Crowdsourcing Alpha: Can Quantopian Re-invent the Hedge Fund?

FinTech startup bets big on the “wisdom of the crowds” in systematic investing

In late 2012, Boston-based entrepreneur John Fawcett published the “Quantopian Manifesto”, a blog post that outlined the genesis of the company he had just co-founded. He wrote, “Wall Street’s culture was born in an age of information scarcity…[but] the world has changed. The new scarcity is people: people with the talent and drive to wring insight from all of that data.”[1] With that vision in mind, the company soon released its first version of the Quantopian IDE: a cloud-based development environment that allowed anyone to build and test systematic investing strategies using the Python programming language.

The goal was that by building a community of “quants” amongst the 30 million STEM-educated professionals around the world—and providing a forum in which they could collaborate and improve upon each other’s code—Quantopian could identify latent investing talent that traditional investment firms might miss. The promise of the vision, team, and product has attracted $49M of VC investment from prominent firms, including a $25M Series C round led by Andreessen Horowitz and Point 72 (FKA SAC Capital) earlier this week.[2]

The New Model for Systematic Investing

The firm iterated through several business models in its early years (i.e., monetizing on retail brokerage commissions, selling subscriptions for live trading, licensing the platform to other funds) before settling on its ultimate goal: becoming the world’s first crowd-sourced hedge fund.[3]

Quantopian operates in some ways like any other fund – it raises capital from institutional investors and manages it in exchange for management and performance fees (typically 2% and 20%, respectively). However, Quantopian doesn’t hire any investing talent directly; instead, it analyses all of the algorithms created by its community, licenses the best ones, and rebates 10% of the overall net profit from each strategy back to the creator.[4] Rather than recruiting at top pHD programs, the company attracts new programmers similar to other “Business to Developer” startups (e.g., GitHub, StackOverflow): through word of mouth, community building efforts and free education about systematic investing.

Another key difference is in the technology stack. While Quantopian manages all the infrastructure required to execute trades (e.g., market data, order management and broker connectivity), it also has to build and maintain a developer-facing website. Thus, the company has built an engineering team with expertise in web development—an expensive skill set not often found at the traditional hedge fund.

Challenges ahead

Quantopian has executed well on its near-term goals, growing its community to 100K users (~110% CAGR since 2014) and attracting $250M in LP funding from Point 72 for the new hedge fund strategy[5]. Despite the hype and the attention from the VC and hedge fund communities, the company is still in its early days, and faces some key questions ahead:

Will Quantopian be able to generate returns?

