Ethereum: fueling the hype around blockchain?

Will Ethereum be the platform that successfully brings blockchain into the mainstream?

Ethereum is an open-source blockchain platform that was introduced in a 2013 white paper by Vitalik Buterin, a Bitcoin programmer who wanted to expand the applications of cryptocurrency. Ethereum’s blockchain went live in July 2015 and seeks to use smart contracts to facilitate transactions on its platform.

Sooo what do all these buzzwords mean?

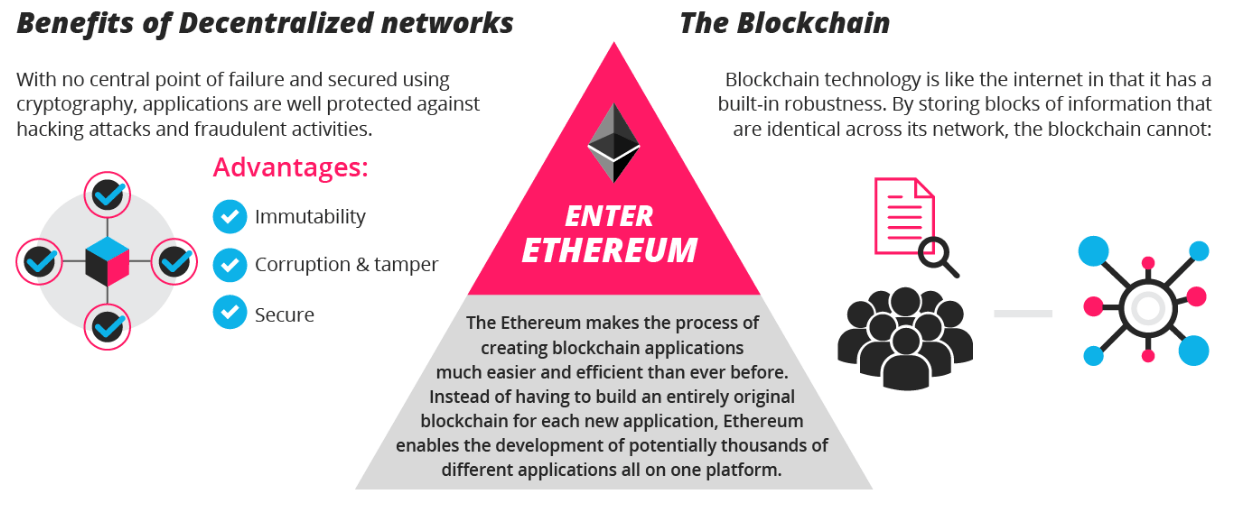

First and foremost, let’s explain what exactly blockchain is. Blockchain is a revolutionary technology that uses a decentralized database to maintain a linear, chronological record of events or transactions. As an open, distributed ledger, there is no single point of failure (making it less vulnerable to cyberattacks) and democratizes ownership records (all transactions are viewable by everyone so it’s very difficult to manipulate records) but it can maintain anonymity of users.

As Don Tapscott, author of Blockchain Revolution, describes it, “blockchain…is the biggest innovation in computer science—the idea of a distributed database where trust is established through mass collaboration and clever code rather than through a powerful institution that does the authentication and the settlement.”

You’ve probably heard of Bitcoin as the most popular current use of blockchain. Ethereum expands upon the digital currency application of blockchain to create an open software that allows developers to build decentralized applications on top of the platform.

To use SAT parlance, Bitcoin : Email :: Ethereum : Internet.

