Coffee is the second-most traded legal commodity in the world, after oil. Billions of cups are consumed every day. Most coffee drinkers reside in Europe and in the US, but all coffee is grown outside of these regions. Over 120 million people rely on coffee for their livelihoods and nearly 80% of all coffee is grown by farmers with relatively small landholding. However, there are less than 10 global companies that roast and sell coffee to consumers.1

The second largest player globally is JDE (Jacob Douwe Egberts), a company that was created in June 2015 through the merger of the coffee business of Mondelez International with the Dutch company DE Master Blenders. JDE is a pureplay coffee company that houses some of the world’s largest brands including Jacobs, Maxwell House, Gevalia and single-serve systems such as Tassimo2. With ambitions for top spot, JDE is gearing up for a spurt of sustained growth. Global demand trends are favorable for coffee. Consumption of coffee has grown an annual rate of 1.3% since 20123.

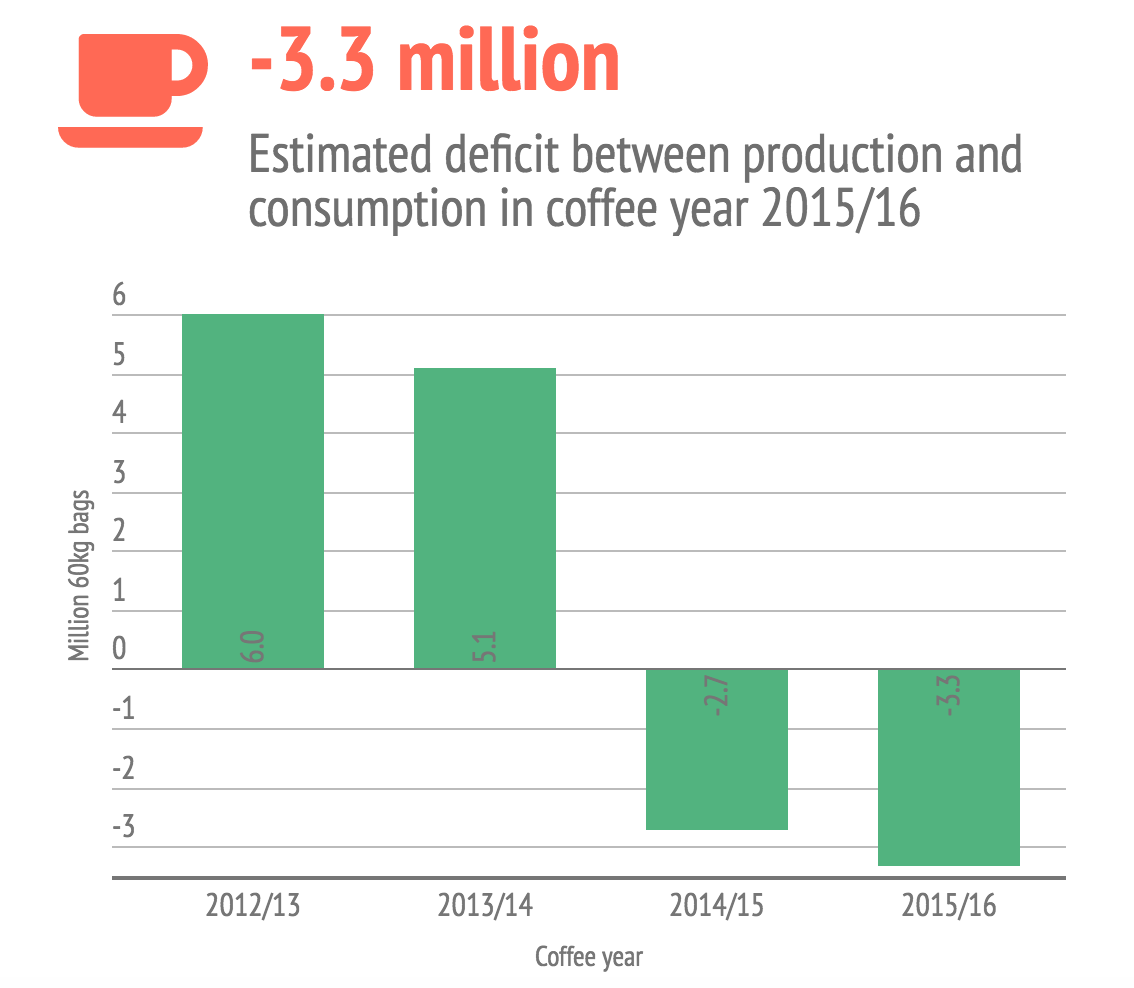

Understanding underlying trends in supply is complex due to the high volume of speculative trading in the commodities market. However, there are supply-side concerns emanating from patterns of climate change that are beginning to result in demand outstripping supply consistently. Despite its commonplace consumption, coffee requires a precise set of physical conditions to grow. Its quality as well as yield is affected acutely by changes in climate. Research indicates that area available globally for coffee farming may fall by as much as 50% by 20504.

