Trouble at Mitsubishi (Transforming Power Plant Business Portfolio)

Evolving trend of energy sources and challenge in transforming power generation business for an incumbent player

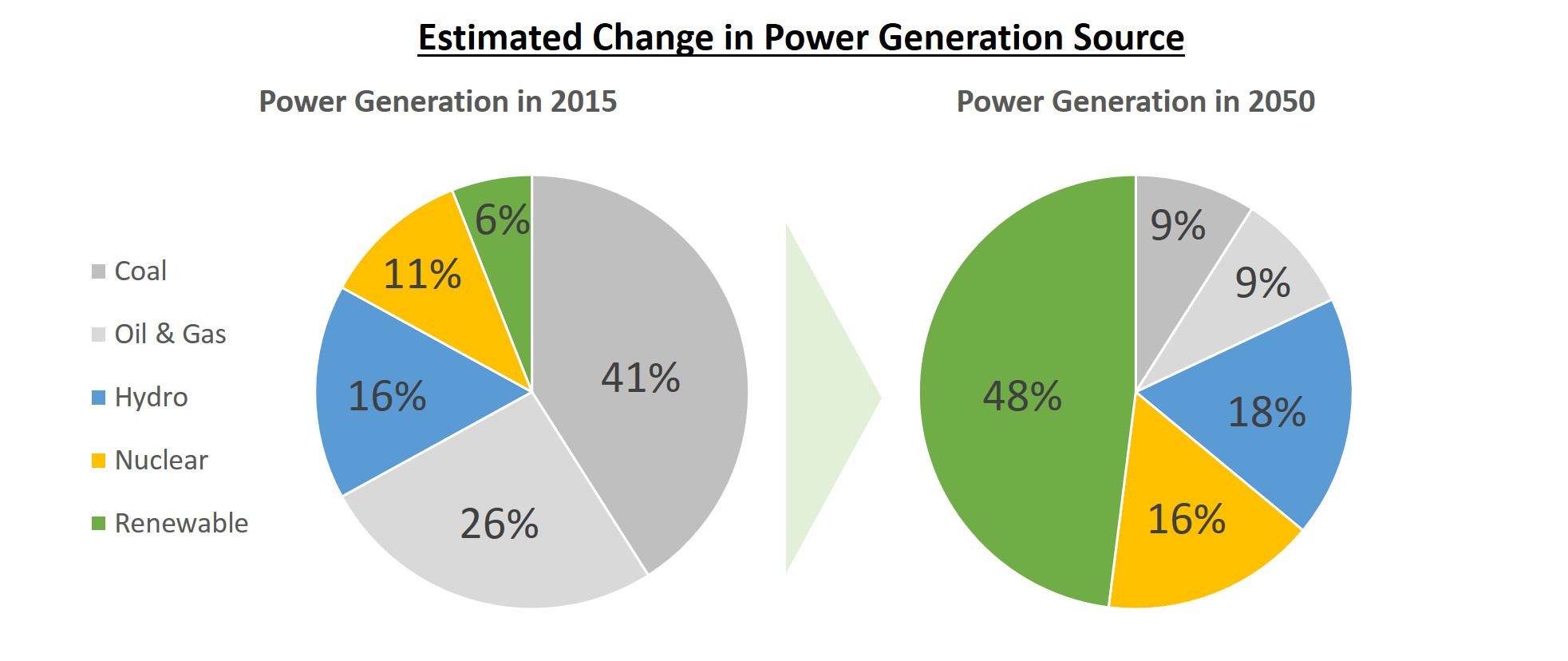

Power Generation Now & Future

Isn’t it striking that power generation by renewable energy accounts for still only 6% globally? 67% of power is generated by fossil fuels even today. Perhaps, some might feel that it has been quite a while since we started talking about renewable energy, leading to a prevailing skepticism whether renewable energy can really take over traditional energy sources…

However, in reality, the situation is gradually changing – partly backed by technological improvement [1], it is estimated that 48% of power generation will be done by renewable energy in 2050. How much do you think our power will be from traditional fossil fuels in 2050? The answer is only less than 20% [2].

