It’s all about who you know: Lenddo makes credit decisions based on your social network

Lenddo uses social media and smartphone application data to provide credit scoring and verification for the emerging middle class.

Loan applications, credit card inquiries, and even apartment rental requests all essentially hinge on one thing: a credit score. Traditionally, institutions have asserted that an individual’s financial history (primarily payment history, current debt profile, and length of credit history) informs future behavior and therefore should dictate the decision to offer credit to potential borrowers and at what rate. This framework makes sense when the necessary information is available, but what about when it is not?

Unfortunately, in low-income countries it is often the case that no such financial history exists. In recent years many politicians and executives have expressed the need to empower the emerging middle class, reduce poverty, and foster opportunities for a better life.1 However, platforms are not in place to aid this development financially. Given the lack of payment history and even financial accounts within this population, banks do not have enough information on which to base credit scores. As a result, taking out a loan is virtually impossible.2

Enter Lenddo

Co-founders Jeff Stewart and Richard Eldridge took note that with repayment rates in microfinance as high as 98% in some regions, a huge opportunity existed to serve the under- and un-banked middle class in emerging markets who lack access to credit.3 What they realized is that even though much of this population does not have an established financial history, they do have an online presence though social media and data surrounding smart phone usage.4

It is a historical and widely accepted belief that a person’s character is just as important as income or assets in making a lending decision. Current trends including the widespread reach and use of social media combined with the penetration of smart phones opened the door for Lenddo to answer the question: can you use someone’s social media presence and mobile phone data to assess trustworthiness, and therefore creditworthiness?

