Talk to Chuck — Your New Robot Overlord

Charles Schwab is a big company. Their market cap currently stands at approximately 50 billion dollars [1]. Even so, Schwab has a remarkable history of reinventing itself as the needs of its customers evolve. Forty years ago, it created one of the first discount brokerage services, and in 1996, it developed an online trading platform to allow anyone to buy and sell stocks on the cheap [2].

The latest challenge for Schwab comes in the form of automated investment services, sometimes referred to as “robo-advisers” to differentiate them from more traditional, human-driven asset management firms. Robo-advisers purport to match or exceed the returns generated by either self-managed portfolios or those devised by expensive financial advisory services, while substantially reducing costs. The United States employs about 300,000 financial advisers. Newcomers like Betterment and Wealthfront are looking to replace human advisers with algorithms written by smart software engineers [3].

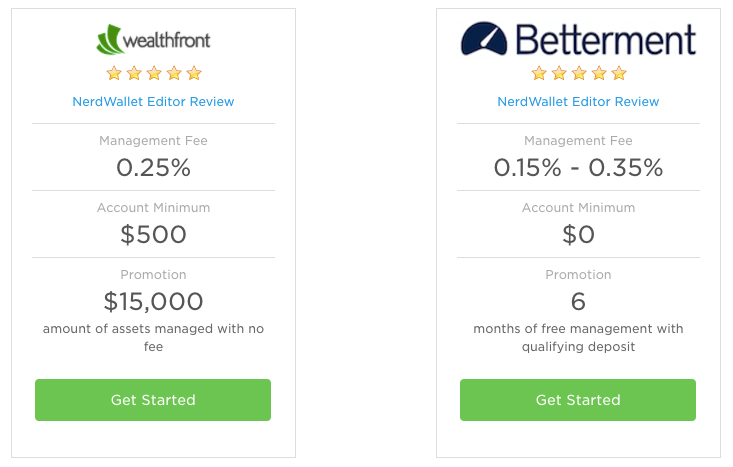

Betterment launched its service in May 2010 [4], and Wealthfront a little more than a year later, in December 2011 [5]. The basics of these two services are pretty similar — each uses automation to choose a blend of mostly low-cost exchange-traded funds (ETFs) to create a portfolio aligned with users’ personal preferences for things like retirement timing and risk tolerance. These portfolios are periodically rebalanced to adjust for changing conditions. Each service charges a management fee on a percentage basis. Betterment has no account minimum, and Wealthfront has a minimum of $500, which is low enough to not be a barrier for the vast majority of potential users. Both services offer tax-loss harvesting, another benefit of automation that’s challenging for humans to do on their own [6].

Exhibit 1: NerdWallet summary of offerings from each company [6]

Both companies have grown fast and now manage respectable pools of assets — ~$6B for Betterment and ~$4B for Wealthfront [7]. Even so, this band of merry adventurers is still far from striking distance of the great treasures guarded by traditional asset managers (Schwab has $2.6T in assets under management; Vanguard has $3.5T) [1][8]. These challengers may seem like nothing more than a minor nuisance, but Schwab appears to be taking the threat seriously. They launched their own take on the robo-adviser, Schwab Intelligent Portfolios (IP), in March 2015.

Schwab’s IP product is similar to Wealthfront and Betterment in some respects. The most obvious difference is that Schwab’s product claims to be “free” since it doesn’t charge a management commission or monthly fee. That can be a bit misleading since Schwab draws from its own ETF products to construct portfolios and the ETFs do, in fact, have fees. Even so, the cumulative impact would still seem to put Schwab at a lower cost point compared with Wealthfront and Betterment. There are other differences, such as a $5,000 minimum account size for Schwab and a more limited tax-loss harvesting capability [2].

Though it’s nearly four years late to the party, Schwab’s IP product has already grown larger than Wealthfront or Betterment, surpassing $10B in assets under management as of September 2016 [10]. This is likely owing to the fact that Schwab has a considerably larger traditional asset management customer base to draw from and a stronger brand. Several of the other traditional asset managers have also launched robo-adviser products including Vanguard, TD Ameritrade, and Fidelity. An estimated $72B in total assets is managed by various robo-adviser platforms, with the majority of these assets managed by the traditional asset managers and the remainder spread across various newer entrants. It would seem the “old-guard” is now beating the youngsters at their own game [9].