Fossil-fuel Power Plant

Fossil fuel used in power generation includes mainly coal and natural gas.

(1) Coal:

For those who might be skeptical about the trend shift from fossil fuel to renewable, it might be surprising that use of coal in power plant has peaked out already, estimated to decrease its share as the fuel year by year going forward [2].

(2) Natural gas:

Often perceived as more eco-friendly fuel [3], natural gas will keep its popular position as a popular cleaner source of energy especially by emerging economies; however, it is estimated that even natural gas will peak out its share as the fuel circa 2030 [2].

While this trend is discussed in a global arena [4], How have power generation businesses been behaving, perceiving this trend? They should be aware of this long-term industrial trend, but it would be interesting to see whether they have been actually adjusting its power plant portfolio from “cash generating” fossil fuels power generation to economically less attractive renewable energy.

Trouble at Mitsubishi – Japan’s Leading Independent Power Producer

Mitsubishi Corporation (Mitsubishi) is one of the largest independent power plant developers in Japan. Mitsubishi is a diversified business entity, whose business coverage ranges from natural resources, infrastructure development (including power plant development), commodity trading, to retail business. Mitsubishi’s strategy is secure stable income from low-volatility assets such as power generation, and aim upside from high-volatility natural resources business, making power generation one of the most important strategic business segments [5].

Although some investors is skeptical about the concept of “diversification,” the company seems to believe that having stable income enables it to keep a good credit rating, as well as invest in natural resource assets at the bottom of market when competitors are financially constrained.

Power generation constitutes approximately 20% of its stable income depending on year [6]. Has Mitsubishi been able to adopt itself to the changing trend of fuel type in the world?

Analyzing its power asset portfolio [6], it is striking that most of its income is from fossil fuel power plants. Does this mean it has been ignorant of this ongoing trend in the world? Or is there any other lesson we can learn from here?

In fact, Mitsubishi established the division focusing on renewables and transferred more than a hundred employees to this division even before Lehman Shock. Also, it partnered with the strongest renewable player in the world, Spain’s ACCIONA, in the early 2009. It has been more than seven years since then. Why is it still stuck with only limited renewables portfolio?

Solving Dilemma?

This business case gives us an important lesson.

Successful companies’ internal control and governance system have optimized themselves to their ongoing successful business (i.e. in this case fossil-fueled power plant). So, using governance criteria for evaluating renewable business opportunity has been automatically filtering potentially competitive renewable assets.

This is not a problem unique to Mitsubishi. In power generation industry, there is a clear divide between the fossil fuel power players and renewable players. For instance, if you look at the website of TENASKA (American leading power plant developer) [7], you can find many natural gas power plant, but limited number of renewables. On the other hands, ACCIONA (global leading player in renewable) [8] has more than twenty renewable projects in the US, but no fossil fuel project.

My recommendation to Mitsubishi is as follows:

1) Curve-out renewable business division

It will be difficult for the existing, profitable fossil fuel power division to spare resources on renewables which is less profitable in a short-term.

2) Introduce different investment evaluation method in curved-out company

Risk-return of renewables is different from fossil fuel power plant. So, Mitsubishi should create a separate methodology to evaluate renewable business opportunity (for instance, assumption of longer investment period).

3) Acquire renewable energy developer with construction and operation functions

Considering the leading players (like ACCIONA) in renewable industry are equipped with not only investment function but construction and operation function (meaning they can enjoy income from construction, operation, and investment return), it is important to be on the same page for becoming competitive.