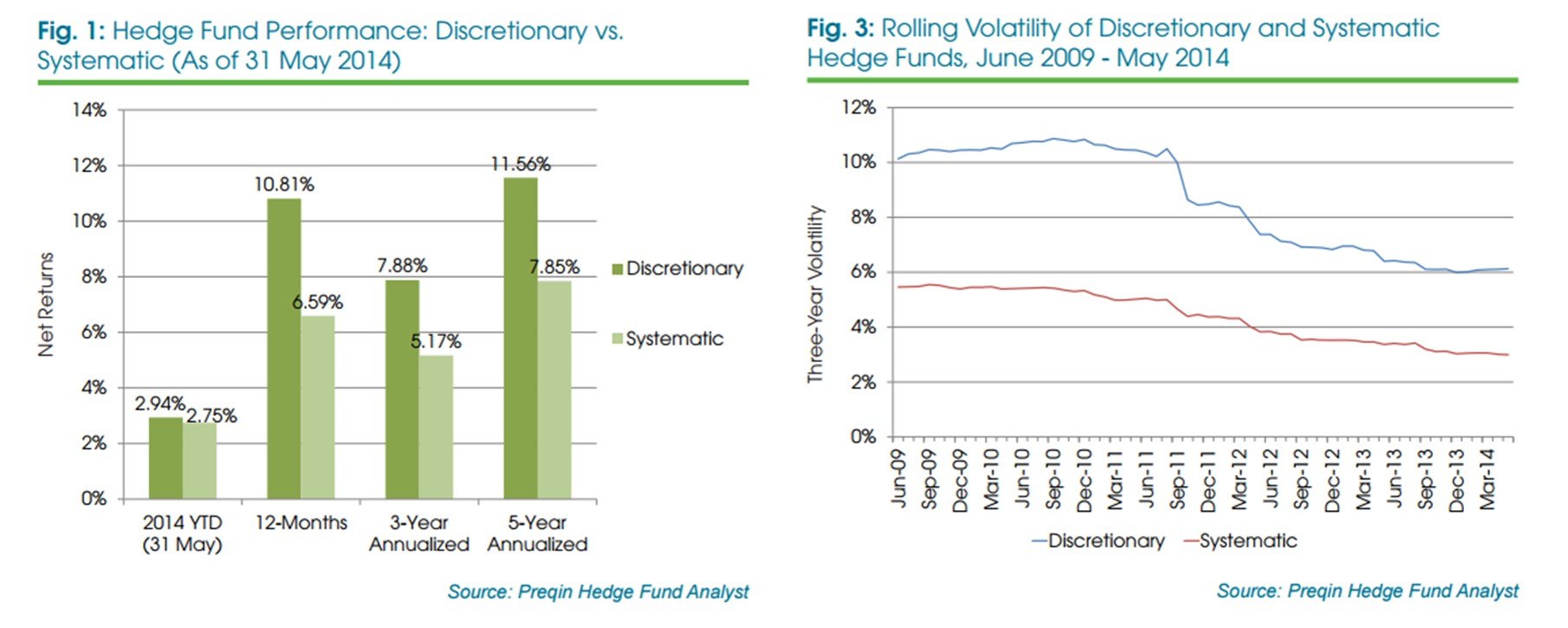

Quantopian has committed to the philosophy of systematic investing—however, these strategies have underperformed discretionary funds over the last several years (albeit with lower volatility).

There may be an inherent flaw in Quantopian’s model as well. Because the company doesn’t look at the underlying code for each algorithm in its portfolio, they miss the opportunity to optimize at the position level. For instance, one strategy might go long Apple while the another goes short, but Quantopian can’t net the two against each other. Nonetheless, early results showed promise: in the first quarter of 2016, the Quantopian fund returned 1.93% net of fees, beating the S&P 500’s 0.8% return. However, Fawcett stressed that the time horizon was too limited to get excited.[6] In order to broaden its investor base beyond Point 72, Quantopian needs to develop a multi-year track record and prove that the crowdsourced model works as they increase AUM and leverage. Amidst an environment that is increasingly skeptical of hedge funds and their fee structures, this will prove crucial.

Is Quantopian’s operating model sustainable?

Quantopian’s long-term success will depend on being able to sustain each side of the marketplace. On the investment side, it needs to properly incentivize quants to stick with the platform and continue submitting algos—however, it stands to reason that the best performers may end up striking out on their own if given the chance to capture more of the ecomomics for themselves. On the capital side, they need to attract enough assets to fund Quantopian’s operating expenses, which to date has come from venture financing. Furthermore, the company must grapple with how to return capital to these VC investors, who traditionally rely on M&A or IPO exits for their investments—these events are relatively rarer in the hedge fund space than in software / biotech.

Win or lose, Quantopian’s model has certainly shaken up the industry—but only time will tell whether the “wisdom of the crowds” truly can beat the market in the future.

(796 words)

[1] John Fawcett, “The Quantopian Manifesto,” Quantopian Blog, September 10, 2012, https://blog.quantopian.com/quantopian-manifesto/, accessed November 2016

[2] “Quantopian Raises $25 Milion in Series C Funding Round Led by Andreessen Horowitz,” Business Wire, November 14, 2016, http://www.businesswire.com/news/home/20161114005847/en/Quantopian-Raises-25-Million-Series-Funding-Led, accessed November 2016

[3] “Quantopian Attracts $15M in Series B FUnding led by Bessemer Venture Partners.” PR Newswire, October 16, 2014, http://www.prnewswire.com/news-releases/quantopian-attracts-15m-in-series-b-funding-led-by-bessemer-venture-partners-279399942.html, accessed November 2016

[4] Quantopian, “Fund Overview,” https://www.quantopian.com/fund, accessed November 2016

[5] John Fawcett, “Quantopian to Manage up to $250M of Investment Capital,” Quantopian Blog, July 27, 2016, https://blog.quantopian.com/q-to-manage-up-to-250m-of-investment-capital/, accessed November 2016

[6] Robin Wigglesworth, “Fund using Freelance Programmers Beats US Stock Market,” Financial Times, April 5, 2016, https://www.ft.com/content/0808729a-faa6-11e5-b3f6-11d5706b613b, accessed November 2016

Note: this post also draws from conversations with company management and Quantopian’s Series A Investment deck, May 2013.

