The UN recently estimated that the global population will grow from 7.3bn in 2015 to 9.7bn by 2050.[1] However, global food demand is projected to significantly outpace this 30% increase due to rising incomes and a consolidating middle class across much of the developing world such that the commensurate increase in demand is nearer the range of 59% to 98% over this same period.[2] One of the main levers in the global food supply chain is yield on arable land, which climate change is projected to significantly negatively impact.

Potassium fertiliser, specifically potash, is a key driver of agricultural yield but its industry is a complex and export oriented one: it is driven by high extraction costs due to deep shaft mining and increasing transportation costs associated with a highly centralised global supply chain. Potash production occurs primarily in Canada, Russia, Belarus, Germany, the USA and Israel. In contrast, the largest agricultural producers include China and the USA, which account for 17.0% and 14.8% of total global agricultural production by tonnage but import more than 50% and 85% of their fertilisers respectively. For Brazil, Russia and Nigeria, the next largest agricultural producers, that import number rises to 95% as of 2014. [3]

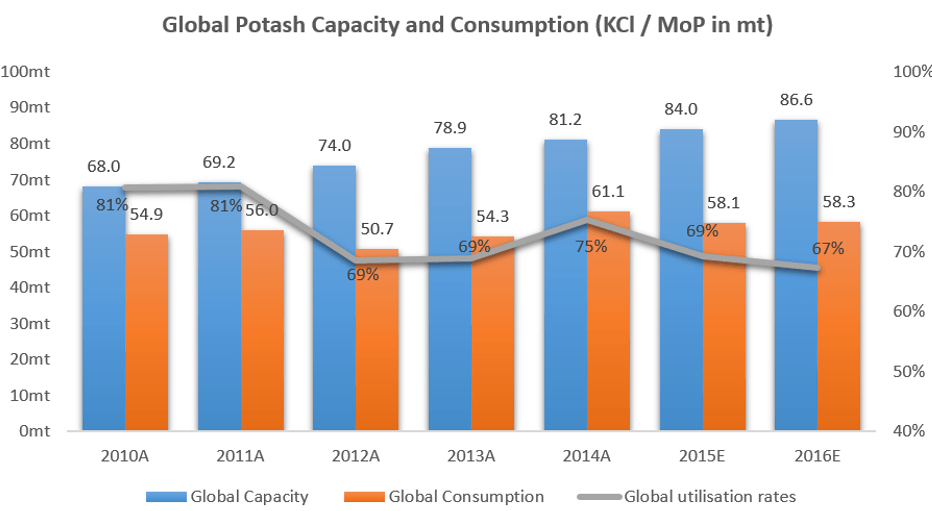

Import dependence breeds a host of related costs across the supply chain, namely currency risk and a higher carbon footprint, which add to the problem the fertiliser is partly solving for. In turn, these costs result in sub-optimal demand levels, a product of both underserved and non-accessible demand where infrastructure is absent (i.e. Africa), while new capacity expansion further pressurised utilisation rates such that the potash fertiliser industry currently operates at 67% of total capacity (Exhibit 1).[4]

Recent consolidation in this sector indicates one supply chain solution the largest fertiliser producers are considering is integration. Indeed, the Agrium and Potash Corp merger announced in September 2016 was in large part driven by this rationale. But a better, lower carbon footprint option may well be available in the form of a low cost, locally sourced fertiliser. APT[5]is developing what it calls HydroPotash (“HYP”) extracted using a patented technology from an abundant form of potassium known as feldspar, plentiful in fertiliser import dependent regions, namely Brazil and Sub Saharan Africa. Historically, technology has limited extraction to potassium predominantly found in current potash exporters and made feldspar effectively redundant. But now the end cost of HYP to the individual farmer is potentially significantly lower than any other current chemical fertiliser on the market due to lower capital and operational expenditures, including lower transportation costs, water and energy consumption and more limited waste.[6] Unlike the more commonly used potash fertilisers, HYP has a cumulative regenerative impact on degraded soils such that it improves soil fertility over time, as well as stimulating fungi and bacterial populations. Moreover, HYP does not include harmful environmental components such as chlorine found in traditional potash fertilisers.

HydroPotash is partly a response to acute demand pull in global food production but also to the high cost of prevailing fertilisers, in large part a product of existing players’ highly centralised and unwieldy international supply chains. Though industry consolidation seems to be one of the more common strategic routes taken, it does not solve for the reality of either (1) the exogenous pressure of greater climate variability on international supply chains (e.g. extreme weather events[7] creating or exacerbating the bullwhip effect), or (2) regulatory pressure regarding carbon emissions, which global firms are under pressure to comply with. The solution will not be found in the supply chain exclusively but also in the original product, i.e. HYP, among others, that allows for a significantly shorter decentralised supply chain, while delivering higher margins with lower energy consumption. For the larger industry players, the new normal must be a combination of re-balancing their product portfolio towards innovative technologies such as HYP as well as M&A to integrate supply chains. Many of them are already doing this. The question is: how fast can they move?

Word count: 793

[1] DESA, The United Nations, World Population Prospects: Key Findings and Advance Tables, 2015 Revision

https://esa.un.org/unpd/wpp/publications/files/key_findings_wpp_2015.pdf

[2] R D Sands, D Van der Mensbrugghe, G C Nelson, H Ahammad, E Blanc, et al. The future of food demand: understanding differences in global economic models. Journal of the International Association of Agricultural Economists, 2013 Dec; 10.1111/agec.12089

http://onlinelibrary.wiley.com/doi/10.1111/agec.12089/full

[3] Food and Agriculture Organisation of the United Nations, Statistics Division http://faostat3.fao.org/browse/Q/QI/E

[4] APT Investor Presentation, October 2016, JP Morgan estimates.

