The Digitization of Microfinance: bKash in Bangladesh

Nearly half of the World's population lives on less than $2 a day with limited or no access to formal financial services. Microfinance is crucial to getting credit into the hands of those most in need. How are microfinance providers using digital technology to help lift families out of poverty?

The Business of Microfinance

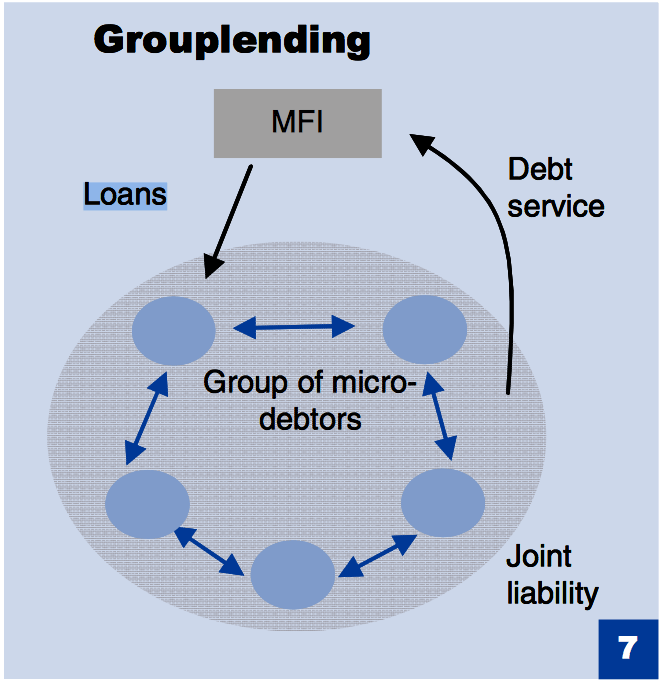

Microfinance serves the World’s under-banked population by providing financial services tailored to the needs of their financially constrained customer base. Microcredit is the primary service provided by Microfinance Institutions (“MFIs”) and it is generally dependent on a group lending model which encourages repayment through joint liability, rather than through use of collateral.

[Source:Raimar Dieckmann, “Microfinance: An emerging investment opportunity.” Deutsche Bank Research, December 19, 2007, http://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000219174.pdf, accessed November 2016.

Traditionally, NGOs have made up the bulk of MFIs, however in recent years more and more for-profit social enterprises have entered the sector.

Microfinance in Bangladesh and BRAC Bank

Bangladesh is often considered the birthplace of modern microfinance. Bangladesh has an enormous market for microfinance services as more than 80% of its 165 million people live on less than two dollars a day and 85% of the population lacks access to formal banking services.1,2 This demand for microfinance is being met by 685 licensed MFIs, more than almost any other country.3 With such a large market and many players, competition in the sector is tough. BRAC Bank is one of the oldest MFIs in Bangladesh and a predominant player in the sector. BRAC was founded in 1972 and is now one of the worlds largest NGOs, operating across 14 countries.4 The intense competition in the market encourages innovation and in November 2011, BRAC Bank founded bKash to focus exclusively on digitizing microfinancial services.5 bKash is at the frontier of digital microfinance, providing 98% of the country’s mobile phone users with financial services.6 Both the IFC and Bill & Melinda Gates Foundation have taken equity stakes in the Company.7

Digitization of Microfinance Services

The digitization of microfinance offers enormous benefits to both the provider and the customer. Generally, MFIs have high transportation costs due to poor infrastructure and a high percentage of customers living in rural areas. The digitization of services allows for transport cost savings, reduced staffing needs and cash risk, increased access to information and the opportunity to scale more rapidly. Digitization also benefits the customer: increased information, increased ease of use, and reduced risk. In fact, a recent study found that the digitization of microfinance could reduce travel and wait time for customers by as much as 75%, translating into savings which could feed a family of five for a day.8

bKash and Digital Microfinance

Source: Gregory Chen and Stephen Rasmussen, “bKash Bangladesh:A Fast Start for Mobile Financial Services,” CGAP Working Paper, 2014, http://www.cgap.org/publications/bkash-bangladesh-fast-start-mobile-financial-services, accessed November 2016.

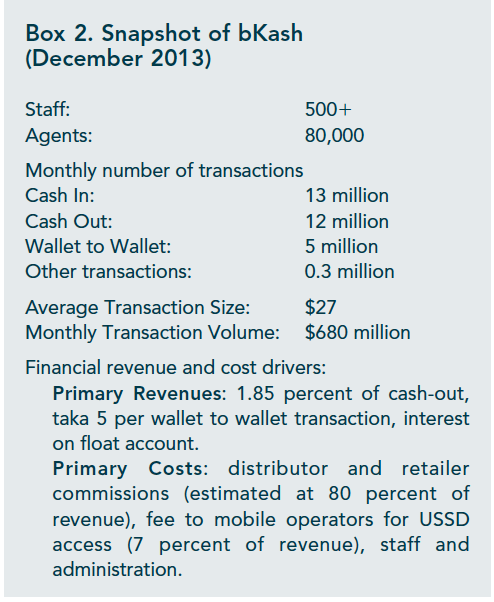

bKash is at the frontier of the digitization of microfinance, conducting more than 80% of mobile financial services in Bangladesh.9 In fact, “the term bKash has become so commonplace that it is synonymous to mobile money payments.”10 bKash offers money transfer and lending services which can be accessed on even the cheapest mobile phone.11 Customers can receive salaries, remittances, or credit through a pin on their mobile device (“cash in”) and then can “cash out” by visiting one of bKash’s 100,000 agents or one of BRACs 300 ATMs.12,13 Signing up for bKash and “cashing in” are both free, but there is a flat fee of 6 cents for person-to-person money transfers and a 1.85% fee on funds withdrawn.14

bKash & Digitization Moving Forward

bKash has made great strides in increasing the digitization of financial services in Bangladesh, but there is still an enormous potential for growth. Only 22% of Bangladesh adults are currently using mobile money.15 Furthermore, bKash can provide other services such as micro insurance and business-to-business transactions. Another option for bKash is to introduce a structured savings programs. A study in Africa found that regular reminders to save sent through mobile financial service providers increased customer savings by 16%.16

