Cerner and the Digitization of U.S. Healthcare Data

Imagine never having to fill out a form at a doctor’s office or showing up to an unfamiliar emergency room with the ER staff knowing your full medical history. This could be the new reality after universal adoption of electronic medical records.

Policy and Digital Transformation in the U.S. Healthcare System

Digital technology has dramatically transformed our everyday lives, but, in the bureaucratic maze of the U.S. healthcare system, widespread adoption of even the most basic healthcare information technology (IT) had been sluggish. In 2009, roughly 75% of Americans had a computer in their home [1], but only 22% of office-based physicians and 12% of non-federal acute care hospitals had a basic electronic medical record (EMR) system [2, Note 1]. The U.S. government decided to use policy in attempt to close this staggering technological gap, and the Health Information Technology for Economic and Clinical Health (HITECH) Act of 2009 was born.

Under the HITECH Act, Medicare and Medicaid providers, such as hospitals and clinics, were financially incentivized to become “meaningful users” of EMRs, since high upfront implementation costs were needed before benefits – such as improved patient and disease management, increased productivity, fewer medical errors, lower costs, and better diagnoses and patient outcomes – could be realized. Adoption of EMR systems significantly improved, resulting in 78% adoption of an EMR system by office-based physicians by 2013 and 48% adoption of a qualifying EMR system [3]. As of May 2015, more than 468,000 Medicare and Medicaid providers (87%) had received $30.4 billion of payments from the HITECH Act [4]. Given the recency of widespread EMR adoption in the healthcare ecosystem, full-scale benefits have yet to be achieved, but certain companies have come out on top of this digitization trend.

Cerner: The Early Bird Gets the Worm

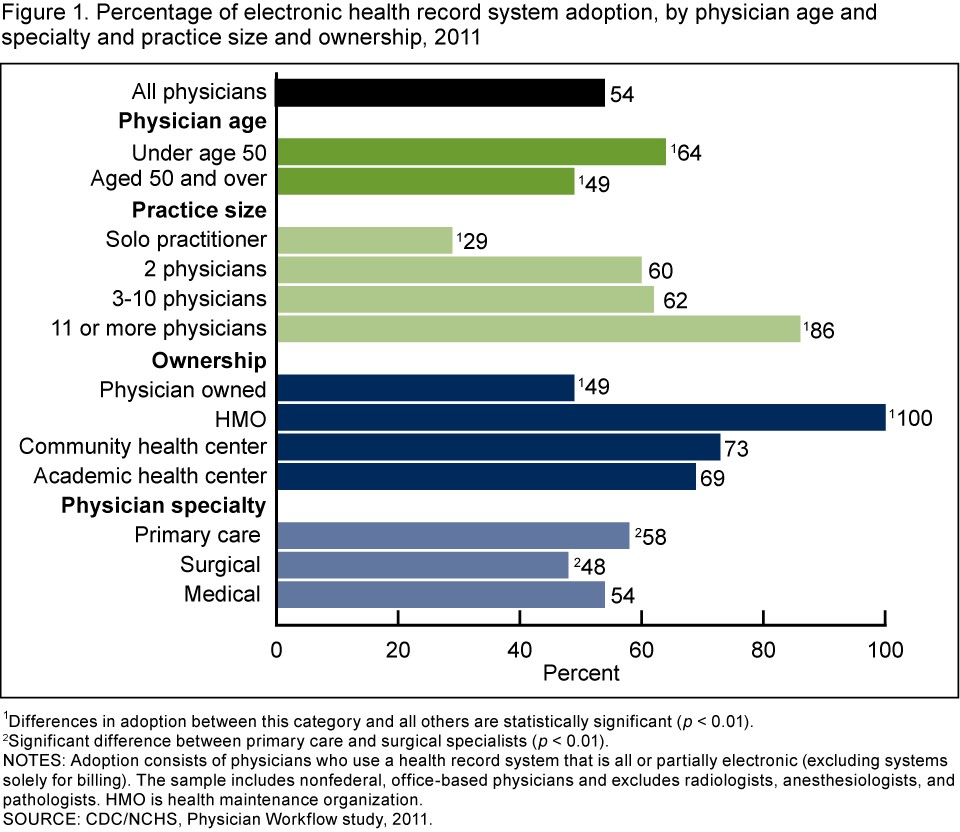

![]()

Founded in 1979, Cerner was one of the earliest companies to recognize the opportunity to help hospitals coordinate mission-critical patient care with medical information shared across a common platform. By the 1990s, Cerner decided to unorthodoxically organize large amounts of medical data by patient, instead of by physician, issue or payment, thus paving the way for the development of comprehensive EMRs [5]. Today, Cerner has the largest market share of the $27 billion EMR industry [6] and is also the world’s largest publicly traded health IT company with $4.4 billion revenue in 2015 and its solutions licensed at more than 25,000 facilities in over 35 countries [5]. How is Cerner winning?

Cerner Solutions, Services and Capabilities

Cerner’s value proposition to its customers is simple: Cerner’s EMR system can improve patient care and increase efficiency for the medical care team since they can access patient information at any time at any venue on the health system network. The Cerner EMR system is built on the HealtheIntent cloud-based platform providing the enterprise-wide, multi-facility, longitudinal EMR. This integrated database provides real-time access to patient medical history and results as well as clinical information across care disciplines, while also complying with regulatory patient confidentiality requirements. The recent $1.3 billion acquisition of Siemens Health Services in 2015 further augmented Cerner’s hospital information and EMR systems.

