P2P Lending: LendingClub’s Sprints & Stumbles

A walk-through a company’s ambitions to digitally transform the $3 trillion consumer credit industry.

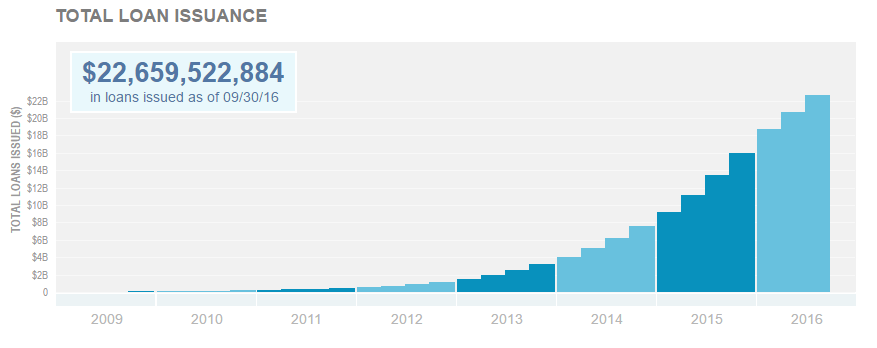

Peer-to-peer lending – or “P2P lending” in Silicon Valley and Wall Street parlance – has set its sights on disrupting the massive $3 trillion consumer credit industry by unleashing the power of digitalization on financial services. [1] Within the space, LendingClub is the poster child and boasts status as the world’s largest online credit marketplace, claiming an impressive $22.7 billion of originated loans since 2009. [2] Its board includes a curated collection of financial leaders, including Mary Meeker and John Mack, as well as Larry Summers, who is quoted on the company’s website as proclaiming:

“LendingClub’s platform has the potential to profoundly transform traditional banking over the next decade.” [3]

Source: LendingClub.

Fundamentally, LendingClub is an online marketplace that tends to two primary stakeholders: borrowers and lenders, and has carefully crafted a value proposition for both constituencies.

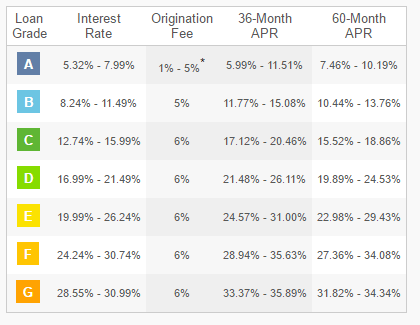

- For borrowers, LendingClub’s menu of credit products, including personal loans, auto financing, and small business loans, competes directly against traditional brick-and-motor credit unions and commercial banks. The value of LendingClub’s loans is created through: access to affordable credit, a superior borrower experience, transparency and fairness, and fast and efficient decisioning. [4] With only a couple of clicks, borrowers skate through a friction-less application process, accessing loans with interest rates ranging from 5.32% to 30.99% and waiting only a few days for funding. [5][6]

Source: LendingClub.

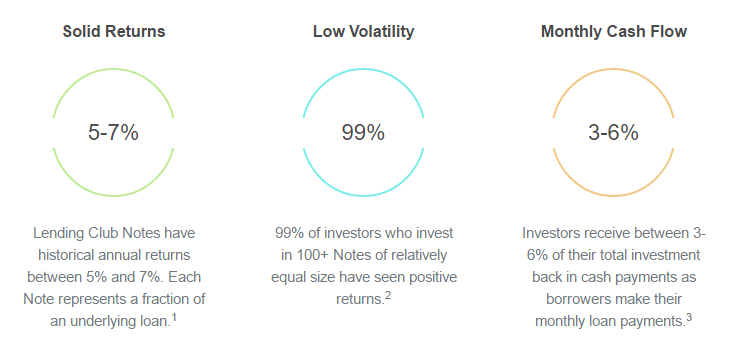

- For lenders, LendingClub offers a diversified and innovatively sourced investment opportunity with fixed income returns of 5.12% to 7.78%. [7] The key value is generated through attractive risk-adjusted returns, which are ultimately driven by the success of LendingClub’s loan underwriting, monitoring, and servicing rigor. Investors can cleanly slice through LendingClub’s loan book to build a customized (by geography, loan purpose, or credit grade) portfolio of direct consumer loans with the right return profile for their appetite.

Source: LendingClub.

Source: LendingClub.

From an operating perspective, LendingClub has embedded state-of-the-art technology across its platform. Chiefly, the digital nature of its operations allows LendingClub to avoid significant costs associated with operating branch infrastructure. Further, it utilizes sophisticated risk assessment technology to evaluate loan applicants, which reaps further cost savings from improved application processing times, optimized pricing, and sharpened risk management. [8] In aggregate, LendingClub postulates that its costs are one-third those of traditional banks [9], which allows it to pass along benefits to its users in the form of lower interest rates for borrowers and higher returns for lenders.