However, to be successful there are several risks that bKash needs to manage. First, the group-lending model of microfinance has been crucial to its success. Mobile microcredit eliminates the group function: how will bKash maintain high incentives to repay without collateral or group pressure? Second, bKash should strive to move away from the agent model. Not only is this an additional cost to the system which will eventually be borne by the consumer, but it also adds an element of risk as the agent must carry large amounts of cash and the system is heavily dependent on the trustworthiness of these agents. Third, bKash must be extremely clear about the fees it is charging. It is a pervasive misconception among users that digital financial services are free.17 Kenya recently enacted a law requiring all digital financial service providers to put transaction costs on the same screen as the transaction to ensure users have full information.18 While this is not currently required in Bangladesh, it is important bKash adopt this level of transparency to ensure the continued trust of its customer base. [757]

Works Cited

- Raimar Dieckmann, “Microfinance: An emerging investment opportunity.” Deutsche Bank Research, December 19, 2007, http://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000219174.pdf, accessed November 2016.

- bKash Limited, “Company Profile,” https://www.bkash.com/about/company-profile, accessed November 2016.

- “List of licensed MFIs as of Oct 30, 2016,” Microcredit Regulatory Authority, http://www.mra.gov.bd/index.php?option=com_content&view=article&id=115&Itemid=95, accessed November 2016.

- Gregory Chen and Stuart Rutherford, “A Microcredit Crisis Averted: The Case of Bangladesh,” CGAP Working Paper No.87, July 2013, https://www.cgap.org/sites/default/files/Focus-Note-A-Microcredit-Crisis-Averted-July-2013.pdf, accessed November 2016.

- Gregory Chen and Stephen Rasmussen, “bKash Bangladesh:A Fast Start for Mobile Financial Services,” CGAP Working Paper, 2014, http://www.cgap.org/publications/bkash-bangladesh-fast-start-mobile-financial-services, accessed November 2016.

- Kamal Quadir, “The Story of Bkash,” The Daily Star, April 23, 2014, http://www.thedailystar.net/the-story-of-bkash-21235, accessed November 2016.

- Chen and Rasmussen, “bKash Bangladesh:A Fast Start for Mobile Financial Services.”

- Leora Klapper and Dorothe Singer, “The Opportunities of Digitizing Payments,” World Bank Development Research Group Report No. 9035, August 28, 2014, http://siteresources.worldbank.org/EXTGLOBALFIN/Resources/8519638-1332259343991/G20_Report_Final_Digital_payments.pdf, accessed November 2016.

- Chen and Rasmussen, “bKash Bangladesh:A Fast Start for Mobile Financial Services.”

- Ibid.

- Quadir, “The Story of Bkash.”

- Ibid.

- bKash Limited, “Company Profile.”

- Quadir, “The Story of Bkash.”

- Chen and Rasmussen, “bKash Bangladesh:A Fast Start for Mobile Financial Services.”

- Klapper and Singer, “The Opportunities of Digitizing Payments.”

- Rafe Mazer, “Kenya Ends Hidden Costs for Digital Financial Services,” CGAP Blog, 2016, https://www.cgap.org/blog/kenya-ends-hidden-costs-digital-financial-services, accessed November 2016.

- Ibid.

This is a fascinating post and certainly eye-opening to learn that 80% of a country’s population lives on under $2 per day and does not have access to banking services. Certainly the advent of mobile phones has allowed companies to deliver services in a new, innovative way that has significantly less friction than before. bKash is no different in taking advantage of this technological revolution and is a great example of innovation benefiting those that arguably need it the most.

You ask pertinent questions at the end that I was asking myself as I read your post. Specifically, how will digital communication affect the group model and its willingness to accept group liability? Technology will likely make these groups less reliable on each other and thus erode their willingness to share financial responsibilities. Will bKash and others be in a position to pivot when this happens?

I agree with the post above. There is an inherent risk that the use of technology (and thus limitations to face to face contact) will have a negative impact on willingness to share financial responsibilities. Especially in the micro loan segment this may become an issue if default rates increase. The systems relies to a large degree on trust established through personal interaction. So this will be an interesting development to follow.

Hi Mkful! Thanks for the super insightful post. I hadn’t considered how digitization might impact traditionally face-to-face transactions like microfinance. One basic question: Does Bangladesh have the mobile phone/data/internet infrastructure to service digitized microfinance? I saw that mobile phone subscriber penetration was ~40% as of 2013 (https://www.gsmaintelligence.com/research/?file=140820-bangladesh.pdf&download). Are the traditional customers of microfinance lending programs part of that 40%, or do they not have phones? Does bKash do something similar to ITC eChoupal or Uber by equipping either a centralized user or all users with a computer/phone? I could also be misinformed on who bKash’s target market is – when I think of microfinance, I think of farmers and rural populations, but it sounds like they cater to urban consumers, too. Thanks again for the insight.

Awesome post – happy to see that there are so many opportunities to enables unbaked populations to have access to capital. One question that I have though is regarding the legitimacy / legal authorization that bKash has. Indeed, Bkash does not have any license under the banking company act – do you think it can provide banking services? Isn’t there a long-term risk likely to jeopardize its customers?