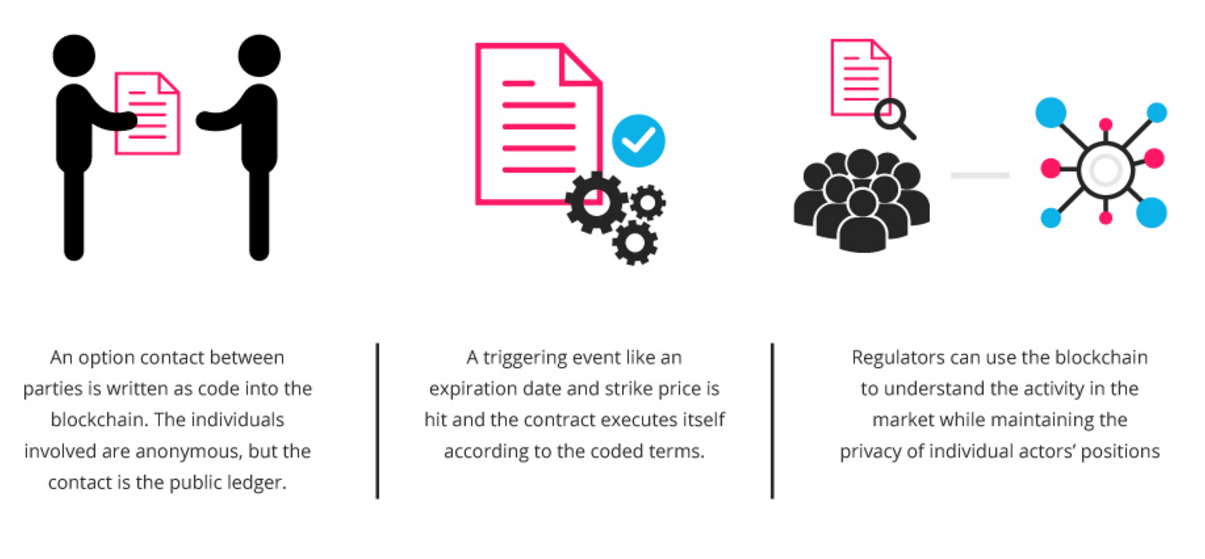

Ethereum uses smart contracts to facilitate the exchange of value – whether it’s in the form of money (on the Ethereum platform, the digital currency is called Ether), content, property or shares of ownership – on its platform. Because Ethereum’s smart contracts run on blockchain technology, the applications can run without fear of downtime, fraud, third party interference, tampering of data or censorship by a centralized authority.

That sounds great, but what are the real use cases?

