to transform are even more significant than they were back in 2016. The industry represents one of the largest in the world, yet it has continuously lagged its peers in its adoption of digital innovations (Figure 1). As a result, the industry is increasingly attracting the attention of digital disruptors seeking a piece of the pie, and Manulife is right in the middle of it. Canada’s largest company by revenue, Manulife embarked on its digital transformation years ago and has made significant investments to better position it for the future.

Figure 1: Life insurance lags other sectors in digital maturity

Source: McKinsey Insurance Multi-Access Benchmark

What changes has Manulife made on its digital transformation journey since 2016

- Leadership. In late 2017, a new CEO, Roy Gori, took the helm of Manulife. As he was beginning his tenure Gori stated, “we need to think of ourselves much more like a technology company. Technology has got to be the way that every single person at the company thinks and operates. Our industry has not evolved at all and has not embraced that transformation.” To truly become a culture that embraces technology, the tone must be set from the top, and it seems that Gori has the intention and desire to do that. [1] While Gori’s reign hasn’t been long enough to assess his success, his appointment was certainly an important organizational change and is indicative of Manulife’s dedication to its digital transformation.

- Capabilities. In the last couple of years, Manulife has launched a global Advanced Analytics group. The Advanced Analytics group is composed of data scientists, data engineers, and strategists in Manulife’s markets around the world and focuses on digital analytics measurement and reporting (e.g., marketing initiatives), talent analytics, underwriting, and fraud detection. The group launched an advanced analytics development program for new data scientist graduates the enables participants to get exposure to different analytics opportunities as well as different aspects of Manulife’s business. [2] Manulife has also engaged in several strategic partnerships to strengthen its digital capabilities, including with Nervana Systems, a Californian technology company to develop an AI-based tool to help portfolio managers in their decision-making. [3]