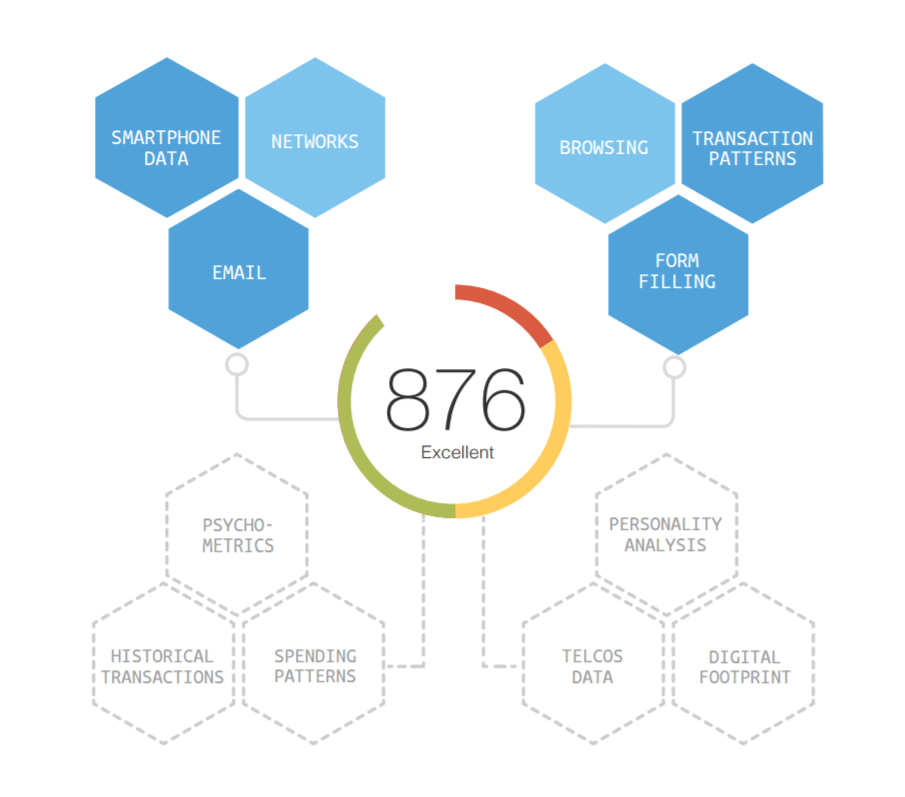

Lenddo developed an algorithm that aggregates data from social media accounts – friends, frequency of interaction, interests, etc. – and other smartphone applications – messaging and browser history, apps, wifi network use, battery levels, etc. – to establish a rating that signals an individual’s likelihood of repaying or defaulting on loans.5,6 This “LenddoScore” is a number ranging from 0 to 1,000, and is said to be a measure of trustworthiness, enabling lending via social networking alone instead of age-old credit score metrics.7 The algorithm has been developed and is maintained by mapping relationships between more than 120 social media profiles on Facebook, Email, LinkedIn, Twitter, and Yahoo.8 Additionally, Lenddo also asks members to select a “Trusted Network” of at least three people. If the borrower fails to pay back the loan, Lenddo scores of their network will also suffer. This additional layer incentivizes friends and family to keep the borrower accountable, as a lower score could affect the chances of being approved for a loan in the future.4

Figure 1: LenddoScore Components

Lenddo starts lending

In the Philippines and Colombia, Lenddo began by granting loans using its own capital, and the results were extremely positive. Default rates were better than the microfinance industry average, confirming the belief that the digital footprint of potential borrowers offers better evidence of loan repayment than a traditional credit score for people just entering the middle class.7,9 In fact, when comparing the Gini Coefficient (assesses the ability of a credit score to predict loan repayments/defaults) in the Philippines, the traditional credit score coefficient ranged from 0.25 – 0.32 whereas the LenddoScore coefficient ranged from 0.32 – 0.39, meaning it had higher predictive power.8

But Lenddo did not stop there. Playing in the lending game was never the end goal. In fact, Lenddo transferred its loan portfolio to a third party and is now focusing on selling its algorithm as a service to financial institutions as an alternative or complementary means to assess credit worthiness.5 Through Lenddo’s cloud-based application programming interface, a financial institution can add code to their lending application allowing customers to opt in and share their social media accounts.3 Lenddo’s goal is to help one billion people get access to financial services by 2020.6 Since launching, Lenddo’s alternative credit scores and online verification services are used in more than 15 countries and the company helps to process tens of thousands of loan applications every month.10

The world beyond loans

What is next for Lenddo? Despite what its name suggests, applications of its algorithm are much more widespread than just loan approvals. Examples of the next generation of uses include:

- Telecom: Verify the identities of plan subscribers and their ability to pay.

- Ecommerce: Prevent fraudulent transactions from both the buyer and seller perspective.

- Online Dating: Authenticate identities of subscribers.

- Corporate Hiring: Quickly validate candidate pre-employment screening information. 5

In a world of increasing online interactions and digital information flow, the opportunities for Lenddo’s service are seemingly endless.

Word Count – 794

Sources:

- Wei, Yanhao.”Credit Scoring with Social Network Data.”Marketing Science. 26 Oct 2015. http://knowledge.wharton.upenn.edu/article/using-social-media-for-credit-scoring/, accessed November 2016.

- Lapowsky, Issie.”How to Get a Loan Without Leaving Facebook.”Wired. 15 May 2014. https://www.wired.com/2014/05/lenddo-facebook/, accessed November 2016.

- Groenfeldt, Tom.”Lenddo Creates Credit Scores Using Social Media.”Forbes. 29 January 2015. http://www.forbes.com/sites/tomgroenfeldt/2015/01/29/lenddo-creates-credit-scores-using-social-media/#fcd40aa3f797, accessed November 2016.

- Hardeman, Bethy.”Lenddo’s Social Credit Score: How Who You Know Might Affect Your Next Loan.”Credit Karma. 15 June 2012. http://www.huffingtonpost.com/bethy-hardeman/lenddos-social-credit-sco_b_1598026.html, accessed November 2016.

- Balea, Judith.”Lenddo stops lending, now helps clients determine customer trustworthiness.”Tech in Asia. 25 January 2015. https://www.techinasia.com/lenddo-customer-trustworthiness, accessed November 2016.

- King, Hope.” This startup uses battery life to determine credit scores.”CNN. 24 August 2016. http://money.cnn.com/2016/08/24/technology/lenddo-smartphone-battery-loan/, accessed November 2016.

- Edquilang, Raya.”Lenddo is Like Klout For Your Credit Rating.”Tech in Asia. 30 April 2013. https://www.techinasia.com/lenddo-social-network-reputation-based-lending-startup, accessed November 2016.