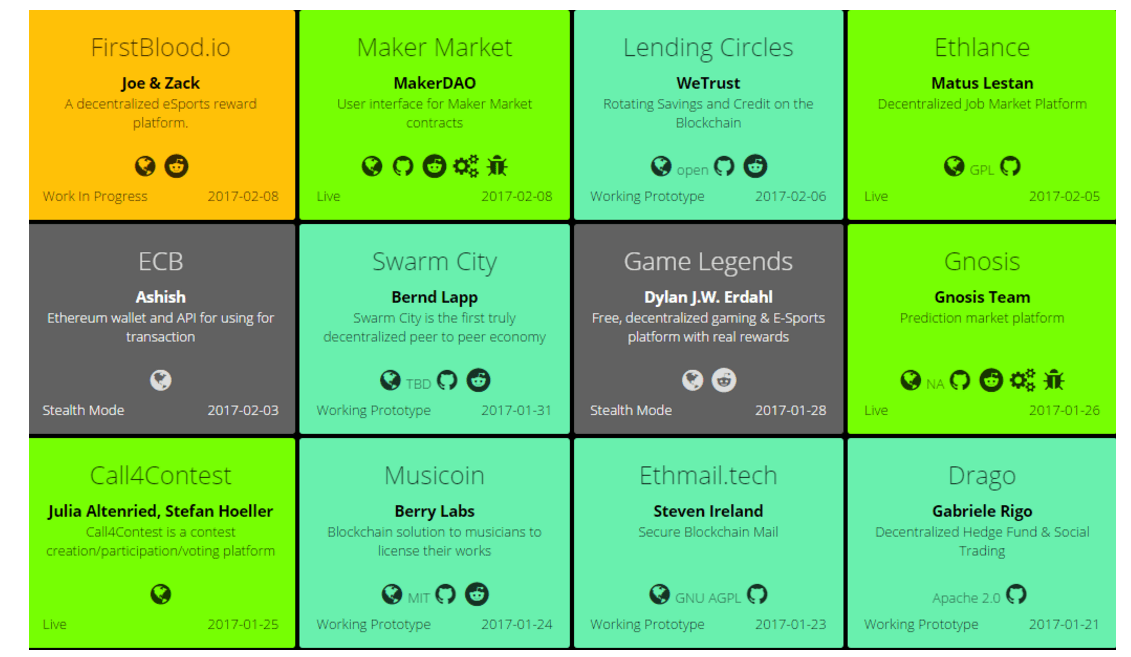

Basically, any service that is currently centralized can be decentralized using Ethereum. Consider all the industries currently controlled by intermediaries: banking, payments, insurance, and real estate are obvious ones, but blockchain can even be used for voting systems, IoT applications, music sharing, forecasting and supply chain management. Current applications on Ethereum include:

- Uport allows users to control who can access their data and personal information

- BlockApps provides tools to create private and public industry-specific blockchain applications

- Weifund provides an open crowdsourcing platform that enables contributions to be turned into digital assets

- Augur is an open-source prediction and forecasting market platform

- Provenance makes supply chains more transparent for consumers by tracing what raw materials go into products

See right for more Ethereum apps.

Many heavy-hitters across various industries have started using Ethereum in their blockchain applications. Microsoft’s Azure, a recently-launched blockchain-as-a-service platform, uses many distributed ledgers in its service offerings, including Ethereum. In fact, in January 2016, eleven banks including Barclays, UBS and HSBC used the Ethereum protocol through Azure to test out a bank-to-bank platform; this simulation allowed banks to settle transactions to each other almost instantaneously, as opposed to several days or weeks (depending in the asset class) required under current systems. Proponents claim that blockchain will be commercially used by banks to transfer real assets in the next couple years.

How will Ethereum scale?

To date, Ethereum’s success is largely propped up by early evangelists on both the developer and user side (with likely considerable overlap of individuals utilizing both sides of the platform). While exact numbers are difficult to obtain, as of March 2016, the market capitalization of Ether – the digital currency on Ethereum – was over $1 billion and there were ~6,000 nodes on the network (a rough proxy for the number of developers).

While trust and understanding of blockchain remain the biggest barrier to mainstream adoption, in order to become THE platform of choice for blockchain, Ethereum will have to capitalize on network effects. Some key considerations in assessing its network potential:

- Global adoption will be key. By the very nature of its decentralized protocol, Ethereum’s payment and transaction systems are not subject to region-specific regulatory or compliance barriers like most payment systems, thus allowing for mass usage globally. Ethereum should leverage this to reach a critical mass of adopters faster.

- While there are competing blockchain platforms in existence, Ethereum is the largest and most reputable as of now. However, switching costs are low and multihoming is likely high among blockchain evangelists (both on the developer and user side) given blockchain’s nascency and the continued evolution of the technology; developers and users want to test out different protocols on different platforms to see what best suits their use cases.

- This is an industry where first mover advantage REALLY matters.

- TRUST, TRUST, TRUST. By becoming the biggest name in blockchain platform technology today, Ethereum already has an advantage over competitors in being the most trusted platform. Trust is everything in driving adoption of blockchain – users need to believe that their money, assets and data will be secure.

- The open source nature of the platform serves Ethereum well. Ethereum can constantly update its protocol based on the newest blockchain thinking in the market, allowing for flexibility in the changing tides of the blockchain market.

- Market liquidity is important. In dealing with payments and transaction, market liquidity is key in spinning the flywheel to get demand and supply onto the platform. If Ethereum can build critical mass in market liquidity first, it’s more likely to remain a dominant player in blockchain transactions. Success begets more success.