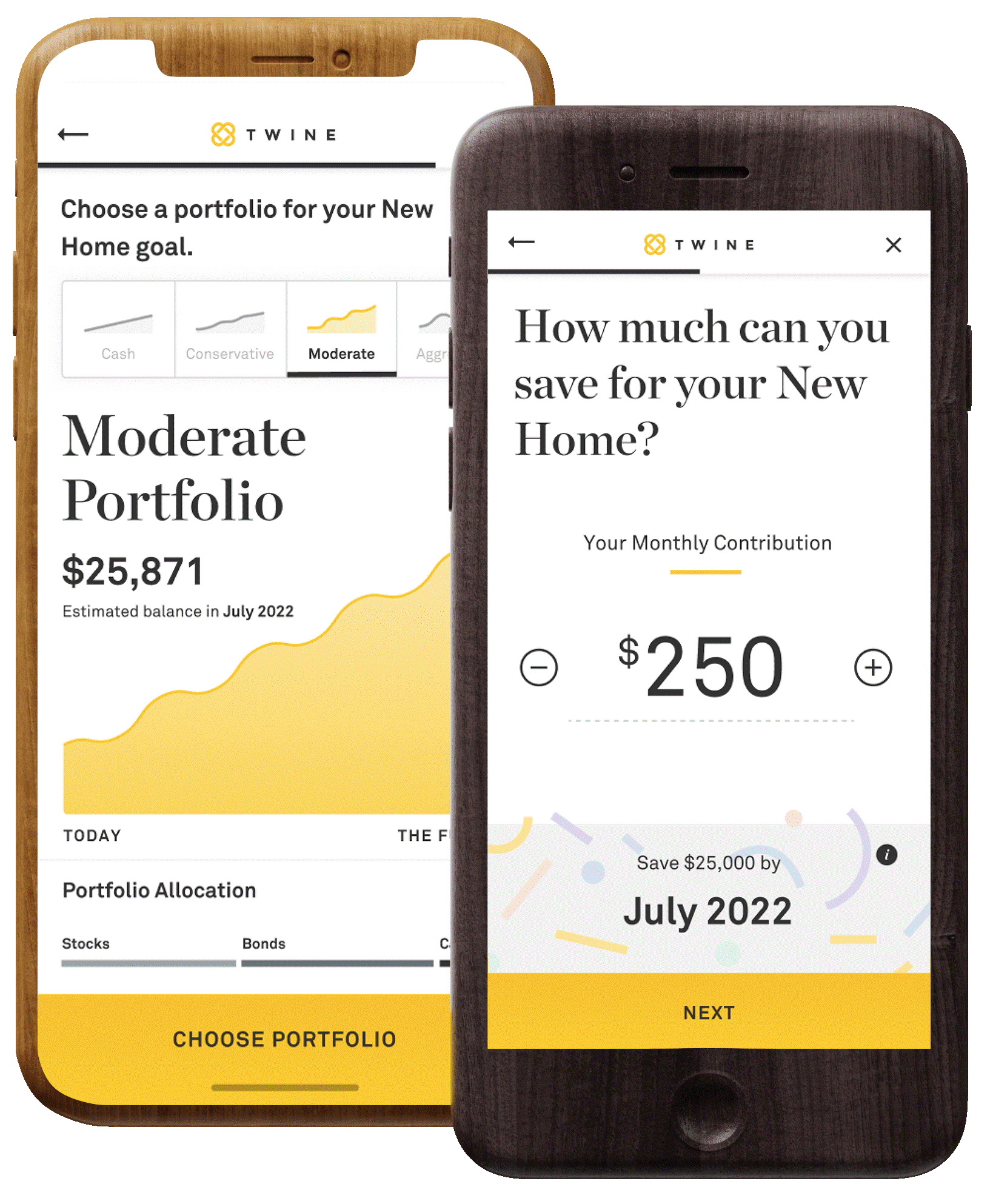

- Products and services. Manulife has launched a number of new digital products to differentiate itself with its customers. For example, Twine is a robo-advisor and personal finance mobile application launched by Manulife in late 2017 (Figure 2). The app has a simple, clean user interface and is targeted to millennial customers, a segment that has been typically more challenging to access for traditional wealth managers and insurers. Twine operates as separate organizational unit in San Francisco, across the country from Manulife’s U.S. headquarters in Boston (John Hancock). While Twine operates with autonomy from the parent company, it also leverages Manulife’s abundant resources. [4]

Figure 2: Twine Mobile Application

Source: Twine Website

What challenges and opportunities lie ahead and how should Manulife address them

- Sourcing key tech talent. This is will continue to be a challenge for Manulife, just as it is for most large incumbents across various industries. Manulife is competing for digital talent with the likes of Google and Amazon, which offer attractive compensation packages and the allure of exciting projects. Therefore, Manulife must be creative in understanding and providing what matters most to prospective talent. For example, Manulife can launch separate companies under separate brand names that operate in a startup-like environment, unencumbered by the parent company’s more bureaucratic operations. It has already successfully done this already with Twine. Ensuring that talent is working on meaningful, visible, and leading-edge projects is also critical both for acquisition and for retention. Manulife also has the benefit of being in markets around the world. It may be easier for the firm to attract certain talent in particular markets and should take advantage of these opportunities.

- Taking full advantage of artificial intelligence. Data is at the heart of insurance, and as a result the industry offers seemingly unlimited opportunities for artificial intelligence and machine learning, from predictive underwriting to advice and customer service. Imagine a world where insurers can rapidly analyze data about how you live your life captured through your mobile device (e.g., how active you are, how many hours of sleep you are likely getting each night) to immediately create custom and dynamic products that are best for you. Of course, this future would open the door to many questions regarding data security and privacy. But without a doubt there is tremendous opportunity for AI and data analytics to create a much more efficient, customer-centric insurance experience. [5] Toronto, where Manulife’s global headquarters is located, also happens to be one of the world’s AI epicentres. Manulife can look to partner with or acquire some of the AI firms in the city to build both its credibility in the eyes of future talent and its capabilities. In return, the AI companies could get access to copious data and opportunities to solve some of the most significant challenges that AI can address.

- Partnering with or acquiring small companies that specialize in desired capabilities. Manulife has made several partnerships, acquisitions, and investments in various technology companies, but there is opportunity for the company to do even more. Deals such as these could serve as an effective way to build capabilities that are otherwise difficult to build in-house and to leverage these autonomous, more entrepreneurial organizations to acquire key talent.