- Popescu, George.”Lenddo- The Google of Lending Algorithms.”Lending Times. 29 February 2016. http://lending-times.com/2016/02/29/lenddo-the-google-of-lending-algorithms/, accessed November 2016.

- Hempel, Jessi.”Banks Are Now Handing Out Loans to People They’d Normally Shun.”Wired. 20 January 2015. https://www.wired.com/2015/01/banks-handing-loans-people-normally-shun/, accessed November 2016.

- Costa, Arjuna.”Why We Invested: Lenddo.”Omidyar Network via Medium. 10 October 2016. https://medium.com/positive-returns/why-we-invested-lenddo-3d1c654f4d62#.3pf6o0669, accessed November 2016.

That’s an interesting discussion. I do agree that social media data could fill holes in the data available to credit scoring particularly where there is little other information about a person. However, since there are some major risks associated with this strategy, it is important to assess the efficiency of this new credit scoring system and compare its predictive power to the traditional methods.

In my opinion, a good way to do this is by taking a group of people with credit history and a heavy use of social media, and assess their credit risk under both methods. Within this context, we would have a solid and objective baseline, which would serve as a parameter to analyze the accuracy of each model. After a year, I would take the default rate of this sample portfolio and compare to the expected default of each method.

Anyways, this is a very valid discussion. The Fin Tech industry will definitely play a big role in the banking industry in the coming years!

I had never heard of this company before but find it fascinating – I personally had a hard time buying my first car because of this exact problem! It also seems to be a rather effective platform, given their default rates are competitive with other microfinance organizations.

I do however wonder if this system introduces new, easier ways to “cheat the system” (as hinted in the article below), given that the algorithms use data pulled from social media sites and platforms, where all the information made available is self-selected by the consumer his or herself. It’s obviously much harder to hide your past payment history and amount of debt you’ve taken on than it is to keep from connecting to certain people on your Facebook platform. You also have to wonder if there will ever be a time where social media platforms do not allow external companies (such as this one) to access and use the data that is found on their users’ profiles.

That being said, this platform certainly seems like a step in the right direction in making credit available to both those who have good credit histories as well as to those who have the potential for high earnings in the future… extremely innovative and creative way to access a previously unserved market.

http://www.wsj.com/articles/SB10001424127887324883604578396852612756398

This was so interesting, thanks for sharing! I have to admit, I’m really curious…and reasonably skeptical…about how more unusual metrics such as battery levels could tie into credit worthiness. Without a longstanding base of past performance of using these metrics as indicators, how was the company able to develop their algorithm’s predicative power? I’m curious whether the users that were initial granted loans using a LenddoScore were just more likely to be well-connected, tech-savvy users that would be more likely to repay a loan anyway than an average citizen in the region. Likewise, are those who are willing to give so much access to their social media profiles and online accounts for some reason naturally higher-quality clients (perhaps because they know they have less to hide?). Not to say that these questions undermine the value of the offering — even if only higher-quality, self-selected populations choose to seek credit under a Lenddo approach, it would still be widening the potential for credit among a traditionally underbanked population.

Another takeaway that I had from this post was that the business model of using a “trusted network” seems very smart. As we learned in the stickK case, accountability to friends / family certainly encourages individuals to stick to their personal intentions. It seems to make a great deal of sense that accountability would also incentivize people to repay their debts.

Fantastic article about a topic that is commonly overlooked! We take for granted in the USA that credit scores actually are not always the best indicator of whether a consumer is likely to pay back their debt. This actually reminds me of the episode that John Oliver did on his job about how flawed credit scores and reports are (https://www.youtube.com/watch?v=aRrDsbUdY_k). I also know that a very large problem applies to recent graduates from schools who are denied cars, apartments or loans because they have a shallow credit history. But we all know that somebody graduating from HBS with a job at BCG is probably going to be able to pay down there loans, so it seems wild that they are being denied!

As Lenddo’s approach is very fascintating, it has its risks, too. And here I will take a controversial standpoint.