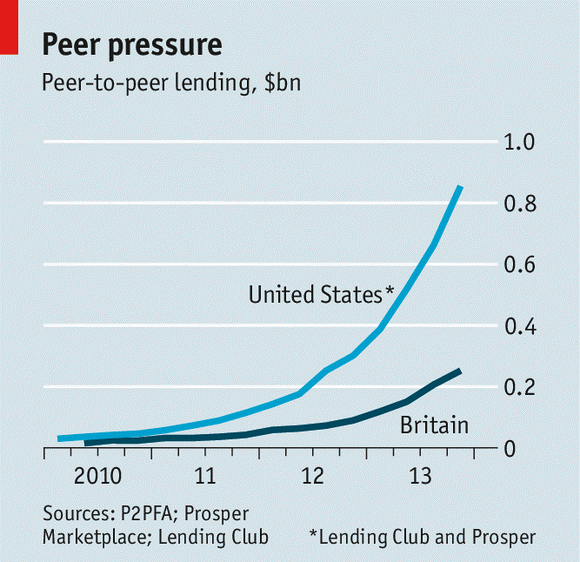

Source: Economist.

Founded in 2009, LendingClub experienced enormous growth and quickly achieved unicorn status and blue-chip venture capital backing. [10] The company was embraced by public markets and IPOed in 2014 at a $8 billion valuation. [11] However, there is concern whether this growth was realized through lax underwriting standards, under-priced loans, and a lack of internal controls. Others note the absence of regulatory oversight as a significant – and potentially dangerous – growth driver for the nascent industry. [9] Until recently, much of these concerns were simply conjecture; however, the music stopped for LendingClub in May 2016, when a $22 million mistake was revealed when a prominent investor was sold loans that did not meet its investment criteria. [12] The incident cast doubt on LendingClub’s loan practices and credibility, which ultimately led to board inquiry and ousting of its Chief Executive Officer and Founder, Renaud Laplanche. The press surrounding the incident spooked the market, sending LendingClub’s stock price down 34% and raising questions on the stability of the whole industry. [12] Looking forward, a tremendous challenge for LendingClub will be to repair investor confidence in its own company as well as in the P2P lending business generally.

An additional challenge that LendingClub faces is to truly realize its “peer-to-peer” concept. Although its borrower base holds true to its “for the people” mission, its lender base is primarily made up of institutional investors. [13] Its messaging of “for the people by the people” [10] falls flat. This lender base composition creates concentration risk and may arguably erode the integrity of the “peer-to-peer” concept. Further, from a purely commercial perspective, the company has not yet proven its ability to generate attractive risk-adjusted returns in a non-zero-interest rate environment. As such, future institutional appetite for LendingClub products may wane, leaving the two-sided marketplace imbalanced, and thus, ineffective. LendingClub could protect against such an imbalance by actively seeding new (and sticky) pools of lenders through stronger marketing efforts.

As LendingClub looks to the future, there is an opportunity for the company to repair its recently damaged reputation and to re-emerge as a leader in the P2P lending space. Its business model and operational model are fundamentally sound; however, the company must diligently maintain the rigor of its underwriting standards and fraud detection practices through constant technological investment and research. Specifically, advances in machine learning and blockchain technologies offer LendingClub the opportunity to sharpen its pricing and risk algorithms and strengthen its fraud protection.

Word Count: 797

—

Sources:

- The Economist. “From the people, for the people”. May 7 2015. http://www.economist.com/news/special-report/21650289-will-financial-democracy-work-downturn-people-people. Accessed Nov 18 2016.

- LendingClub. “Statistics”. https://www.lendingclub.com/info/statistics.action. Accessed Nov 18 2016.

- LendingClub. “About Us”. https://www.lendingclub.com/public/about-us.action. Accessed Nov 18 2016.

- LendingClub. “2015 Annual Report”. http://ir.lendingclub.com/Cache/1001209585.PDF?Y=&O=PDF&D=&fid=1001209585&T=&iid=4213397. Accessed Nov 18 2016.

- LendingClub. “Rates and Fees”. https://www.lendingclub.com/public/rates-and-fees.action. Accessed Nov 18 2016.

- LendingClub. “Personal Loans”. https://www.lendingclub.com/public/personal-loans.action. Accessed Nov 18 2016.

- LendingClub. “Solid Returns”. https://www.lendingclub.com/site/investing/solid-returns. Accessed Nov 18 2016.

- LendingClub. “How Peer Lending Works”. https://www.lendingclub.com/public/how-peer-lending-works.action. Accessed Nov 18 2016.

- The Economist. “Banking without Banks”. Mar 1 2014. http://www.economist.com/news/finance-and-economics/21597932-offering-both-borrowers-and-lenders-better-deal-websites-put-two. Accessed Nov 18 2016.

- Cohan, William. “Bypassing the Bankers”. Sept 2014 Issue. http://www.theatlantic.com/magazine/archive/2014/09/bypassing-the-bankers/375068/. Accessed Nov 18 2016.

- Davidoff Solomon, Steven. “Acknowledging the Value of Lending Club even as it Stumbles”. May 17 2016. http://www.nytimes.com/2016/05/18/business/dealbook/as-scrutiny-mounts-acknowledging-the-value-of-lending-club.html?_r=0. Accessed Nov 18 2016.