(Word Count: 798)

[1] Harvard Business School Case, N2-317-032 “Climate Change in 2016: Implications for Business” (Exhibit 20) (Oct 14, 2016)

[2] Under 450 Scenario, data based on “World Energy Outlook 2015”

[3] American Gas Association, https://www.aga.org/environmental-benefits-natural-gas (accessed on Nov 4, 2016)

[4] United Nations Environmental Programme, GEO-5 for Business: Impacts of a Changing Environment on the Corporate Sector

[5] Mid-term Strategy 2018, http://www.mitsubishicorp.com/global/ (accessed on Nov 1, 2016)

[6] Annual Reports, http://www.mitsubishicorp.com/global/ (accessed on Nov 1, 2016)

[7] http://www.tenaska.com/ (accessed on Nov 2, 2016)

[8] http://www.acciona.us/ (accessed on Nov 2, 2016)

Thanks for the piece Satoshi. I agree that a separate entity for renewables makes sense given potentially clashing incentives between the fossil-fuel based division and developing renewables. I wonder if we have a sense of how the return on investment and payback periods differ between developing renewable power plants and traditional fossil fuel plants? Are tradtitional plants still much more economically viable? If so a complete different entity that’s able to somehow attract capital with different required rates of return makes even more sense.

I believe this is not only a dilemma for Mitsubishi, but also one for most conglomerates in the world. Fossil fuels have been accounting for major source of energy consumption in the world for so many years that it’ll take long period for us to really improve the renewable energy, decrease the fossil fuels and balance them to an environmentally friendly portfolio. I agree with your proposal that Mitsubishi should create a separate methodology to evaluate renewable business opportunity, but the question would be how do we justify this methodology and how do we setup the appropriate standard to evaluate renewable business opportunity. Would Mitsubishi be really neutral and fair when designing the methodology standards? Would it be better if we involve an independent third-party to do this?

Great line of questioning! It’s always a mystery to me how large corporations focusing on fossil fuels adapt to this trend, to what degree, and how fast. Their partnership with ACCIONA seems like a major stride towards actions beyond investing, and I hope to learn more about it! What projects are they doing jointly? Is it going to be a separate entity in the future? How will the current infrastructure support and benefit from it?

Satoshi, I agree with the way you have laid out your approach to solving this dilemma. I actually think this issue applies not just to companies which have relied heavily on fossil fuels and are now are looking into renewable energy projects. An analogous case can be drawn to any tech company which is profitable with a current generation of technology, but still looks to invest in the next generation of technology. For example I am thinking of Kodak which did invest in digital technology but failed to embrace it. It is better to cannabilize one’s own share with a new technology (in this case renewable energy), than let someone else do it. With this issue in particular the time horizons are much longer, and so I agree there must be a different way to value renewable energy projects. In the short term it is easier to embrace a profitable fossil fuel business, but the leaders of Mitsubishi and other energy conglomerates must look farther out into the future.

I am very hopeful about the future however, especially as you have pointed out some of the projects and partnerships Mitsubishi has launched.

Great article! Very interesting to see how a large IPP in Japan approaches the difficulty of integrating renewable assets into its portfolio. Really enjoyed your point about companies such as Mitsubishi not being able to take on the risk of these projects directly. In the US, many companies get around this by setting up independent entities whose sole purpose is to develop renewable assets so that they don’t carry these projects directly on their balance sheets. The independent entities receive “sponsorship” from the parent company (such as Mitsubishi) and debt from banks who offer viable rates on the condition that the company demonstrates that it has secured future revenues for its power production, most commonly in the form of Purchase Power Agreements (PPAs). Here’s an old article about how renewable project finance works in the US: https://www.wsgr.com/PDFSearch/ctp_guide.pdf.

One important piece of the equation in the US are the favorable investment tax credits offered on many renewable projects. I would be curious to know whether Japan has a similar framework?

Thanks for sharing!