Of course, analizing data of social networks and other online websites is tempting in order to achieve different goals whether they are goals of the company or goals of their clients, but, it can also have negative impacts on these clients.

This might be a very drastic example but a possible one. In the 1920s, Munich (Germany) collected a lot of data of its Sinti and Roma with which they were able to be identified easily. This was not a big problem until Adolf Hitler came to power in the 1930s. With the National Socialist German Workers’ Party trying to eliminate different groups of people (e.g. Jews, Bible Students, Homosexuals, mentally ill people, dissidents, Sinti and Roma), the complete eradication became a big goal. With the precise and systematic registration of Sinti and Roma by Munichs officials it became easy to find and deport them.

I do not want to say that companies like Lenddo are comparable to this, instead I want to say that the collection of our data has an impact on our future, we might not know yet.

For further information, please have a look at this interesting website.

http://www.holocaustresearchproject.org/holoprelude/romasinti.html

Access to credit can be a powerful economic development tool; specifically around land and even more so in emerging countries. In these environments, the informal economy leads poses a real problem to understanding a consumer’s ability to pay. Enriching formal data points with the slew of data that the internet has created is a genius solution. I keep on going back to Monte’s map in class on how lending institutions will, even if they have an approvable “credit score”, will not based on where you live as a proxy for your ethnicity. So not only can a platform like Lenndo generate great returns and improves access to credit, it may be a step towards reducing discrimination. Bravo!

Great article, thanks!

It is very interesting to see how digital can enable the middle class to access to capital in a way previously (almost) impossible. I wonder if digital will eventually allow for similar analysis for SME’s. Access to capital is one of the main challenges for informal businesses in Latin America (see: http://comercioyjusticia.info/blog/pymes/informalidad-y-garantias-trabas-para-el-acceso-al-credito-pyme/ ).

I love the idea of this technology, and it’s a shame that regulation around “Know Your Customer (KYC)” limits its use in the U.S. There are nine million unbanked households in the US and another 24.5 million underbanked households that encounter the same issues with accessing loans due to the lack of a credit score (https://www.fdic.gov/householdsurvey/). However, banks are incredibly risk adverse to using social media; from trying to implement a similar technology at Barclays, the argument was that the social media accounts could be faked and that it was then impossible to know who you were really lending to. It’s encouraging to hear other countries are able to use technology like Lenddo and that it’s predictive capabilities have been shown to be better than credit scores, per your Philippines example. So that begs the question, how can we use the mounting body of evidence to convince U.S. banks to utilize similar technologies and also change the KYC regulations to allow for confident use of social media in evaluating credit worthiness?

Have you read about China’s relatively new “social credit” system? It reminds me of what Lenddo is building and in many ways, originated because they were trying to solve the same issues around implementing a credit score. However, with China’s authoritarian government, the risks of building such a system become apparent and very frightening. While high credit scores can definitely be used to give access to certain benefits, low credit scores (especially ones based on non-financial metrics) can also be used to penalize individuals. Because you’re now basing the scores on subjective measures, is there a risk that this becomes a surveillance and censorship tool?

http://www.independent.co.uk/news/world/asia/china-surveillance-big-data-score-censorship-a7375221.html

In Kenya, I’ve seen similar examples of companies that use non-financial information to assess the credit worthiness of an individual and to ultimately provide loans to people. Examples include Branch.co.ke, a lending platform that uses phone data (contacts, call history, messaging history, sums of airtime pop up payments, etc. to determine how much to lend. Branched received $9m in equity funding from Anderseen Horowitz earlier this year.

I’m excited about the prospects of this since many of these ventures are actually increasing access to capital for millions that would otherwise struggle to find loans. Additionally, the fact that default rates on these platforms tend to be really high underscores the immense level of trust that exists on both parties. By the way, I am not sure that the reason default rates are low is because of the social component, because the platforms I’ve seen in Kenya such as Branch and m-kopo don’t actually have social media integration yet are able to maintain much lower than what we see in traditional systems. That said, I’m still not sure what exactly makes people on these platforms so sticky and willing to not default on their loans. This will be an interesting discussion in class, and I’ll try to read more about it.

Thanks for sharing