Helvetia: a Swiss insurer on time with digitalization

While Fintechs (financial technology companies) have been transforming the banking industry for a decade, traditional insurance companies had, until recently, been protected by a heavy regulation and the complex nature of their products. It is now time for them to face the digital reality.

The rise of the Insurtech industry

The last few years have seen the apparition of the Insurtechs: technology-led companies, usually startups, taking advantages of either new technologies or lowered regulatory obstacles to enter the insurance landscape. Entrepreneurs are not the only ones who saw this opportunity – investors have fueled this growth: investments from venture capitalists in this industry has increased from $400 million in 2014 to more than $1 billion in 2016. [1]

Usually, the arrival of a new entrant, or in this case, a whole fleet of them, raises the question “threat or opportunity?” for incumbents. While the Fintech experience demonstrated the importance of partnering with startups to embrace such an important shift [2], the insurers are still lagging banks in this area. In 2016, only 38% of insurers were working with startups and universities on digital initiatives versus 60% for banks. [3]

Despite these numbers, the situation does not look too bad for incumbents. A study from McKinsey reveals that 61% of these new entrants are actually focusing on enabling the insurance value chain instead of disrupting it. [4] A real opportunity for insurers that could impact them across the whole supply chain:

• Distribution and customer interaction: from online identity verification to accelerate the customer acquisition to a full digital portfolio of products

• Advanced analytics: from fraud detection using machine learning and big data to new pricing schemes based on IoT devices [5]

• Internal efficiency: from the automation of claims procedures to fully integrated processes across the organization

Helvetia and its 20.20 strategy

Helvetia, one of Switzerland’s leading insurance companies, knew it had to evolve or risk losing market share and came up with an answer: the 20.20 strategy [6], a comprehensive digitization solution covering the three main axes mentioned above. According to Helvetia Chief Executive Philipp Gmuer, «This strategy is making Helvetia more agile, innovative and customer-focused.” [7]

One of Helvetia’s initiatives was the creation of an InsurTech accelerator to support startups in the insurance industry and, more precisely, startups that fit in Helvetia’s core business. In addition, Helvetia launched a Venture Fund of CHF 55 million (approximately $55 million) to supplement that effort and will focus on European Insurtech startups in their early or late stage.

With their subsidiary “Smile direct”, Helvetia controls 22% of the online insurance market in Switzerland and keeps expanding into new territories through acquisitions or internal innovations (e.g. Helvetia was the first insurer in Europe to launch a chatbot to renew insurances).

On the longer term, and in addition to strengthening their core business, Helvetia aims at developing new “Ecosystems”. The Helvetia Innovation Lab at the university of St Gallen conducts research in the domains of Home, Mobility, and Health, where it became “apparent that business model innovations need to be studied and analyzed from an Ecosystem perspective.“ [8] Their first ecosystem “Home” was launched in 2016 with the acquisition of the two leading mortgage brokers in Switzerland.

Helvetia’s CEO Philipp Gmuer concludes that the strategy 20.20 “is also creating the conditions needed for fully exploiting the opportunities offered by digitalization.” [7]

Acquisitions is not the end game

Despite these efforts, it is only the beginning of Helvetia’s journey. Like most incumbents, it will have to face the inertia of its organization and, by solely focusing on investments and synergies, might miss on a truly radical transformation.

After decades in a stable environment, creating the buy-in from its employee and fostering a culture of innovation is paramount for Helvetia. Buy-in not only means involving employees in the generation and implementation of new ideas but also think of new incentive schemes that will allow these ideas to mature. Helvetia must challenge and invest in its employees: if Helvetia wants to become more flexible and customer-centric, it will have to train employees and managers to give them the appropriate tools (design thinking, agile framework, etc.) to take on this challenge.

In order to go from playing catch-up to leading the way, Helvetia will have to win “the battle for technology talent”. [9] Indeed, with the explosion of tech startups in recent years and the Big Tech companies (Apple, Alphabet, etc.) that keep getting bigger, developers and other digital specialists have plenty of opportunities.

Are they going fast enough?