Challenges Ahead

Despite the incredible potential of Ethereum’s platform, the road ahead is fraught with uncertainty. What is the business model? Will developers monetize in the same way they do with app stores (e.g., by downloads or subscription)? Perhaps developers will not want to earn money by Ether when the cryptocurrency value is so uncertain. How will the business model evolve to incentivize the above network effects? On the user side: how does Ethereum reach post-chasm users? Does it need a killer app to do so, and if yes, what will it be? What are the biggest barriers to mainstream adoption? Is it cybersecurity concerns? How will Ethereum compete with Visa and Mastercard in terms of liability and insurance capabilities?

How will the overall ecosystem develop – will traditional financial institutions become competitors or complementors? Will banks strongarm Ethereum into becoming a single-use payment transfer system? Will private blockchains deter the growth of an open platform like Ethereum? These questions just begin to scratch the surface of the unsettled issues around Ethereum.

With 100x step-change technologies like blockchain, it’s difficult to parse out hype vs reality. While blockchain’s potential is undoubtedly massive, it remains to be seen whether it can cross the chasm past its early evangelists, particularly as it seeks to transform deeply entrenched, slow-moving industries like insurance and banking.

References:

http://blockgeeks.com/guides/what-is-ethereum/

https://medium.com/@AroundTheBlock_/a-current-list-of-use-cases-for-ethereum-b8caa5807553#.xrfthr6q3

https://cointelegraph.com/news/why-ethereum-urgently-needs-next-gen-apps-to-succeed

https://www.cbinsights.com/blog/industries-disrupted-blockchain/

https://www.cryptocoinsnews.com/ethereum-rise-growth-new-york-times/

http://bitcoinist.com/six-ethereum-projects-and-its-five-competitors/

https://www.ethnews.com/the-banking-industry-is-embracing-the-ethereum-blockchain

http://uk.reuters.com/article/uk-banking-trading-blockchain-idUKKCN0UY28W

http://www.mckinsey.com/industries/high-tech/our-insights/how-blockchains-could-change-the-world

Yezi, great post. Bitcoin is one of the most exciting technologies evolving right now, but so many people remain oblivious as to what it is! I get the sense that this could be a winner-take-all market, if Ethereum can figure out how to reduce multi-homing or gain mass adoption on the user side. Does that intuition make sense to you? Also, do you think the recent news about the successful SHA1 hash collision change the game for bitcoin more broadly? If so, can Ethereum differentiate itself in any way when it comes to security versus other blockchain reliant technologies?

I definitely agree that this feels like a winner-take-all market. User adoption will be really key – while I personally believe blockchain is an inevitable technology that will disrupt a lot of industries, I wonder if Ethereum is too early. We may have a few years ahead of us before blockchain hits the mainstream; can Ethereum maintain momentum through that time, or will another company come in at a more opportune time and win the race for users?

Cybersecurity will absolutely be the most crucial issue. Cryptographers have been warning that SHA1 may not be totally secure for a while, and luckily Ethereum runs on a different, more secure hash function. But it will certainly have to stay on its toes to be at the forefront of blockchain security in order to be the trusted platform of choice.

Extremely well written Yezi! One of the finest posts I have read in a long time which explains the technologies around blockchain and their application in the finance world so lucidly.

Since this is a technology where reliability is a major factor, do you think adopting the newest trend is right for ethereum always as it looks to scale always? Won’t it make sense to ensure that someone else tests a new technology since a lot is riding on ensuring reliable service?

The second question I have (and this maybe due to the fact that I have very basic level of understanding of this field) but do you see a future where Visa and MasterCard to develop a blockchain platform of their own?