Figure 1: Actual and estimated deficit between coffee demand and supply5

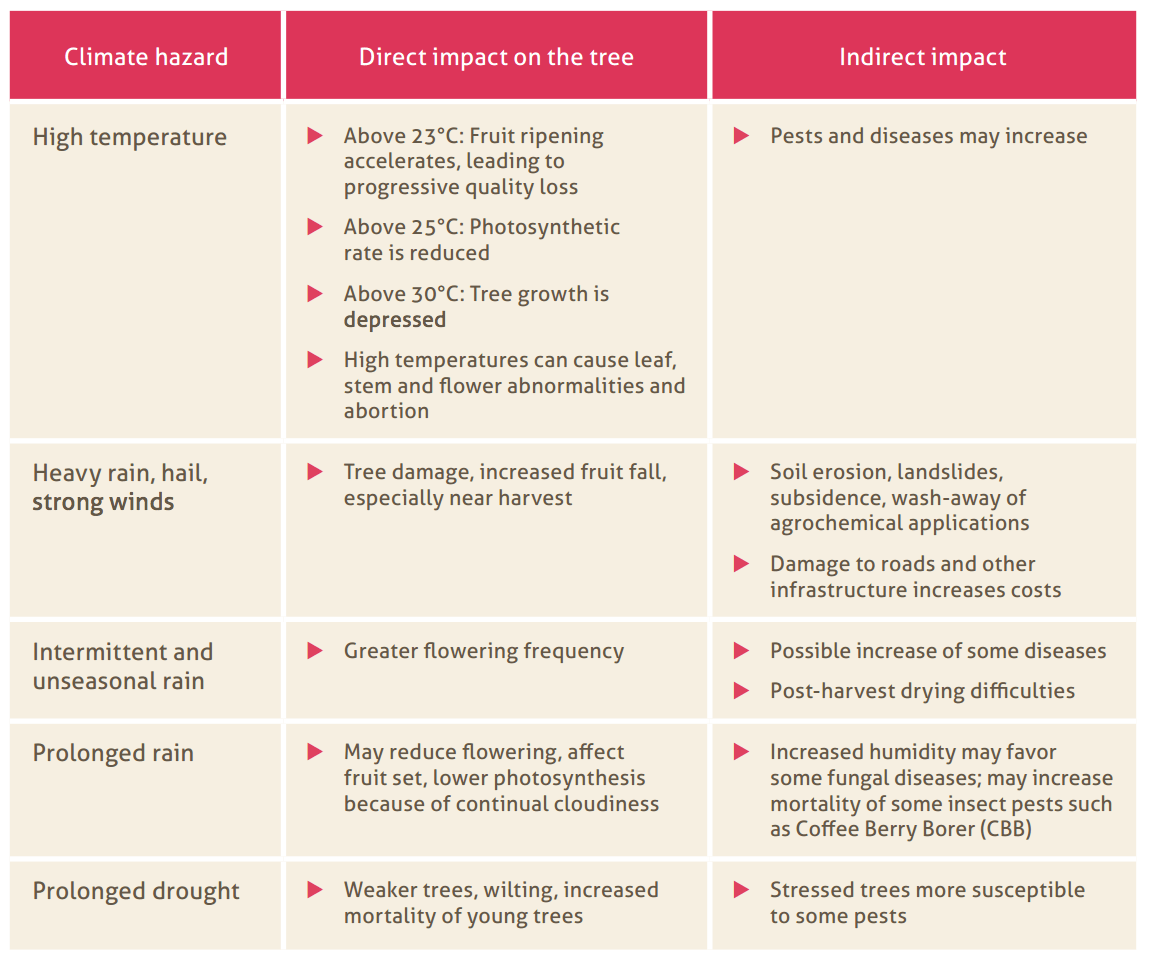

All coffee is grown between the Tropic of Cancer and the Tropic of Capricorn. There are two broad varieties of coffee beans: Arabica – grown primarily in Central and South America, and Robusta – primarily focused in Asia. The emergence of ‘coffee culture’ globally has focused on linking quality coffee with the Arabica bean: its value sales are roughly double those of Robusta. Arabica, however, is grown at high altitude in temperature ranging from 18-21oC 6. Coffee plants thrive in stable environments with predictable patterns of rainy and dry periods. These patterns are shifting. A combination of spells of high temperature, dry weather and heavy rain has created problems such as outbreaks of roya, the coffee rust disease7, and the emergence of new pests.

Figure 2: Impact on coffee plant from climate hazards8

The uncertainty and volatility that mars the production of coffee is a threat to the sustainability of JDE. In order to combat the effects on their operations, JDE is engaging in numerous initiatives to create favorable outcomes throughout its supply chain. A number of these programs were originally incubated in their legacy businesses.

Identification: The role of certification

Climate change impacts countries as diverse as Honduras, Brazil, Kenya and Vietnam. The company has engaged various external partners such as the Rainforest Alliance and 4C9 in order to create a set of guidelines and measure its growers’ current state, while creating financial incentives to encourage them to practice more sustainable practices. This allows them to understand areas of significant risk. However, there is limited impact on small farmers who are unable to achieve certification standards.

Capacity building

JDE has chosen the route of upskilling small-holding farmers instead of lobbying in the politics of climate change. Building up resilience10 to increasing climate variability requires both skills and financial access. Coffee Made Happy11 is a program that aims to invest $200 million in farmer training and provision of capacity