[5] Advanced Potash Technologies (joint enterprise between the Brazilian firm Tarrativa and the Allanore Lab at MIT) https://mpc-www.mit.edu/component/k2/item/388-a-new-source-for-potassium-fertilizer#&ts=undefined

[6] Conversation with Philip Wender, Director of Advanced Potash Technologies.

[7] http://www.pwc.com/gx/en/services/advisory/consulting/risk/resilience/publications/business-not-as-usual.html

This is a great piece, LC.

That agriculture innovations have dramatically increased crop yields without increasing agricultural land use has been one of the great success stories of the past century. HYP certainly seems poised to follow in this tradition, given its low cost and ability to replenish soil. And I think you’re right to point to the need for large industry players to invest in these technologies and incorporate them into their supply chains.

I can’t help but wonder, though, about the public’s response. While the environmental case for HYP seems strong, I worry about whether consumers and activists will be able to distinguish it from other potash fertilizers (ie, those that harm soil with chloride) that the USDA and other regulatory agencies have deemed unacceptable for organic growing standards.[1] This is, of course, a major concern given that the public’s skyrocketing demand for organic and non-GMO foods is already challenging the ability of large industry players to maintain current yield-per-acre ratios. GMOs in particular have gotten a bad rap, despite scientific consensus that they are safe to eat and a boon to sustainability.[2] While Cargill has been a strong advocate for GMO foods, they’ve also invested heavily in non-GMO crops in order to keep up with demand from food processors, who are in turn responding to consumer demand.[3] Given its enormous potential to increase yields in a sustainable way, I would hate to see HYP suffer the same fate.

[1] http://www.nrcs.usda.gov/Internet/FSE_DOCUMENTS/nrcs144p2_045863.pdf

[2] https://www.scientificamerican.com/article/why-people-oppose-gmos-even-though-science-says-they-are-safe/

[3] http://www.cargill.com/news/releases/2016/NA31979657.jsp

The problem of how the world will feed its growing population is extremely important and concerning. I was particularly struck by the fact that food demand is expected to increase by 59% – 98% through 2050. The implications of not meeting this demand are difficult to fully comprehend. As climate change continues to alter global weather patterns in unpredictable ways, parts of the world will likely experience famines, which could lead to violent conflict and/or large numbers of refugees. Recent events have unfortunately shown that the world is not equipped to deal with regional conflicts or mass refugee situations and the outlook only gets worse as we approach 2050. The post above points to new types of fertilizer to help meet global food demand, but I wonder if a more radical approach is needed. Genetic engineering, urban farming and cultural changes must all be on the table to ensure that global food production can keep up with demand.

Part of the issue of feeding the ever expanding population is our over-consumption of foods which have very low energy efficiency. According to an article published in Scientific American, “Meat is four times as demanding as grains are. If consumers would gravitate toward less intensive foods, energy use would drop.” (https://www.scientificamerican.com/article/webber-more-efficient-foods-less-waste/). Beyond increasing crop yield with fertiliser products such as HYP, I wonder whether we could tackle the potential of a ‘Malthusian catastrophe’ by being more environmentally conscious in our eating habits. Historically the ethical focus of vegetarianism has been on the unethical nature of harming living creatures – should we also be considering the ethical nature of meat from an environmental standpoint?

More controversially, could we look more seriously at alternative meat products with higher energy efficiency, such as insects? In an independent research project I conducted in high school in 2008, I discovered that the protein content of edible insects in Thailand were comparable to more conventional meats, and were unsurprisingly significantly easier and more environmentally friendly to cultivate. These benefits are widely known (http://www.fao.org/edible-insects/en/), but the entomophagy movement has yet to gain enough momentum to sway the general public towards eating insects!

This article is quite interesting as it highlights how the pressures of climate change can pose an attractive opportunity for new technologies. Innovation like HydroPotash have the potential to experience high penetration if they can be delivered at a competitive cost post. As such, the potential opportunity for new technologies pressures large corporations to invest to remain competitive as the risk of climate change and its impact receives more attention. I also wonder if we will experience a shift in the public viewpoint of similar technologies. The debate regarding engineering crops and implemented new technologies may shift as the food demand becomes more difficult to fulfill. Industry can be a power stimulant and accelerator of science. Is there a way to accelerate the product development lifecycle in this space? Could government initiatives on big data sharing (similar to the Cancer Moonshot) be implemented to increase awareness and drive innovation in the development process, bringing industry and academia together? The time to act on climate change is now and the technology may be near, but how can we push it to move faster?

I agree with the author that fertilizer will continue to be one of the responses to ensure that food production will keep up with food demand, especially while waiting for new, innovative solutions to emerge. But one thing we must address as soon as possible is this “spray and pray” mentality that is prevalent in modern agriculture. It is becoming more and more clear that with the environmental changes happening around us, we need to be far more methodical in our approach to agriculture. Supporting and investing in new ways to deliver fertilizers, added nutrients and pesticides in a more tailored and precise way to address the specific needs of each crops, in each climate and environment in which it is grown, should be one of our top priorities. This would support higher yields, which would result in less required farmland and could potentially enable us to do agriculture in places we would have otherwise not deemed auspicious. Being able to diversify/disperse our centers of agriculture from the traditional clusters we see nowadays would help relieve the food-access inequality we see today, shorten the supply chain, increase quality and freshness and altogether reduce the carbon footprint (which today is further amplified by the oftentimes ridiculous distances our food has to travel from field to fork). This is an extremely interesting topic and one that will become more and more “mainstream” throughout our lifetime.