Sidharth–a timely question! I was wondering the same thing, and have been reading about this company R3 that is doing just such test. I’ve dropped a link below about a recent one. The firm’s approach is to put together a consortium of banks, get them to agree to allow R3 to run tests where they move their ledgers from traditional systems to blockchain systems (in this case, using Ethereum!) and see how it goes. From a technological perspective, this seems to be a wonderful development: business practitioners are hearing the calls of technologists, and taking advantage of innovation for practical and creative applications. I wonder if it should worry us, however, that firms like R3 could stand to capture all the value from implementation of these types of innovations. If, for example, R3 can save Morgan Stanely $10M per year, surely R3 can claim $1M (just making up numbers). Ethereum will capture none.

http://blogs.wsj.com/cio/2016/01/20/major-banks-complete-modest-blockchain-test/

see below

http://www.coindesk.com/visa-blockchain-payments-service/

Thanks, Sidharth! I agree that Ethereum will have to be very smart and intentional about which new algorithms and functions it decides to deploy in its protocol – cybersecurity will be of utmost importance. Your second question is a really good one – Visa is actually already exploring using blockchain for payments. I think private blockchains will become prevalent in the financial sector, and it will certainly be interesting to see what types of transactions go the way of private vs open blockchain. A lot of it will be up to the users – some will feel more secure using the more familiar route with their dedicated banking institution on that bank’s private blockchain; others may eschew traditional banking altogether and go with open blockchain transfers. I think it will be a slow adoption curve with the majority going with the former approach in early years.

James – you’re totally right, and I think that’s where the delineation between private and public blockchains will come in (as mentioned above). It will definitely be interesting to see if open blockchains become the medium of choice (as that’d benefit Ethereum), or if these industries decide to go with more incremental change and go with private blockchains which are a more intermediate use of blockchain (in that they are not fully decentralized systems). I think the latter is frankly very likely for mass usage products, which is concerning for an open platform like Ethereum.

One of the best posts I read today! I’ve been fascinated by blockchain and glad this company exists to help populate more applications of blockchain technology. My intuition for the business model is a Platform-as-a-service model, ‘hosting’ whichever application on its blockchain technology platform. This way as long as the applications exist and the company does its job of supporting it, it earns revenue. Pricing could be tiered based on the ‘volume’ of records being created on the ledger. I see a mid-market play here as the big institutions such as JPMorgan, etc. are already very aggressive in developing their own and has the capital to do so.

Thanks Yezi! I agree with you that trust and reliability are key in this market, but therefore I feel a first-mover advantage may not be as relevant in this case. Firstly, it is because the first mover is most susceptible to the “teething problems” of an emerging technology and its reputation will likely take a brunt for all of these. More importantly however, I feel that if an established name like Google chose to build a similar platform in the near future, the trust associated with its brand equity would quickly draw users and developers to their platform instead. Do you know if a large player like Google is planning to enter this space at all?

Great post Yezi. I am myself a blockchain enthusiast and have enjoyed reading your blog post 🙂 !

I think Blockchain is enabling a shift from a centralized internet (where we have to rely on super-sized middle-men like Facebook, Google, Uber, etc) to a more decentralized internet in which value is better shared and privacy more protected. I wonder however what would you think the catalyst for this paradigm shift would be, in particular from the user perspective. Let’s take for example OpenBazaar – which is a decentralized ebay-like App (See Erik’s post here https://d3.harvard.edu/platform-digit/submission/openbazaar-using-the-power-of-blockchain-crowds-to-disintermediate-amazon/). What do you think would make a user switch from centralized eBay to a decentralized OpenBazaar? Is the incremental privacy worth the risk of switching to a completely new platform? If not, what could be other ways or business models that would allow for this switch to happen?

As I mentioned on my post on Erik’s post, I also invite you to check out the concept of AppCoins that is also emerging. AppCoins are crypto-currencies that are issued by Blockchain-based protocols in order to capture the value created by the protocol. They can be used to (a) Raise money through Initial Coin Offerings (a concept that could disrupt the entire VC industry) (b) Distribute value across the stakeholders – for example the network participants who are escrows on OpenBazaar could be rewarded by getting OpenBazaar AppCoins in exchange for their services and (c) AppCoins can be used to reward the company itself (The company can issue and keep a bunch of AppCoin, that it can sell on the secondary market onces the AppCoin appreciates). This concept is obviously still very nascent and faces many challenges in particular in terms of regulation (Are AppCoins securities in the SEC sense?).