building tools. For instance, an important method of hedging against unpredictable temperatures is shade management, the process of planting trees to provide shade and act as windbreakers to the fragile coffee plant. By educating farmers about such techniques and giving them access to credit markets12, the company hopes to achieve sustainable outcomes, at least for the next decade.

Looking beyond suppliers: Who cares?

In order to generate internal resources, JDE’s initiatives cannot conclude with their sourcing strategy. Ultimately, the company has to find a meaningful and motivating way for consumers to engage with the issue in order for the economics of this investment to work. It has historically been difficult for brands to justify demanding a price premium for certification. Circumstances facing those that are producing the coffee are simply not relatable to a vast majority of those consuming the product, and the time horizons for a complete shutdown of supply are simply too large for people to care. Empathy will need to be created through a concerted effort towards purposeful marketing and by bringing human stories from the origin countries to life for the mainstream consumer in an overt and relevant manner. After all, caring for those that care for the bean will ultimate result in the survival of our beloved morning java.

777 words

References:

- Coffee Barometer 2014: Report by Hivos, IUCN Nederlands, Oxfam Novib, Solidaridad and WWF <https://hivos.org/sites/default/files/publications/ coffee_barometer_2014_report_1.pdf>. Accessed Oct 2016

- JDE Brands <https://www.jacobsdouweegberts.com/brands/retail-brands/> Accessed Oct 2016

- International Coffee Organization <http://www.ico.org/monthly_coffee_trade_stats.asp> Accessed Oct 2016

- A Brewing Storm: The climate change risks to coffee: Report by the Climate Institute in partnership with Fairtrade <http://fairtrade.com.au/~/media/fairtrade%20australasia/files/resources%20for%20pages%20-%20reports%20standards%20and%20policies/tci_a_brewing_storm_final_24082016_web.pdf> Accessed Oct 2016

- International Coffee Organization <http://www.ico.org/monthly_coffee_trade_stats.asp>