Great post! I personally have a few friends who are professional traders and have experimented Quantopian for trading. From them I got feedback such as “too simplistic and missing a ton of features… most users are extremely unsophisticated.” I agree that Quantopian needs a lot of money, and because of this I am skeptical if it can achieve sustainable success.

I think its biggest dilemma is in its funding. Because for the amount of startup funding it has got, it is expected to get tons of users to justify the next round funding. However, beginner traders and trading experts are two very different markets. While Quantopian focusing on getting general public to on board, it seems its lack of advanced features doesn’t help professional traders much. They need to make people profitable in long term, but at the same time, the number of profitable traders are generally small. If they devote a large percentage of their company’s effort to take care of the small percentage of users, the return of investment is too low to justify especially when they need more funding in the futures. I think that in the longer term, they have to get the winning users to fund the general public playing, and get more people from the general public to the winner users and so the cycle can continues, but I have strong doubt on that with the current state of the platform.

DSN – great write-up. NovChopin – great comments.

Quantopian’s “sweet-spot” is the quant who is skilled enough to find a mispricing that can be systematically exploited, but is not sufficiently capitalized or sophisticated (from a trading systems perpspective) to take advantage of that mispricing. Numerai is a business that is similar to Quantopian, and is backed by a RenTec founder. This business model fundamentally depends on the funnel of newly-minted STEM graduate degrees – this sounds to me like a great business model. As aspiring MBAs and TOM students, we should probably admire this sort of business architecture. The parallels to some of our previous cases are clearly there – maximize the initial data funnel, and use the best items in the funnel for monetisation (sounds a bit like Threadless).

But is this thing really ‘beautiful’ or ‘useful’ from a societal perspective? Does being a good quant help anyone other than yourself? Hundreds (or thousands) of the world’s STEM Phds every year are defecting from hard sciences to dedicate themselves to becoming quants. They would probably do more good for the world had they stuck with science. Imagine an alternative state of the world where an Elon Musk or a Jeff Bezos went into quant finance instead of starting Tesla, Amazon or Blue Origin; something like this probably is happening every single day, and we’ll never even know about it.

A handful of quants who make it to the top (Simons, Shaw, etc) become fabulously wealthy and engage in large-scale philantropy. But many are probably wasting their lives, and are creating a deadweight utility loss to society. To be fair, this argument could be extended to any other purely rent-seeking profession out there.

P.S. Bezos was a quant in the early 90s, but luckily for all of us, he ditched being a quant to do something else.

While I am a strong believer in the benefits of quant investing and believe that Quantopian’s mission is a noble one, I am highly skeptical that the current business and operating model described here will deliver value to investors in the long run. As with any investment approach, quant investing has its benefits and drawbacks. On the benefit side, well executed quant strategies can provide better diversification, much more effective risk management, avoid behavioral biases, and (for managers that invest in their trading platforms) provide best in class execution. On the drawbacks side, a quant investor definitionally lacks the ability to engage with management and incorporate more qualitative inputs. Most notably, quant strategies are often criticized for being “data-mined” or engineered to have amazing results on historical data with no economic intuition for various data patterns to proceed into the future.

