Clean Tech VC: A Decade of Failure

Sometimes throwing money at a problem can be counterproductive. Here is one take on how Climate Change and resulting regulations affected an entire investment industry.

The year was 2006. Oil prices had increased by approximately 400% since 1998, and Goldman Sachs was calling for a steady state oil price of $200 per barrel.[1] Al Gore had just released An Inconvenient Truth, and George Bush just recently passed the Energy Policy Act of 2005, giving billions of dollars to renewable energy companies.[2] Headlines read Green is Good [3] and The Smart Money is Going on ‘Clean’ Technologies.[4] Clearly it was the dawn of a new energy era, and investors were chomping at the bit to be the first movers in this sector, where government subsidies and cash infusions were sure to keep companies growing.[5]

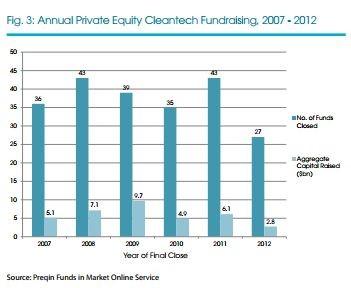

Limited Partners (L.P.s), such as University Endowments, Philanthropic Institutions, Pension Funds, and Fund-of-Funds were eager to allocate large portions of their venture capital portfolios to clean tech funds (G.P.s). Between 2004 and 2012 they invested approximately $25 billion into clean tech strategies. One of the largest and most vocal proponents of clean tech funds, Khosla Ventures II, raised $200 million in 2006 from investors. Vinod Khosla, the founder, publicly stated that he was “thinking outside the barrel”[7] by investing 40% of the fund in alternative energy technologies.[8] Some funds allocated even greater percentages of their portfolios to clean tech. John Doerr from Kleiner Perkins announced that he thought “Green technologies…is bigger than the Internet.”[9]

In 2009 President Obama passed the American Recovery and Reinvestment Act, which encouraged spending of up to $100 billion into clean tech companies. Despite the wider macroeconomic downturn, these new regulations made clear that the clean tech industry was going to be aided by a massive cash infusion, and investors continued to be optimistic. Clean teach fund investments reached $9.6 billion in 2009, almost double the amount raised in 2008. Khosla Ventures III raised $1 billion dollars, the majority of which would go towards clean tech investments. [10]

(Aggregate Fundraising for Clean Tech Venture Funds from 2007 – 2012, Preqin Database)

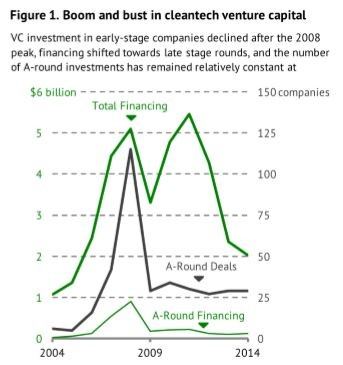

(A-round Venture Capital Investments spiking and crashing from 2004 – 2014, Gaddy et. al)

Unfortunately, the hype surrounding climate change and new regulations were not enough to counteract the inherent difficulties that made clean tech a bad sector for venture capital investments; clean tech investments required high upfront costs, developed hardware slowly, faced execution and manufacturing challenges, were exposed to highly volatile energy markets, and produced returns only after a long period of time. In 2016, after nearly a decade and over $25 billion invested by L.P.’s,[11] 90% of clean tech investments can be considered abject failures, and close to 100% can be considered poor investments.[12] The colossal and widespread failures of clean tech venture investments had numerous negative consequences: not just to the Limited Partners who lost tens of billions of dollars, but also the investors who bet their careers on clean tech venture capital.

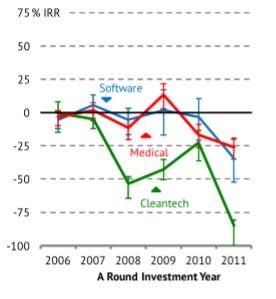

(A Round investment returns by year, relative to Medical and Software sectors from same vintage years, Gaddy et. al)

The governmental regulations that were instituted to address climate change spurred a venture capital bubble in clean tech investments which financially impacted not just a number of Limited Partners and their causes, but also a wide variety of Venture Capital Funds. Khosla Ventures II and Khosla Ventures III had dismal returns, at less than 5% IRR as of March, 2016.[13] This track record reduced their credibility and made their future fundraising efforts much more difficult. Although Khosla Ventures is still alive today, many other smaller clean tech funds went out of business completely.[14]

Perhaps the greatest negative ramification of all, beyond the capital losses at the L.P. and G.P. levels, is that dozens upon dozens of clean tech companies were over-capitalized, over-extended, and ultimately bankrupted. Of the 150 clean tech companies founded in Silicon Valley over the last 10 years, almost all of them have floundered and failed.[15][16] Evergreen, EPV, Solyndra, Spectrawatt, Sterling Energy- the list goes on. What is even more concerning is that now technology has progressed to the point where alternative energy solutions may be extremely compelling economically, yet the L.P. and G.P. community will not invest in clean tech for the foreseeable future due to the extremely poor track record. Heading into 2016, clean tech companies that are good investments may now fail because they struggle to receive financing.

Even when politicians agree on spending measures to encourage innovation and combat global warming, these regulatory changes can lead to market distortions as we saw in the venture capital industry from 2004-2016. Going forward we must attempt to carefully consider how new regulations may affect capital market investors, and the long-term trade offs between the value we gain from incentivizing markets to behave in a certain manner, and the potential long-term negative ramifications these market distortions may cause.

(Word Count: 793)

Sources:

- Benjamin Gaddy, Dr. Varun Sivaram, and Dr. Francis O’Sullivan, “Venture Capital and Cleantech: The Wrong Model for Clean Energy Innovation”, MIT Energy Initiative, July 2016, 4.