- Joel Iscaro, ‘The Impact of Climate Change on Coffee Production in Colombia and Ethiopia’ <https://www.american.edu/cas/economics/ejournal/upload/Global_Majority_e_Journal_5_1_Iscaro.pdf> Accessed Oct 2016

- Climate Change Adaptation in Coffee Production: Report by Coffee&Climate <http://www.cabi.org/Uploads/projectsdb/documents/44640/Coffee%20and%20climate%20change%20guide.pdf> Accessed Oct 2016

- Coffee Barometer 2014: Report by Hivos, IUCN Nederlands, Oxfam Novib, Solidaridad and WWF <https://hivos.org/sites/default/files/publications/ coffee_barometer_2014_report_1.pdf> Accessed Oct 2016

- Carbon Disclosure Project Information Request 2015 <http://www.mondelezinternational.com/~/media/mondelezcorporate/uploads/downloads/cdpclimate2015.pdf> Accessed Oct 2016

- JDE Sourcing in Vietnam <https://www.jacobsdouweegberts.com/CR/source/vietnam/> Accessed Oct 2016

- Coffee Made Happy: Key Facts and Figures <http://www.mondelezinternational.com/~/media/MondelezCorporate/uploads/downloads/CoffeeMadeHappyFactsheet.pdf> Accessed Oct 2016

- Mondelez Wellbeing strategy <http://www.mdlzmeuap.com/well-being/agriculture-commodities/coffee-made-happy> Accessed Oct 2016

For coffee growers to remain viable one alternative could also be start investing in coffee varieties that can withstand adverse weathers and soil conditions. Coffee growers alone won’t be able to generate a change in the trend of climate change, but to remain in business they do have to find ways to overcome the change. Hedging against bad conditions in a short term relief, to be financially viable the product itself will need to adapt.

Interesting point about product – coffee is a single ingredient product, but you’re right maybe some work could be done on blends. Also some great work happening in the arena of instant coffee around yield (getting more ‘coffee’ out of every pound of bean).

Very interesting perspective on coffee. When suggesting potentially applicable initiatives for the company I researched about (Starbucks), I thought of developing partnerships with academia to understand better the impacts of climate change on coffee crops. Such collaboration could help identify genetically modified variations of coffee, more resistant to certain climate conditions, or even fertilizers or additives that could make coffee more adaptable to different climate scenarios. I believe JDE could also consider this approach going forward. After all, more scientific knowledge about the issue can only be beneficial to guide future actions.

100%! A number of companies like Unilever do quite well with becoming thought-leaders by partnering with universities on White Papers. Of course, the answer is both things need to be done: research, as well as ‘marketing’ to get consumers to care. Remember the fact that consumers in the world still continue to smoke tobacco knowing fully well the research on its link with heart disease and cancer…!

Awesome post! As someone that cannot function without coffee, coffee is very close to my heart. This is why your post headline “Melting polar caps or not having your morning coffee: what’s worse?” really caught my attention. I found very interesting Coffee Made Happy. Looking at their website, I was positively surprised about the emphasis they make on the importance of training smallholder farmers. That been said. I am concern that this strategy, an adaptation rather than a mitigation strategy, does not have the necessary scale to really combat climate change.

Very good point about scale. Coffee Made Happy was built to affect 1 million coffee farming households by 2020. Interesting fact: if all the coffee brands in the world chose to be ‘certified’ and good there’s a huge lag until supply could catch up – there simply isn’t enough of that type of coffee bean out there yet. So some fundamental changes needed in long term consumption.

Amazing post!

How do you think, we as consumers can help to make an impact here? Should we ask and look out for environmental friendly coffee? Should we be willing to pay up? Or is it really a question of demand and should we all try to limit ourselves in our daily intake?

I read that Nestle for their Nespresso brand and Starbucks have made an impact on the supply chain, as they only buy highest premium coffee that was produced in line with fair trade policies (because given their high price points and margins, they can afford it) – have they also put climate change on their agenda? Should they?

Some amazing questions. Consumers certainly do have the ultimate power in my opinion. Despite the power of brands to charge a premium, the fact that consumers vote with their wallets and buy certain brands over others is a huge motivator. Fairtrade vs Fair trade is a big debate too. The former is about price point and margins as you said, the latter about capabilities and access.