- Corkery, Michael. “As Lending Club Stumbles, Its Entire Industry Faces Skepticism”. May 9 2016. http://www.nytimes.com/2016/05/10/business/dealbook/as-lending-club-stumbles-its-entire-industry-faces-skepticism.html?action=click&contentCollection=DealBook&module=RelatedCoverage®ion=EndOfArticle&pgtype=article. Accessed Nov 18 2016.

- Cortese, Amy. “Loans that Avoid Banks? Maybe Not”. May 3 2014. http://www.nytimes.com/2014/05/04/business/loans-that-avoid-banks-maybe-not.html. Accessed Nov 18 2016.

Like many marketplaces, it seems like much of lendingclub’s success hinges upon the network effect of growing borrowers bringing in more lenders and vice versa. Its success going forward likely will be correlated with its ability to offer a superior customer interface and experience. A startup partnering with a large financial institution could potentially provide a better experience very quickly, and take marketshare from Lendingclub.

I’m not sure I agree that there is still an opportunity for Lending Club to repair its business. I think the company has lost its luster and investors, who recently fired the CEO over faulty loans, have lost their patience. The whole premise doesn’t make much sense to me—why would you expect to get better risk-adjusted returns lending to individuals with generally weak credit scores than you would lending to robust corporations? I think, as the article below says, Lending Club is just another one of many companies that shows that there are limitations to what technological disruption can do. [1]

[1] http://www.wsj.com/articles/from-lending-club-to-theranos-the-limits-of-disruption-1463161745

Lending Club is certainly a very interesting business model. It seems that Lending Club has already begun to make a comeback. According to Business Insider, Q3 results show that their comeback strategy is working. Indicators include increase in loan originations and an increased focus on transparency and compliance. (1)

Like Dave mentioned above, competition is a real threat for Lending Club. In fact, just a few days ago, it was announced that Renaud Laplanche, the former CEO of Lending Club who was ousted in May, is starting a new lending site called “Credify.” (2) Few details are available on the new venture, but it’s interesting how quickly and easily Laplanche was able to enter the market. And he certainly has the experience to launch a compelling marketplace. What’s stopping others from doing the same?

(1) http://www.businessinsider.com/lending-club-is-on-a-path-to-recovery-2016-11

(2) http://www.nytimes.com/2016/11/17/business/dealbook/former-lending-club-chief-is-creating-a-new-lending-site.html?_r=0

I agree with Emily’s point that the barriers to entry in this market are just too low for LendingClub to focus on repairing its reputation. Lending is a business built on trust and once damaged, it is almost easier to re-enter the market as a new company rather than live in the shadow of a past disgrace. Established banks may find it easier to provide lower cost and higher quality loans using big data analytics, enabled by digital transformations. While peer-to-peer lending was very exciting a few years ago as it first emerged, I’d be concerned that this market becomes eclipsed by larger institutions as they begin to leverage digital technology.

One of the interesting things about LendingClub is that its growth has mostly come during a period of economic recovery. I wonder how its underwriting and P2P lending model will fair during an economic downturn. Can LendingClub’s returns remain resilient even though their portfolio is purely consumer credit? Evidence from 2008 suggests the service might (http://www.lendingmemo.com/p2p-lending-recession-performance/), but LC may have had different, less lax standards during that period. Also, it’s interesting to think about how these new P2P opaque lenders might lead to reduced ability for banks to see a credit downturn coming. If consumers struggling to repay their credit cards are able to refinance with lax LendingClub loans, first order banks may have a rosier picture of the economy than actually exists. This multi-tiered supply chain of consumer credit could ultimately result in bullwhip type effects within the consumer credit market. In that way, digital lending from LendingClub might be an interesting place to watch for early signs of economic weakness. Digital lending models clearly hold promise, but we have to keep a close eye on whether or not P2P lenders are able to successfully price risk in years to come.

This is a very interesting article – very well researched. One thing that I find interesting that you mentioned is the composition of the supply side of the “P2P” dynamic.

As discussed in the article (http://www.bloomberg.com/news/articles/2016-05-10/lendingclub-is-turning-out-to-be-anything-but-a-direct-lender), institutional capital is a major driver of LendingClub’s business and that leaves a lot of risk that the market unwinds whenever we have another shakeout in consumer credit. I agree that the platform has a lot of potential, but I am very skeptical that these short term yield temptations are not sustainable when volatility hits.

I think it’s really interesting to note that one of the key reasons that lenders flock to these models is the poor rate of return on conventional financial instruments as well as low retail credit rates. In the US, almost no bank gives any substantial return on savings deposits and hence people flock to alternate lending markets to get more bang for their buck. For example, in my experience with similar models in India, one of the key things I learnt was that given savings deposit interest rates of ~8% the incentive to go for some such models is not that high. It’ll be interesting to benchmark average returns of S&P with some such lending marketplaces because if markets start to generate good returns, people might not go for such alternate models.