Satoshi – I completely agree. In fact, I’d encourage you to read my blog post about NRG Energy, the U.S.’s largest independent power producer. Unlike the path you’ve proposed for Mitsubishi, NRG attempted to transition its portfolio from fossil fuel (coal and natural gas-fired) power plants to renewables. In the process, however, they exposed a number of difficulties in executing such a transition. First, and foremost, is the difference in investment profile between fossil fuel power plants and renewables. The coal and natural gas-fired power plants had high cash flow yields and made money off of the so-called ‘dark’ and ‘spark’ spreads (basically the price at which energy can be acquired through fossil fuel commodities and the price at which resultant power can be sold into the market). By contrast, renewables have higher up-front capital costs and lower, bond-like cash yields (call it 8-14% to equity holders after accounting for tax equity?). Also important to NRG was the ‘culture clash’ that came from de-prioritizing an existing business. For individuals working at natural gas-fired power plants, what happens when the parent company says that the future is in utility-scale solar? As a business leader, it’s tough to tell your employees that you’re trying to put their part of the business (which they’ve worked in for the last 20 years!) out-of-business. For these reasons, I think your recommendation that Mitsubishi carve-out the renewables business and run it with a separate investment evaluation process make a lot of sense.

Going forward, I wonder whether there is also an opportunity for Mitsubishi in renewables services. Would Mitsubishi’s renewables business also be interested in developing a business around doing the ongoing services for solar or wind plants? In the U.S., some owners of these plants outsource the ongoing maintenance and break-fix to third parties. That could be a new, growing profit pool where a competitor of Mitsubishi’s scale could leverage global capabilities and generate value in a less asset-intensive way.

Great analysis Satoshi. I really appreciate how you have identified the underlying causes for Mitsubishi’s stagnant foray into renewable energy sources, and how you listed possible solutions for the company to overcome these issues. Like you said, I think this common problem of “optimizing for your ongoing business” is one that almost every major corporation faces in one way or another (not just in energy). Often times, these companies fail to see old growth cycles slowing down because the business is such a cash cow and any new growth cycle could be seen as “cannibalistic”. Consequently, many companies struggle to remain relevant when a certain area of their business is reinvented.

I really liked all the recommendations you presented for Mitsubishi. Maybe they could do some combination of 2 or three (i.e. carve-out but keep as a subsidiary under the same management and impose different investment criteria).

I was also wondering if you found or have heard of any companies that have struck a healthy balance between earning stable revenues from fossil-fuel power generation with growing revenues from renewable power projects? If not, this really could be a serious opportunity for Mitsubishi. Maybe they could even begin investing some of the cash generated from their traditional power businesses into building their renewable energy business (sounds crazy, I know).

Satoshi, really enjoyed reading your post as it is very related to mine. To quickly answer your questions on my post, Colbún currently does not have its NCRE investments in a separate entity, although they do go through a separate evaluation process compared to conventional energy projects. I very much agree that the company, as you propose for Mitsubishi as well, should move onto separating this two lines of businesses as they have very different risk profiles and expected returns. However, I think this depends on 2 factors:

1.- The company (be it Colbún or Mitsubishi) should have a considerable portfolio of NCRE investments so they can run in their on parallel vehicle and not be dependent of the parent company, which at least Colbún is not quite there yet, and would like to know where Mitsubishi stands.

2. How does the company see its investments in NCRE in relation to the entire generation portfolio? Colbún sees this kind of power generation as a complement to conventional generation, given the unstable pattern of NCRE sources. In this regard, having a separate entity doesn’t make sense. However, the company is aware that this will change in the future, so that is why it continues to invest in this types of technology with the plan to eventually have them go on their own in the future. What is Mitsubishi’s point of view in this area?

Despite my last point, I do agree that in the long term and with enough critical mass having a separate entity makes sense, as we can it with Enel (Italian conglomerate and one of the biggest generators in the world) with its parallel vehicle Enel Green Power for their renewable projects. However, they have had some “bad looks” from the market by raising capital at the conventional power level to later invest in the NCRE projects, so I think that is something to consider in the future as Mitsubishi moves down that path.