While Quantopian’s model does bring “fresh ideas,” it aso removes many of the advantages and exacerbates the disadvantages of quant investing. Not being able to net out trades (being long apple in one place and short in another as the article describes) is a HUGE cost to investors. Moreover, not being able to see the underlying model components and how that interacts with other parts of the model makes sophisticated risk management programs and diversification standards incredibly difficult to implement. Thoughtful algorithmic trading is also difficult if you don’t have a sense of the urgency to trade or the time horizon for the “alpha” to materialize. Lastly, the method by which they ask their users to create strategies is very suspect. 14 years of data (what is provided to users to build their strategies on) is a nanosecond in the realm of empirical data and doesn’t even encompass most types of economic conditions to evaluate the strategy. Further, not being able to ascertain whether the strategy has an economic basis (i.e. is there a reasonable story for why the premiums being captured in the backtested model should continue in the future) leaves very little ability to safeguard against data mining.

Really interesting write up. I think Quantopian is a really interesting concept with a lot of promise but I do worry about the long-term sustainability of the business model. Inherent in the assumption of the business model is that there is latent investment talent that has been untapped by hedge funds and that in a way the company will be able to pool the talent of these individuals in order to create a strategy that will outperform the market. I question, like you, the investment professionals desire to stay on such a platform if they recognize that their strategy is one that Quantopian is trying to license (why not leave the platform for greater economics).

Thanks Doug. I think this is an interesting idea but as you mention, I think the key challenge for Quantopian is their ability to retain high performing quants. If the best algorithms are taken out of the Quantopian system, then what value – apart from academic learning – would Quantopian provide? I wonder if quant hedge funds could find ways to leverage Quantopian for recruitment or assessment purposes – whether it’s to help identify potential candidates or verify the ability of early tenure quants they hire.

DSN, thanks for this post—it was right up my alley! This is like the Threadless of quant trading!

I find myself with mixed feelings about the strength / viability of this model. On one hand, I do believe in the power of the masses. I’m sure there are really smart and motivated people out there that could come up with creative, market-beating algorithms. However, given the incredibly limited number of algorithmic trading jobs reserved for only the most pedigreed applicants, most of these folks will never get a chance to develop their ideas. Providing the masses with a platform to create and test their ideas seems likely to produce some great algorithms.

Beyond the fact that it sounds like the platform itself still needs a lot of improvement, I struggle with how Quantopian “analyses all of the algorithms created by its community” to select the best ones. For this platform to succeed, it will ultimately need to show that it can sustainably generate alpha. Even if you accept the premise that some good algorithms will get created, Quantopian is still dependent on its ability to find these among inevitability an even larger number of bad ideas. While this may seem like an easy task, I’m guessing it’s not. Data mining can result in the creation of algorithms that fit the historical data incredibly well but are not actually predictive of market movements in the future (i.e. they pick up on spurious historical correlations). My intuition is that it wouldn’t be that easy to figure out what patterns (which algorithms can then trade on) are likely to persist into the future. Interested to see how this turns out!

Doug, thanks for this post. It’s fascinating to think about how algos and systematic trading might disintermediate financial services as we currently know them. But as has already been mentioned I do worry about the sustainability of the underlying investment idea funnel, whereby the best investors beta test their strategies and then move on quickly. It would make sense to price participation accordingly and either (a) require non-competes for a set amount of time for each participating investor and their strategy, or (b) deliberately alter the business model as has already been highlighted above such that Quantopian operates as a recruitment funnel for other funds.

(1) http://www.businessinsider.com/r-steve-cohen-bets-250-million-on-firm-that-uses-algorithms-2016-7

(2) http://www.bbc.com/news/business-35830311

Wow, fascinating post! As a former hedge fund analyst and math geek, I really enjoyed reading this. It’s a little unsettling for the hedge fund industry if a crowd-sourced quantitative hedge fund can perform better in the long-term without any investment analysts.

I wonder if their 2/20 pricing model is sustainable. Fees are coming down in the asset management industry overall and especially for a crowdfunding quantitative fund (there should be little overhead), I could see institutional investors being wary of whether the 2% management fee is appropriate. Roboadvising firms typically charge less than 0.5% management fee (take a look at Wealthfront for example which charges 0.25%: https://www.wealthfront.com/our-low-fees).

Also, I would think about how they protect themselves from capital outflows in this early stage as they’re proving out this model. They are dependent on crowd-sourced talent so it’s possible that the best engineers are not yet on their platform. I would be selective about how much capital they take from investors and put stringent lockups on this capital so that they have time to prove out this model.