Performance is another big question. Condor Capital Management launched an initiative last year to track the results of robo-adviser managed portfolios — it opened accounts at 11 companies for the experiment (unfortunately Wealthfront opted not to participate due to a disagreement with Condor about measuring outcomes). Among the participating platforms, Schwab was the top performer with a gain of 10.2% net of fees this year through September [9]. It’s a promising result, but a lot more data is required before we can draw any conclusions about how robo-advisers perform across a variety of market conditions.

We’ll have to wait to see what ultimately becomes of the robot investment managers. It’s clear that newcomers like Wealthfront and Betterment are finally feeling the heat from the more innovative incumbents, like Schwab. Wealthfront, in particular, isn’t going down without a fight. Just last month, Wealthfront reinstated original founder Andy Rachleff as CEO. They’ve stepped up an anti-Schwab PR campaign, claiming that Schwab IP can’t match the tax loss harvesting results of Wealthfront. Rachleff bluntly comments “Not all software is created equal. We believe our software is simply better than our competitors” [11].

(791 words)

[1]https://www.google.com/finance?cid=6025

[2]https://www.nerdwallet.com/blog/investing/charles-schwab-intelligent-portfolios-review/

[4]https://www.betterment.com/resources/inside-betterment/our-story/the-history-of-betterment/

[5]https://www.wealthfront.com/two-billion#launch

[6]https://www.nerdwallet.com/blog/investing/best-robo-advisors/

[7]http://www.investopedia.com/news/why-wealthfront-replaced-its-ceo/

[8]https://about.vanguard.com/who-we-are/fast-facts/

[9]http://www.wsj.com/articles/spotlight-on-robo-advisers-returns-1478018429

[10]https://aboutschwab.com/images/uploads/inline/schw_q3_2016_earnings_release.pdf

[11]http://www.wealthmanagement.com/technology/wealthfront-attacks-schwabs-robo-technology

I think we often hear the cool stories of a new startup coming in and disrupting a traditional industry, so its always good to get a perspective of the flip-side, an incumbent staying tune to trends in innovation and outperforming the startup. I’m assuming that Schwab weighted the cost/benefits of creating its own software vs. attempting an acquisition of Wealthfront or Betterment. Recently that has been an area of interest for me is looking at the strategies behind acquisition vs. internal generation. In the case of asset management, I find it hard to believe that Wealthfront or Betterment will be able to sustain a strategy of “our software is better than yours” given the decades of data, brand recognition, and experience that Charles Scwab has, but time will tell.

Good analysis on a market where incumbents seem to be able to crush the digital start up breed. Money management has always been a conservative sticky kind of business so not the easiest to penetrate with technology.

Indeed it seems absurd that there still 300,000 financial advisers in the USA. As Ric Edelman points out, theyu are likely to disappear. They will mainly be educator going through financial management pedagogy rather than active portfolio advisors.

Then I agree with the conclusion of the post: Money management behemoths have a fair chance to transform and beat new entrants.

The two main assets of existing money managers are indeed their pool of customers/accounts and their brand. If they can leverage those two, they may be able to keep the competition at bay. To some extend time is on their side as people tend to be cautious and slow vis-a-vis money management. As most of the savings are hold by 50y+ people, they aren’t the most tech daring app testers. Money is about trust. Old players are likely to use this to try to stop the leakage to low fees by providing their own solutions.

But as the fee pot is likely going to reduce they have a diverging interest: change to preserve business but wait to keep the high fees ticking… Interesting transition to manage!

Very interesting post! The world of retail investing and advising certainly is facing some whole-scale changes as you mentioned. As a giant in the industry, it is a wise move for Charles Schwab to develop its own software and establish their presence within “robot” investing, even if these emerging companies are taking a tiny amount of market share. Charles Schwab has the resources and as you mentioned, smartly capitalized on its existing base of clients. Personal wealth management is such an important part of everyone’s life, and it does not surprise me that consumers are much more willing to try this “robot” method of investing when it is endorsed by Charles Schwab. The concept of “robot” investing makes a lot of sense to me for certain parts of one’s portfolio. Many mutual funds and ETFs simply track and index, sector, etc. so algorithms are well positioned to carry this out. Have you looked at Quantopian before? They are a start-up whose business is built around using algorithms to displace hedge funds (https://www.quantopian.com/). They are a very creative company we could see on the rise over the next few years!