Cerner’s newsworthy Department of Defense (DoD) contract win in 2015 exemplifies many qualities that makes Cerner a game-changing digital healthcare player. Why was Cerner selected over a large competitor, Epic Systems, to replace the DoD’s legacy health IT system in 55 hospitals, 600 clinics and multiple military locations [7]? At the cornerstone is Cerner’s interoperable and integrated EMR system, a key differentiating factor in Cerner’s business model. Not only is its architecture more modular and flexible to suit DoD’s needs, Cerner is one of the founding partners of the CommonWell Health Alliance, which creates a secure nation-wide interoperability infrastructure for patient information sharing with other leading health IT providers. Epic Systems, on the other hand, decided to maintain its own separate, incompatible ecosystem of EMRs.

Cerner made a strategic operating choice to focus and deliver on interoperability and has amassed a wide range of customers including multistate health systems, accountable care organizations, government agencies, academic research institutions, physician private practices and critical access community hospitals. To serve this diverse customer base, Cerner also offers services such as implementation and training, remote hosting, operational management, support and maintenance, data analysis, and clinical process optimization among others.

Risks for the Future

As Cerner continues to expand its customer base and develop additional functionality within its EMR system, all players in this ecosystem stand to benefit – from physicians to patients and health system administrators, even Cerner itself. However, Cerner needs to ensure that its systems do not become an unwieldy time sink that threatens the efficiencies and cost-savings that digitization of patient information originally created. Epic Systems has already received significant and often public pushback from medical professionals and government officials [8].

Overall, such widespread digitization of patient health information can help solve a fundamental information supply and demand equilibrium issue in highly sensitive medical care settings. Digital transformation with EMRs can help save lives but we should also remain vigilant about cybersecurity risks that threaten the security of patient health data.

Word Count: 800

Notes:

- A basic EMR system is defined to do the following: record patient history and demographics, track patient problem lists, store physician clinical notes, record a comprehensive list of patients’ medications and allergies, provide for computerized ordering of prescriptions, and allow for electronic viewing of lab and imaging results.

Sources

- File, Thom. “Computer and Internet Use in the United States: Population Characteristics.” United States Census Bureau. May 2013. https://www.census.gov/prod/2013pubs/p20-569.pdf

- Charles, Dustin et al. “Adoption of Electronic Health Record Systems among U.S. Non-federal Acute Care Hospitals: 2008-2012.” The Office of the National Coordinator for Health Information Technology. March 2013. https://www.healthit.gov/sites/default/files/oncdatabrief9final.pdf

- Hsiao, Chun-Ju and Hing, Esther. “Use and Characteristics of Electronic Health Record Systems Among Office-based Physician Practices: United States, 2001–2013.” Centers for Disease Control Prevention. January 2014. http://www.cdc.gov/nchs/data/databriefs/db143.htm

- “Data and Program Reports.” Centers for Medicare & Medicaid Services. September 2016. https://www.cms.gov/Regulations-and-Guidance/Legislation/EHRIncentivePrograms/DataAndReports.html

- “Company Fact Sheet.” Cerner. November 2016. http://www.cerner.com/uploadedFiles/Fact-Sheet-2016Q4.pdf

- Landi, Heather. “Cerner Retains Largest Market Share in EMR Industry, Report Says.” Healthcare Informatics. June 16, 2016. http://www.healthcare-informatics.com/news-item/ehr/cerner-retains-largest-market-share-emr-industry-report-says

- Garamone, Jim. “DoD Awards Contract for Electronic Health Records.” U.S. Department of Defense. July 29, 2015. http://www.defense.gov/News/Article/Article/612714

- Caldwell, Patrick. “We’ve Spent Billions to Fix Our Medical Records, and They’re Still a Mess. Here’s Why.” Mother Jones. October 21, 2015. http://www.motherjones.com/politics/2015/10/epic-systems-judith-faulkner-hitech-ehr-interoperability

I really liked your post. I also wrote about EHR’s and the digitization of healthcare but did not touch on the interoperability of EHR’s between different EHR vendors like you did. I think it’s a very important point to bring up. If personal healthcare data is to be aggregated and used for healthcare analytics like we discussed during our Watson case, the EHR data needs to be compatible. This is an interesting example of competitive business interests clashing with public interests. I wonder if there will be future government regulation regarding the interoperability of EHR software for the good of scientific research.

Thank you for the post. Cerner is undoubtedly in a great position as the incumbent EHR supplier to many hospitals. However, they will become increasingly under pressure for healthcare technology startups aiming to take a slice of the EHR pie. Cerner must therefore ensure that it does not fall a victim of its own success, and that it does not lose sight of what it’s younger, nimbler competitors are doing. Large incumbents in many industries throughout history have been slow to adapt to ever changing landscapes, and so Cerner must ensure it does not follow this fate. I also feel that an aggressive M&A strategy of young startups developing technology which could be implemented into their system is a potential means of Cerner ensuring it maintains its position as the market leader.