- “Bush Signs $12.3 Billion Energy Bill into Law”, NBC News, August 2005. http://www.nbcnews.com/id/8870039/ns/politics/t/bush-signs-billion-energy-bill-law/#.WBurXvkrK00

- Green is Good, The Times (London), Features, October, 2006, 23.

- Camilla Cavendish, “When it comes to investment, the smart money is going on ‘clean’ technologies”, Home News, The Times (London), October, 2006, 32.

- Katie Benner, “VCs Think Cleantech Is a Dirty Word”, Bloomberg View, November, 2014. https://www.bloomberg.com/view/articles/2014-11-14/vcs-think-cleantech-is-a-dirty-word

- Gaddy, “Venture Capital and Cleantech”, 1.

- Cavendish, “When it comes to investment, the smart money is going on ‘clean’ technologies”,

- Preqin Private Equity/Venture Capital Fund Profile, Tearsheet, Direct Investments, and Fund Performance, Khosla Ventures II, L.P. www.preqin.com

- Cavendish, “When it comes to investment, the smart money is going on ‘clean’ technologies”,

- Preqin Private Equity/Venture Capital Fund Profile, Tearsheet, Direct Investments, and Fund Performance, Khosla Ventures III, L.P. www.preqin.com

- Gaddy, “Venture Capital and Cleantech”, 1.

- Gaddy, “Venture Capital and Cleantech”, 19, figure 6.

- Preqin Private Equity/Venture Capital Fund Profile, Tearsheet, Direct Investments, and Fund Performance, Khosla Ventures III, L.P. www.preqin.com

- “CleanTech Investing, the Green Gold Rush”, GreenBiz, January 2008. https://www.greenbiz.com/news/2008/01/05/cleantech-investing-green-gold-rush

- Gaddy, “Venture Capital and Cleantech”, 1.

- Eric Wesoff, “Rest in Peace: The Fallen Solar Companies of 2014”, Greentech Media, December, 2014. https://www.greentechmedia.com/articles/read/Honoring-the-fallen-solar-soldiers

- Preqin Special Report: Cleantech, February 2013. https://www.preqin.com/research/

Thanks for this article. Looking at these poor VC investment results, makes me extremely worried. Could it be that investing in clean technologies is simply non profitable? If that is the case, the implications would be massive: it could mean that global warming is not a problem to be solved by the private sector.

If that were the case, what would be the best course of action to ensure that the climate change problem is tackled? Who would be responsible for taking charge of this massive issue? Could we rely on governments and NGOs to solve this issues by their own initiatives? Do governments need to take measures that make clean investments more profitable, and encourage investors and operators to dedicate their resources, talent, and time to ensuring global sustainability?

As you pointed out, low oil prices are one of the biggest barriers to clean tech and sustainability in general. When a budget conscious individual conducts a net present value analysis of the hybrid version of a car and its conventional equivalent, the analysis still resoundly points towards the conventional vehicle. I used to think that the free market would solve this problem by pushing up the cost of oil as supply continued to decrease (before the fracking boom) until alternatives became viable economic solutions, but now I see that there may be a need for governments to intervene to slow the pace of climate change.

This was a great post. Coming from the energy private equity world, I can certainly relate to the sentiment in this article. 80-90% of my former employer’s energy investments were in oil & gas, and of the renewable investments, very few were success stories. Renewable investments in the energy industry certainly carry a connotation with energy investors given its poor track record, and I hope that this sentiment can soon change. The primary issue in my mind is that the majority of these investments turn out to really be investments in science projects (many of which are unsuccessful because of failed science, or too much time / capital required to succeed) – not investments in businesses that can grow to scale. While I hope governments can incentivize the investments in renewable energy, investors can find it difficult to include these incentives in a long-term investment thesis. It’s a difficult issue surrounding sustainability, and I’m not sure what the right answer is. Nonetheless, hopefully over the next several years we can see some improvements in the performance of renewable investments to help encourage more investors to take on this risk.

From this blog, it sounds like the cratering of the clean-tech investment sector was more of a timing than a market opportunity issue. Additionally, government incentives and the price of oil seem to be key influencers on how investors view the opportunity. Especially with the 2016 election, given the division between the two candidates’ views, I wonder if a Democratic victory will spur investment in clean-tech, being the party of “government intervention” and spending. Additionally, as technology advances exponentially, one can hope we are closer to key breakthroughs that permit clean energy to be run more efficiently. Yet, these efficiencies will always be measured against the price of oil, an unknown variable. I can only hope government puts into action the right incentives to spur investment in clean-tech once again and assuage investors’ concerns regarding the viability of renewable energy.

I completely agree with one of your conclusions that over regulation by political entities can distort markets. That is clearly exemplified in the clean tech industry and I thought your blog post helped to lucidly articulate that view. What a blood bath. Outside of extraneous one-time events/reverberations in the market, has an asset class posted such putrid returns before? Really amazing. The one view that I would like to challenge is your assertion on capital allocation. I do broadly think that the market in its manifestations is efficient and while an asset class can go through short-term vagaries that ultimately the market is efficiently pricing in the risk of clean-tech. Could it be that capital is not going to this sector because perhaps the risk-reward profile of the asset class is still not what it should be? Perhaps we still have some way to go from a technological and cost perspective till the market sees these projects as viable from a risk standpoint.

Many thanks for the interesting and timely read as recruiting season approaches! As LPs turn their back on cleantech VC, it sadly appears that we are losing a generation of skilled cleantech investors at a time when electric vehicles, and distributed solar reach broad market acceptance. The risk-reward trade off for a budding VC investor with viable biotech and software options simply isn’t there at the moment.