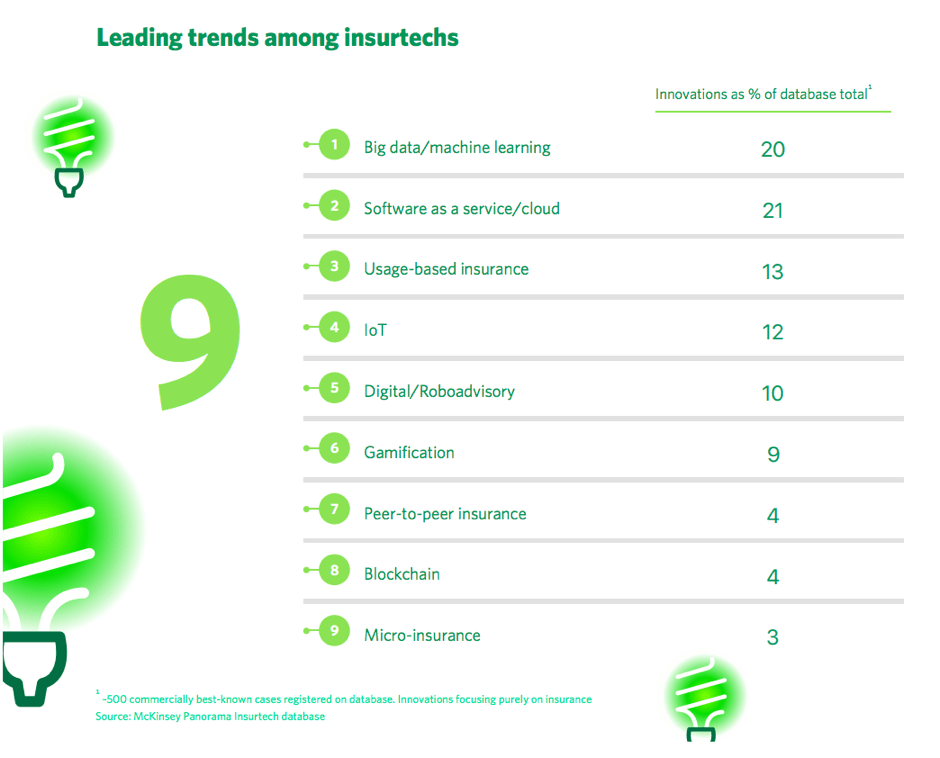

Technologies keep maturing and the Blockchain technology has gathered enough momentum to threaten again the insurance industry. Indeed, the emergence of smart contracts and the increased transparency on the blockchain could facilitate the development, already initiated, of Peer-to-Peer insurances [10], one of Insurtech least represented trends (figure 1).

Figure 1 [4]

(Word Count: 798)

Sources:

[1] Martin Blake, Tek Yew Chia and Murray Raisbeck, „Insurtech: The innovation imperative continues“, KPMG, 2017, p. 2, https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/06/the-innovation-imperative-continues.pdf

[2] “Financial technology is proving less of a battleground than feared”, The Economist, May 6, 2017, https://www.economist.com/news/special-report/21721505-relationship-between-banks-and-technology-companies-becoming-increasingly

[3] Roy Jubraj, Steven Watson and Simon Tottman, “The Rise of Insurtech”, Accenture (blog), 2017, p. 9, http://insuranceblog.accenture.com/wp-content/uploads/2017/04/Accenture-Insurance-Insurtech-Report-2017.pdf

[4] Tanguy Catlin, Johannes-Tobias Lorenz, Björn Münstermann, Braad Olesen, and Valentino Ricciardi, “Insurtech – the threat that inspires”, McKinsey, Mar. 2017, https://www.mckinsey.com/industries/financial-services/our-insights/insurtech-the-threat-that-inspires

[5] Michelle Canaan, John Lucker and Bram Spector, “Opting in: Using IoT connectivity to drive differentiation”, Deloitte, Jun. 2, 2016, https://dupress.deloitte.com/dup-us-en/focus/internet-of-things/innovation-in-insurance-iot.html

[6] “Strategy Helvetia 20.20”, Helvetia, Sep. 2017, https://www.helvetia.com/content/dam/os/corporate/web/de/home/%C3%BCber-uns/auf-einen-blick/strategie-2020/helvetia2020_strategy.pdf

[7] “Helvetia posts higher profit and is making good progress with the implementation of its strategy”, Helvetia press release, Sep. 4, 2017, https://www.helvetia.com/corporate/web/en/home/media-and-stories/overview/media-releases/2017/20170904.html

[8] University of St. Gallen, “Helvetia Innovation Lab”, https://item.unisg.ch/en/divisions/innovation-mgmt/research/helvetia-innovation-lab, accessed November 2017

[9] James Kaplan, Naufal Khan and Roger Roberts, “Winning the battle for technology talent”, McKinsey, May 2012, https://www.mckinsey.com/business-functions/digital-mckinsey/our-insights/winning-the-battle-for-technology-talent

[10] Pauline Adam-Kalfon, Selsabila El Moutaouakil and Corentin Richard, “Blockchain, a catalyst for new approaches in insurance”, PwC, 2017, pp. 14-15, https://www.pwc.com.au/publications/pwc-blockchain.pdf

How is Helvetia dealing with potential regulatory concerns of the new and untested tech innovations?

Insightful article on an industry traditionally obscured behind a veil of complex regulation and poor emotional connection with its customers. I fully agree that Helvetia, along with other insurers, needs to foster a a culture of digital innovation and win the “battle for technology talent”. However, this is easier said than done. The top-tier talent required to develop innovation in a heavily regulated and error-sensitive industry such as insurance will come at a very high price, which will put further pressure on the bottom line in an already constrained profit environment within the insurance industry. Furthermore, even if Helvetia is willing to pay a fair market price for this expertise, I see a big challenge in attracting this talent to put their knowledge to use within the insurance industry. Traditionally not seen as a “cool” industry to work in, but rather an “old boys’ club”, it will take considerable marketing effort on Helvetia’s part to attract and retain the talent they need.

Agree with Simon that this feels like an uphill HR/human capital challenge for Helvetia as much as a strategic shift. I think creating the Innovation Labs at University of St. Gallen was such a smart, long-term move–connect with younger, eager students who may have fully formed their opinions on insurance companies and may be attracted to being part of something exciting and new. The more they can develop relationships like that with St. Gallen’s, the better their chances of success in insurtech feel.