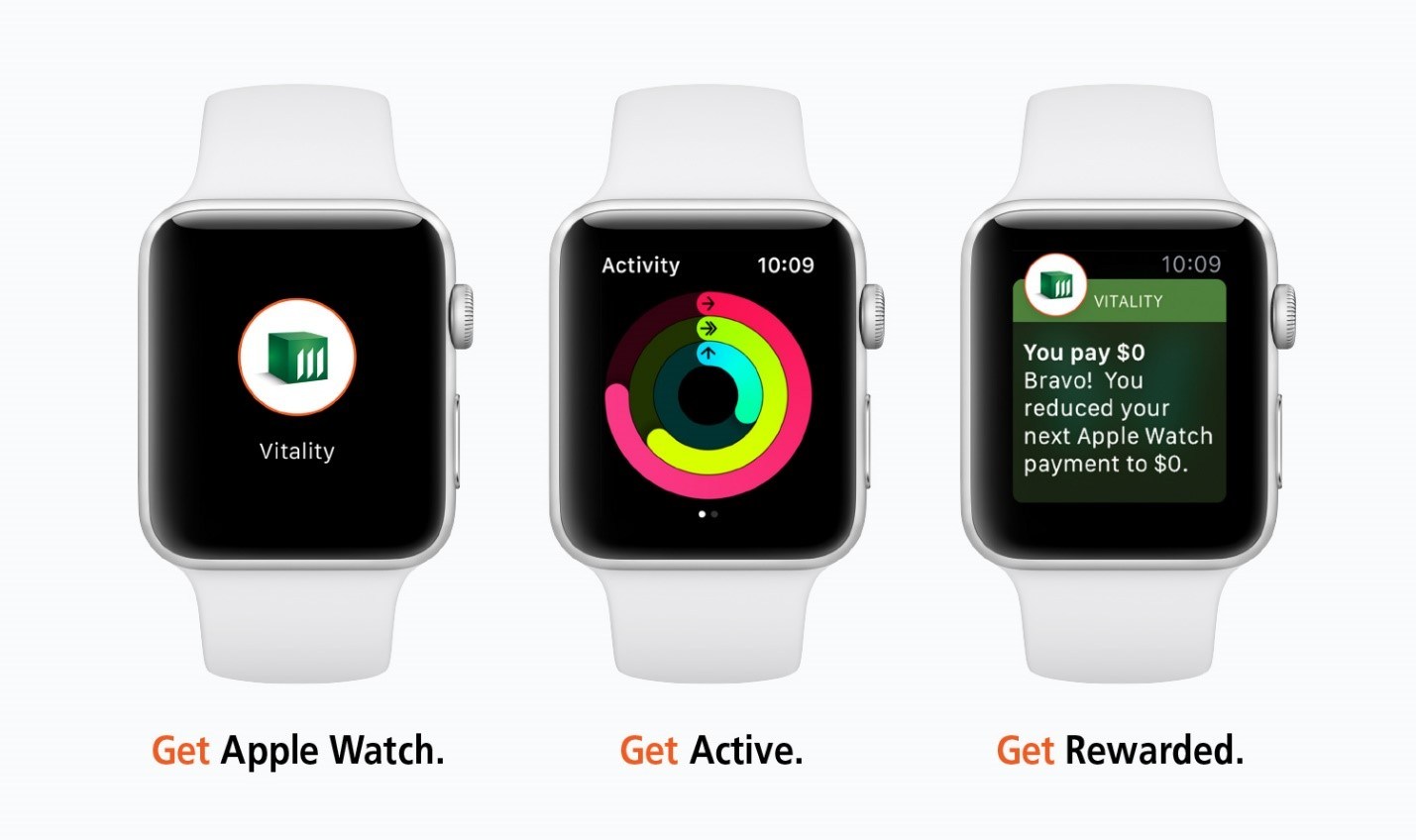

- Invest in technologies of the future. Internet of Things (IoT) and Blockchain will offer many opportunities to create a more differentiated experience for customers. Manulife has already begun investing in IoT, especially through its wellness-based initiatives and products (e.g., Vitality program in Figure 3), which leverages wearable devices. [6] Manulife’s innovation group, the Lab of Forward Thinking (LOFT), is also exploring potential use cases for blockchain and is collaborating with ConsenSys and BlockApps, two blockchain-based tech start-ups. [7] Despite challenges that will surely arise with regulation, Manulife must continue to explore how technologies like IoT and blockchain can help the company provide a better customer experience.

Figure 3: Manulife Vitality enables the company to collect more data and offer a more tailored experience for customers leveraging wearable devices

Source: Manulife Website

Manulife faces an uncertain future but has been deliberate and determined in its digital transformation efforts. The firm must increase the pace and urgency with which its making this change. It will be fascinating to watch how Gori and the culture he is creating around digital technology will fare in the years to come.

Sources

[1] Jacqueline Nelson, “Manulife’s New CEO Roy Gori Sets Sights on Shaking up the Insurance Industry,” The Globe and Mail, https://www.theglobeandmail.com/report-on-business/manulifes-new-ceo-roy-gori-sets-sights-on-shaking-up-insurance-industry/article36442248/, accessed April 2018.

[2] Manulife Advanced Analytics, http://www.manulife.com/AdvancedAnalytics, accessed April 2018.

[3] Tessie Sanci, “Manulife to Develop AI Tool Thanks to New Partnership,” Investment Executive, https://www.investmentexecutive.com/news/industry-news/manulife-to-develop-ai-tool-thanks-to-new-partnership/, accessed April 2018.

[4] Suman Bhattacharyya, “How Twine, John Hancock’s Robo-Adviser Tool, Keeps a Startup Feel,” Tearsheet, http://www.tearsheet.co/culture-and-talent/how-twine-john-hancocks-robo-advisor-tool-keeps-a-startup-feel, accessed April 2018.

[5] Bob Crompton, “Artificial Intelligence and Its Effects on Life Insurance Companies,” Society of Actuaries, https://www.soa.org/Library/Newsletters/Predictive-Analytics-and-Futurism/2017/december/2017-predictive-analytics-newsletter-issue-16-crompton.aspx, accessed April 2018.

[6] Julianne Callaway, “The Internet of Things: Key Considerations for Life Insurers,” Reinsurance Group of America, https://www.rgare.com/knowledge-center/media/articles/the-internet-of-things-key-considerations-for-life-insurers, accessed April 2018.

[7] Barbara Shecter, “Manulife to Use Blockchain Technology at U.S. Wealth Management Division,” Financial Post, http://business.financialpost.com/news/fp-street/0421-biz-blockchain, accessed April 2018.